Financial Planning To Do's For A Family

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with the

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with them.

There is a lot of information to take into consideration when putting together a financial plan and the larger your family the more pieces to the puzzle. It is important to set goals and celebrate them when they are met. Everything cannot be done in a day, a week, or a month, so creating a task list to knock off one by one is usually an effective approach. Using relatives, friends, and professionals as resources is important to know what should be on that list for topics you aren’t familiar with.

Create a Budget

It may seem tedious but this is one of the most important pieces of a family’s financial plan. You don’t have to track every dollar coming in and out but having a detailed breakdown on where your money is being spent is necessary in putting together a plan. This simple Expense Planner can serve as a guideline in starting your budget. If you don’t have an accurate idea of where your money is being spent then you can’t know where you can cut back or afford to spend more if needed. Also, the budget is a great topic during a romantic dinner.

You will always want to have 4-6 months expenses saved up and accessible in case a job is lost or someone becomes disabled and cannot work. Having an accurate budget will help you determine how much money you should have liquid.

Insurance

You want to be sure you are sufficiently covered if anything ever happened. One terrible event could leave your family in a situation that may have been avoidable. Insurance is also something you want to take care of as soon as possible so you know the coverage is there if needed.

Health Insurance

Research the policies that are available to you and determine which option may be the most appropriate in your situation. It is important to know the medical needs of your family when making this decision.

Turning one spouse’s single coverage into family coverage is one of the more common ways people obtain coverage for a family. Insurance companies will usually only allow changes to policies through open enrollment or when a “qualifying event” occurs. Having a child is usually a qualifying event but this may only allow the child to be added to one’s coverage, not the spouse. If that is the case, the spouse will want to make sure they have their own coverage until they can be added to the family plan.

It is important to use the resources available to you and consult with your health insurance provider on the ins and outs. If neither spouse has coverage through work, the exchange can be a resource for information and an option to obtain coverage (https://www.healthcare.gov/).

Life Insurance

The majority of people will obtain Term Life Insurance as it is a cost effective way to cover the needs of your family. Life insurance policies have an extensive underwriting process so the sooner you start the sooner you will be covered if anything ever happened. How Much Life Insurance Do I Need?, is an article that may help answer the question regarding the amount of life insurance sufficient for you.

Disability Insurance

The probability of using disability insurance is likely more than that of life insurance. Like life insurance, there is usually a long underwriting process to obtain coverage. Disability insurance is important as it will provide income for your family if you were unable to work. Below are some terms that may be helpful when inquiring about these policies.

Own Occupation – means that insurance will turn on if you are unable to perform YOUR occupation. “Any Occupation” is usually cheaper but means that insurance will only turn on if you can prove you can’t do ANY job.

60% Monthly Income – this represents the amount of the benefit. In this example, you will receive 60% of your current income. It is likely not taxable so the net pay to you may be similar to your paycheck. You can obtain more or less but 60% monthly income is a common benefit amount.

90 Day Elimination Period – this means the benefit won’t start until 90 days of being disabled. This period can usually be longer or shorter.

Cost of Living or Inflation Rider – means the benefit amount will increase after a certain time period or as your salary increases.

Wills, POA’s, Health Proxies

These are important documents to have in place to avoid putting the weight of making difficult decisions on your loved ones. There are generic templates that will suffice for most people but it is starting the process that is usually the most difficult. “What Is The Process Of Setting Up A Will?, is an article that may help you start.

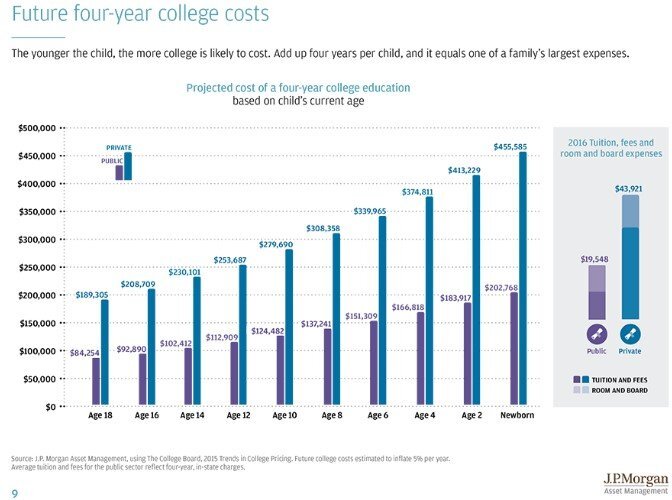

College Savings

The cost of higher education is increasing at a rapid rate and has become a financial burden on a lot of parents looking to pick up the tab for their kids. 529 accounts are a great way to start saving early. There are state tax benefits to parents in some states (including NYS) and if the money is spent on tuition, books, or room and board, the gain from the investments is tax free. Roth IRA’s are another investment vehicle that can be used for college but for someone to contribute to a Roth IRA they must have earned income. Therefore, a newborn wouldn’t be able to open a Roth IRA. Since the gain in 529’s is tax free if used for college, the earlier the dollars go into the account the longer they have to potentially earn income from the market.

529’s can also be opened by anyone, not just the parents. So if the child has a grandparent that likes buying savings bonds or a relative that keeps purchasing clothes the child will wear once, maybe have them contribute to a 529. The contribution would then be eligible for the tax deduction to the contributor if available in the state.

Below is a chart of the increasing college costs along with links to information on college planning.

About Rob……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Strategies to Save for Retirement with No Company Retirement Plan

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. We wrote the article, How Much Money Do I Need To Save To Retire?, to help individuals answer this question. This article is meant to help create a strategy to reach that number. More

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. We wrote the article, How Much Money Do I Need To Save To Retire?, to help individuals answer this question. This article is meant to help create a strategy to reach that number. More specifically, for those who work at a company that does not offer a company sponsored plan.

Over the past 20 years, 401(k) plans have become the most well-known investment vehicle for individuals saving for retirement. This type of plan, along with other company sponsored plans, are excellent ways to save for people who are offered them. Company sponsored plans are set up by the company and money comes directly from the employees paycheck to fund their retirement. This means less effort on the side of the individual. It is up to the employee to be educated on how the plan operates and use the resources available to them to help in their savings strategy and goals but the vehicle is there for them to take advantage of.

We also wrote the article, Comparing Different Types of Employer Sponsored Retirement Plans, to help business owners choose a retirement plan that is most beneficial to them in their retirement savings.

Now back to our main focus on savings strategies for people that do not have access to an employer sponsored plan. We will discuss options based on a few different scenarios because matters such as marital status and how much you’d like to save may impact which strategy makes the most sense for you.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Not Maxing Out

A common strategy we use for clients when a covered spouse is not maxing out their deferrals is to increase the deferrals in the retirement plan and supplement income with the non-covered spouse’s salary. The limits for 401(k) deferrals in 2021 is $19,500 for individuals under 50 and $26,000 for individuals 50+. For example, if I am covered and only contribute $8,000 per year to my account and my spouse is not covered but has additional money to save for retirement, I could increase my deferrals up to the plan limits using the amount of additional money we have to save. This strategy is helpful as it allows for easier tracking of retirement accounts and the money is automatically deducted from payroll. Also, if you are contributing pre-tax dollars, this will decrease your tax liability.

Note: Payroll deferrals must be withheld from payroll by 12/31. If you owe money when you file your taxes in April, you would not be able to go back and increase your deferrals in your company plan for that tax year.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Maxing Out

If the covered spouse is maxing out at the high limits already, you may be able to save additional pre-tax dollars depending on your Adjusted Gross Income (AGI).

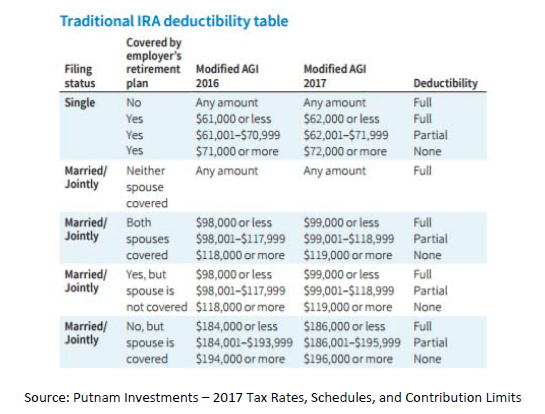

Below is the Traditional IRA Deductibility Table for 2021. This table shows how much individuals or married couples can earn and still deduct IRA contributions from their taxable income.

As shown in the chart, if you are married filing jointly and one spouse is covered, the couple can fully deduct IRA contributions to an account in the covered spouses name if AGI is less than $99,000 and can fully deduct IRA contributions to an account in the non-covered spouses name if AGI is less than $184,000. The Traditional IRA limits for 2017 are $5,500 if under 50 and $6,500 if 50+. These lower limits and income thresholds make contributing to company sponsor plans more attractive in most cases.

Single or Married Filing Jointly and Neither Spouse is Covered

If you (and your spouse if married filing joint) are not covered by an employer sponsored plan, you do not have an income threshold for contributing pre-tax dollars to a Traditional IRA. The only limitations you have relate to the amount you can contribute. These contribution limits for both Traditional and Roth IRA’s are $5,500 if under 50 and $6,500 if 50+. If married filing joint, each spouse can contribute up to these limits.

Unlike employer sponsored plans, your contributions to IRA’s can be made after 12/31 of that tax year as long as the contributions are in before you file your tax return.

Please feel free to e-mail or call with any questions on this article or any other financial planning questions you may have.

Below are related articles that may help answer additional questions you have after reading this.

Traditional vs. Roth IRA’s: Differences, Pros, and Cons

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Year End Tax Strategies

The end of the year is always a hectic time but taking the time to sit with a tax professional and determine what tax strategies will work best for you may save thousands on your tax bill due April 15th. As the deadline for your taxes starts to get closer, you may be in such a rush to file them on time that you make some mistakes in the process, but

year end tax strategies

The end of the year is always a hectic time but taking the time to sit with a tax professional and determine what tax strategies will work best for you may save thousands on your tax bill due April 15th. As the deadline for your taxes starts to get closer, you may be in such a rush to file them on time that you make some mistakes in the process, but don't worry, you won't be the only one. If you don't have the relevant tax strategy in place, you are more prone to mistakes. So, the purpose of this article is to discuss some of the most common tax strategies that may apply to you. It may be worth contacting a company that specializes in tax services if you're unsure of how to go about these strategies though. Some of the deadlines for these strategies aren't until tax filing but the majority include an action item that must be done by December 31st to qualify and therefore taking the time before year end is crucial.

Taxable Investment Accounts

Offset some of the realized gains incurred during the year by selling investments in loss positions. Often times dividends received and sales made in a taxable investment account are reinvested. Although the owner of the account never received cash in the transaction, the gain is still realized and therefore taxable. This may cause an issue when the cash is not available to pay the tax bill. By selling investments in a loss position prior to 12/31, you will offset some, if not all, of the gain realized during the year. If possible, sell enough investments in a loss position to take advantage of the maximum $3,000 loss that can be claimed on your tax return.

Note: The IRS recognized this strategy was being abused and implemented the "wash sale" rule. If you sell an investment in a loss position to diminish gains and then repurchase the same investment within 30 days, the IRS does not allow you to claim the loss therefore negating the strategy.

Convert a Traditional IRA to a Roth IRA

If you are in a low income year and will be taxed at a lower tax bracket than projected in the future, it may make sense to convert part of a traditional IRA to a Roth IRA. The current maximum contribution to a Roth IRA in a single year is $5,500 if under 50 and $6,500 if 50 plus. You will pay taxes on the distributions from the traditional but the benefit of a Roth is that all the contributions and earnings accumulated is tax free when distributed as long as the account has been opened for at least 5 years. Roth accounts are typically the last touched during retirement because you want the tax free accumulation as long as possible. Also, Roth accounts can be passed to a beneficiary who can continue accumulating tax free. Roth money is after tax money and therefore the IRS allows you to withdraw contributions tax and penalty free and let the earnings continue to accumulate tax free. If you don't have the cash come tax time to cover the conversion, you can convert the Roth money back to a traditional IRA by tax filing plus extension and the account will be treated as the Roth conversion never took place.

Donate to Charity if you Itemize

If you itemize deductions on your tax return, go through your closet and donate any clothing or household goods that you no longer use. There are helpful tools online that will allow you to value the items donated but be sure you keep record of what was donated and have the charity give you a receipt.

Max Out Your Employer Sponsored Retirement Plan

If you know you will be hit with a big tax bill and want to defer some of the taxes, max out your retirement plan if you haven't already. Employer sponsored plans, such as 401(k)'s, must be funded through payroll by 12/31 and therefore it is important to make this determination early and request your payroll department start upping your contribution for the remaining payroll periods in the year. The maximum for 401(k)'s in 2015 and 2016 is $18,000 if under 50 and $24,000 if 50 plus.

Business Owners – Cut Checks by 12/31

If your company had a great year and the cash is available, use it to pay for expenses you would normally hold off on. This could mean paying state taxes early, paying invoices you usually wait until the end of the payment term, paying monthly expenses like health or general insurance, or buying new office equipment. This might also mean investing in new office furniture such as chairs and desks, or more storage space for all of your paperwork and electronics. Above all, by getting the checks cut by 12/31, you realize the expense in the current year and will decrease your tax bill.

Business Owners – Set Up a Retirement Plan

For owners with no full time employees, a Single(k) plan being put in place by 12/31 will allow you to fund a retirement account up to the 401(k) limits mentioned early. As long as the plan is established by 12/31, the owner will be able to fund the plan any time before tax filing plus extension. If the plan is not established by 12/31, other options like the SEP IRA are available to take money off the table come tax time.With tax laws continuously changing, it is important to consult with your tax professional as there may be strategies available to you that could save you money. Don't procrastinate as some planning before the end of the year may be necessary to take full advantage.

About Rob.........

Hi, I'm Rob Mangold. I'm the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Should I Establish an Employer Sponsored Retirement Plan?

Employer sponsored retirement plans are typically the single most valuable tool for business owners when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

establishing an employer sponsored retirement plan

Employer sponsored retirement plans are typically the single most valuable tool for business owners when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

But with all of the different types of plans to choose from which one is the right one for your business? Most business owners are familiar with how 401(k) plans works but that might not be the right fit given variables such as:

# of Employees

Cash flows of the business

Goals of the business owner

There are four main stream employer sponsored retirement plans that business owners have to choose from:

SEP IRA

Single(k) Plan

Simple IRA

401(k) Plan

Since there are a lot of differences between these four types of plans we have included a comparison chart at the conclusion of this newsletter but we will touch on the highlights of each type of plan.

SEP IRA PLAN

This is the only employer sponsored retirement plan that can be setup after 12/31 for the previous tax year. So when you are sitting with your accountant in the spring and they deliver the bad news that you are going to have a big tax liability for the previous tax year, you can establish a SEP IRA up until your tax filing deadline plus extension, fund it, and take a deduction for that year.

However, if the company has employees that meet the plan's eligibility requirement, these plans become very expensive very quickly if the owner(s) want to make contributions to their own accounts. The reason being, these plans are 100% employer funded which means there are no employee contributions allowed and the employer contribution is uniform for all plan participants. For example, if the owner contributes 15% of their income to the SEP IRA, they have to make an employer contribution equal to 15% of compensation for each employee that has met the plans eligibility requirement. If the 5305-SEP Form, which serves as the plan document, is setup correctly a company can keep new employees out of the plan for up to 3 years but often times it is either not setup correctly or the employer cannot find the document.

Single(k) Plan or "Solo(k)"

These plans are for owner only entities. As soon as you have an employee that works more than 1000 hours in a 12 month period, you cannot sponsor a Single(k) plan.

The plans are often times the most advantageous for self-employed individuals that have no employees and want to have access to higher pre-tax contribution levels. For all intents and purposes it is a 401(k) plan, same contributions limits, ERISA protected, they allow loans and Roth contributions, etc. However, they can be sponsored at a much lower cost than traditional 401(k) plans because there are no non-owner employees. So there is no year-end testing, it's typically a boiler plate plan document, and the administration costs to establish and maintain these plans are typically under $400 per year compared to traditional 401(k) plans which may cost $1,500+ per year to administer.

The beauty of these plans is the "employee contribution" of the plan which gives it an advantage over SEP IRA plans. With SEP IRA plans you are limited to contributions up to 25% of your income. So if you make $24,000 in self-employment income you are limited to a $6,000 pre-tax contribution.

With a Single(k) plan, for 2021, I can contribute $19,500 per year (another $6,500 if I'm over 50) up to 100% of my self-employment income and in addition to that amount I can make an employer contribution up to 25% of my income. In the previous example, if you make $24,000 in self-employment income, you would be able to make a salary deferral contribution of $18,000 and an employer contribution of $6,000, effectively wiping out all of your taxable income for that tax year.

Simple IRA

Simple IRA's are the JV version of 401(k) plans. Smaller companies that have 1 – 30 employees that are looking to start are retirement plan will often times start with implementing a Simple IRA plan and eventually graduate to a 401(k) plan as the company grows. The primary advantage of Simple IRA Plans over 401(k) Plans is the cost. Simple IRA's do not require a TPA firm since they are self-administered by the employer and they do not require annual 5500 filings so the cost to setup and maintain the plan is usually much less than a 401(k) plan.

What causes companies to choose a 401(k) plan over a Simple IRA plan?

Owners want access to higher pre-tax contribution limits

They want to limit to the plan to just full time employees

The company wants flexibility with regard to the employer contribution

The company wants a vesting schedule tied to the employer contributions

The company wants to expand investment menu beyond just a single fund family

401(k) Plans

These are probably the most well recognized employer sponsored plans since at one time or another each of us has worked for a company that has sponsored this type of plan. So we will not spend a lot of time going over the ins and outs of these types of plan. These plans offer a lot of flexibility with regard to the plan features and the plan design.

We will issue a special note about the 401(k) market. For small business with 1 -50 employees, you have a lot of options regarding which type of plan you should sponsor but it's our personal experience that most investment advisors only have a strong understanding of 401(k) plans so they push 401(k) plans as the answer for everyone because it's what they know and it's what they are comfortable talking about. When establishing a retirement plan for your company, make sure you consult with an advisor that has a working knowledge of all these different types of retirement plans and can clearly articulate the pros and cons of each type of plan. This will assist you in establishing the right type of plan for your company.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Inherited IRA's: How Do They Work?

An Inherited IRA is a retirement account that is left to a beneficiary after the owner’s death. It is important to have a general knowledge of how Inherited IRA’s work because a minor error in how the account is set up could lead to major tax consequences.

how do inherited ira's work

An Inherited IRA is a retirement account that is left to a beneficiary after the owner’s death. It is important to have a general knowledge of how Inherited IRA’s work because a minor error in how the account is set up could lead to major tax consequences.

Before going into the different kinds of Inherited IRA’s, if you are the sole beneficiary of your spouse’s IRA, you are able to transfer the assets to your own existing IRA or to a new IRA through what is called a “Spousal Transfer”. This account is not treated as an Inherited IRA and therefore is subject to all the rules a Traditional IRA would be subject to as if it was always held in your name. If the spouse needs to have access to the money before age 59 ½, it would probably make sense to set up an Inherited IRA because this would give the spouse options to access the money without incurring a 10% early withdrawal penalty.

Withdrawal Rules for Spouse & Non-Spouse Beneficiaries

The SECURE Act that passed in December 2019 dramatically changed the distribution options that are available to non-spouse beneficiaries. If you are spousal beneficiary please reference the following article:

10 Year Method

All the assets must be distributed by the 10th year after the year in which the account holder died. This option may make sense compared to the Lump Sum option explained next to spread out the tax liability over a longer period.

Lump Sum Distribution

You may take a lump sum distribution when the account is inherited. It is recommended that you consult your tax preparer to discuss the tax consequences of this method since you may move up into a different tax bracket.

Additional Takeaways

If the decedent was required to take a distribution in the year of death, it is important to determine whether or not the decedent took the distribution. If the decedent was required to take a RMD but did not do so in the year they passed, the inheritor must take the distribution based on the life expectancy of the decedent or the distribution will be subject to a 50% penalty. Distributions going forward will be based on the life expectancy of the inheritor.

It is important to be sure a beneficiary form is completed for the Inherited IRA. If there is no beneficiary and the account goes to an estate then the inheritor will have limited choices on which distribution method to choose among other tax consequences.

You are only able to combine Inherited IRA’s if they were inherited from the same individual. If you have multiple Inherited IRA’s from different individuals, you cannot commingle the assets because of the distributions that must be taken.

There is no 60 day rule with Inherited IRA’s like there is with other Traditional IRA’s. The 60 day rule allows someone to withdraw money from an IRA and as long as it’s replenished within 60 days there is no tax consequence. This is not available with Inherited IRA’s, all non-Roth distributions are taxable.

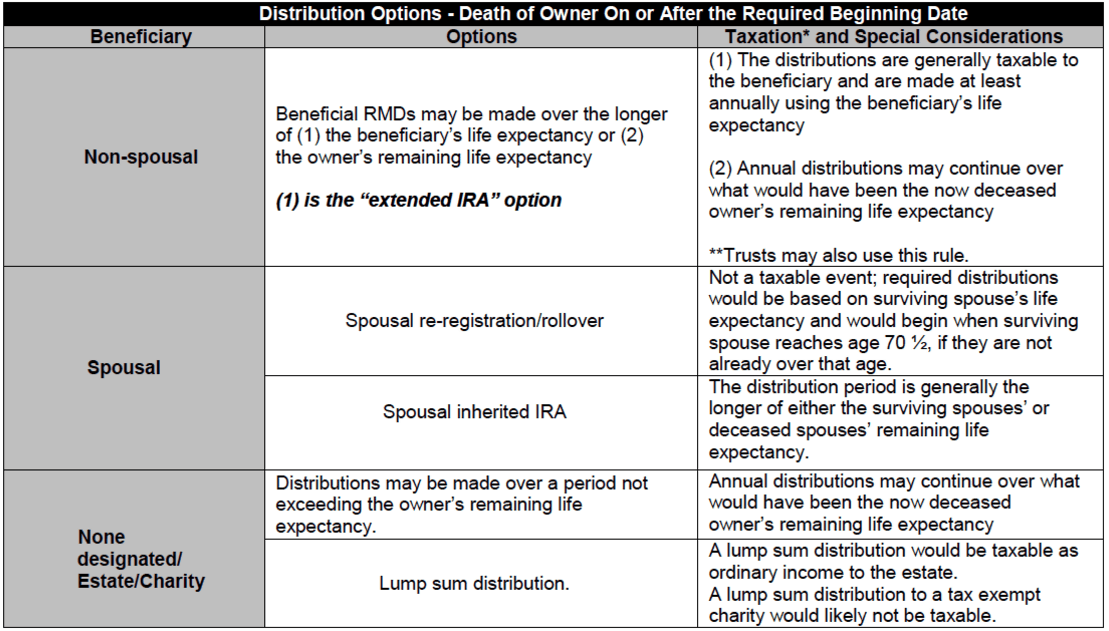

The charts below are from insurancenewsnet.com publication titled “Extended IRA Quick Reference Guide” give another look at the details of Inherited IRA’s.

inherited ira options

inherited ira distribution options

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Backdoor Roth IRA Contribution Strategy

This strategy is for high income earners that make too much to contribute directly to a Roth IRA. In recent years, some of these high income earners have been implementing a “backdoor Roth IRA conversion strategy” to get around the Roth IRA contribution limitations and make contributions to Roth IRA’s via “conversions”. For the 2020 tax year, your

backdoor roth ira strategy

This strategy is for high income earners that make too much to contribute directly to a Roth IRA. In recent years, some of these high income earners have been implementing a “backdoor Roth IRA conversion strategy” to get around the Roth IRA contribution limitations and make contributions to Roth IRA’s via “conversions”. For the 2021 tax year, your ability to make contributions to a Roth IRA begins to phase out at the following AGI thresholds based on your filing status:

Single: $125,000

Married Filing Jointly: $198,000

Married Filing Separately: $0

However, in 2010 the IRS removed the income limits on “IRA Conversions” which open up an opportunity……if executed correctly…….for high income earners to make “backdoor” contributions to a Roth IRA.

Why would a high income earning want to contribute to a Roth IRA? Once high income earners have maxed out their contributions to their employer sponsored retirement plans, they usually begin to fund plain vanilla investment management accounts or whole life insurance policies. When assets accumulate in an investment management account, once liquidated, the account owner typically has to pay either short-term or long term capital gains on the appreciation. For whole life insurance, even though the accumulation is tax deferred, if the policy is surrendered, the policy owner pays ordinary income tax on the gain in the policy.

With a Roth IRA, after tax contributions are made to the account and the gains in the account are withdrawn TAX FREE if the account owner at the time of withdrawal is over the age of 59½ and the Roth IRA has been in existence for 5 years. A huge tax benefit for high income earners who are typically in a medium to higher tax bracket even in retirement.

Here is how the strategy works

Rollover all existing pre-tax IRA’s into your employer sponsored retirement plan

Make a non-deductible contribution to a Traditional IRA

Convert the Traditional IRA to a Roth IRA

Here are the pitfalls in the execution process

Over the years, more and more individuals have become aware of this wealth accumulation strategy. However, there are risks associated with executing this strategy and if not executed correctly could result in adverse tax consequences.

Here are the top pitfalls:

Forget to aggregate Pre-Tax IRA’s

Do not understand that SEP IRA’s and Simple IRA’s are included in the Aggregation Rule

They create a “step transaction”

Pitfall #1: IRS Aggregation Rule

The IRA aggregate rule stipulates that when an individual has multiple IRAs, they will allbe treated as one account when determining the tax consequences of any distributions (including a distribution out of the account for a Roth conversion).

This creates a significant challenge for those who wish to do the backdoor Roth strategy, but have otherexisting IRA accounts already in place (e.g., from prior years’ deductible IRA contributions, or rollovers from prior 401(k) and other employer retirement plans). Because the standard rule for IRA distributions (and Roth conversions) is that any after-tax contributions come out along with any pre-tax assets (whether from contributions or growth) on a pro-rata basis, when all the accounts are aggregated together, it becomes impossible to justconvert the non-deductible IRA.

picture

If an individual has pre-tax IRA’s we typically recommend that they rollover those IRA’s into their employer sponsored retirement plans which eliminates all of their pre-tax IRA balance and then open the opportunity to execute this backdoor Roth IRA contribution strategy.

Pitfall #2: SEP IRA & Simple IRA's count

Many smaller companies and self-employed individuals sponsor SEP IRA’s or Simple IRA Plans. Many individuals just assume that these are “employer sponsored retirement plans” not subject to the aggregation rules. Wrong. In the eyes of the IRS these are “pre-tax IRA’s” and are subject to the aggregation rules. If you have a Simple IRA or SEP IRA, make sure you take this common pitfall into account.

Pitfall #3: Beware IRS Step Transaction Rule

This is probably the most common pitfall that we see when executing this strategy. Individuals and investment advisors alike will make deposits to the non-deductible traditional IRA and then the next day process the conversion to the Roth IRA. In doing this, you run the risk of creating a “step transaction”.

There is a very long explanation tied to “step transactions” and how to avoid a “step transactions” but I will provide you with a brief summary of the concept.

Here it is, if you use legal loop holes in the tax system in an obvious effort to side step other IRS limitations (like the Roth IRA income limit) it could be considered a “step transaction” by the IRS and the IRS may disallow the conversion and assess tax penalties.

Disclosure: Backdoor Roth IRA Conversion Strategy

It is highly recommend that you work closely with your financial advisor and tax advisor to determine whether or not this is a viable wealth accumulation strategy based on your personal financial situation.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

What is the 60 Day Rule and How Should it be Used?

The 60 day rule refers to the length of time an individual has to deposit money back into a retirement account that was previously withdrawn without incurring a taxable event. There are a number of reasons someone would withdraw money from an account whether it be to pay a large tax bill, obtain cash for an unexpected expense, or to rollover the

60 day rollover

The 60 day rule refers to the length of time an individual has to deposit money back into a retirement account that was previously withdrawn without incurring a taxable event. There are a number of reasons someone would withdraw money from an account whether it be to pay a large tax bill, obtain cash for an unexpected expense, or to rollover the balance into another retirement account.

There are multiple ways to rollover a balance from one retirement account to another so we will begin by explaining the more common ways to rollover a balance where the 60 day rule won't come into play.

Direct Rollover

A direct rollover is a transfer from a retirement plan to another retirement plan or IRA where the custodian of your current plan makes payment directly to your new account. This can be in the form of a check made payable to the new account custodian or a direct wire transfer. This method will avoid taxes and penalties because the account owner never had access to the cash during the transfer.

Trustee to Trustee Transfer

Similar to the direct rollover, a trustee to trustee transfer moves money from one IRA to another IRA without the account owner ever having access to the cash and therefore avoiding taxes and penalties.

The direct rollover and trustee to trustee transfer methods both avoid taxes and penalties as cash is never available to the owner and therefore the 60 day rule does not come into effect. In any case where the account owner has access to the cash, the money will have to be redeposited into another retirement account within 60 days or the owner will be taxed on any pre-tax dollars and possibly penalized if the owner is under the age of 59 ½.

The 60 day rule is one of the only ways an owner has access to money in a retirement account without paying taxes or penalties on the distribution. An individual can take advantage of this if they are in need of immediate cash for something like an unexpected expense. The distribution is essentially an interest free loan from your retirement account for 60 days. If the money is not available within the 60 days to redeposit, taxes and possible penalties will be assessed on the distribution.

IRS: One 60 Day Rollover in 12 Month Rule

The IRS recognized that individuals were taking advantage of this rule by taking multiple distributions in a single year and therefore increasing the time period. Beginning after January 1, 2015, the IRS changed the law to state that only one rollover can be made from one IRA to another IRA within a 12 month period. This rule does not apply to the following:

rollovers from traditional IRAs to Roth IRAs (conversions)

trustee-to-trustee transfers to another IRA

IRA-to-plan rollovers

plan-to-IRA rollovers

plan-to-plan rollovers

It shows the one rollover in a 12 month period rule was meant to limit the abuse of the 60 day rule because direct rollovers and trustee to trustee transfers are excluded.

What can be Rolled Over?

Most of the time the entire balance in a retirement account can be rolled over to another account unless the balance includes an amount of money that is required to be withdrawn. Examples include required minimum distributions and contributions in excess of limits (plus earnings on the excess contributions). For retirement plans, in addition to RMD's and excess contributions, any loans outstanding at the time of rollover or hardship distributions taken during the year will be subject to taxes and possible penalties.

Are Taxes Assessed at the Time of Distribution?

Distribution from an IRA: Typically, a tax is not assessed on a distribution from an IRA unless the account owner elects to have taxes withheld. A distribution from a pre-tax IRA account is typically subject to a 10% early withdrawal penalty if taken before 59 ½.

Distribution from Retirement Plan: Any distribution taken from a retirement plan where cash is made available to the owner is subject to a minimum 20% federal withholding. For example, if you request a $10,000 distribution, you will receive $8,000 and $2,000 will go to the government. There is no option to opt out of this withholding even if you intend to rollover the balance within 60 days. For this reason, a direct rollover would be a way to avoid the 20% withholding.

It is important to understand if you intend to rollover a distribution from a retirement account that the entire amount of the distribution must be redeposited within 60 days to avoid taxes and penalties even if taxes were already withheld. Using the previous example, if you take a $10,000 distribution from a retirement account and have the 20% withheld for taxes you must redeposit $10,000 within 60 days even though you only received $8,000 in cash. This scenario may appear that you are losing $2,000 but when you complete your taxes the $10,000 distribution will not be taxable as long as the full amount was redeposited within 60 days. When you file your taxes, the $2,000 will be included in the federal taxes withheld which is how the money is recouped.

How is the Rollover Reported to the Government?

Any time you wish to utilize the 60 day rule, it is important you keep documentation. Any distribution from a retirement account will generate a 1099-R form that must be reported as income on your tax return. Also, the 1099-R will show any taxes withheld from the distribution. You will receive a 1099-R even if a direct rollover or trustee to trustee transfer was done. The way the distribution is coded determines how the IRS treats it for tax purposes. If the distribution is coded as a direct rollover or trustee to trustee transfer, the distribution will not be treated as taxable income. If the distribution gave you access to cash, the 1099-R will be coded in a way that treats the distribution as a taxable event. If you redeposited the amount into another retirement account within 60 days, it is important you notify your tax preparer and bring documentation showing the deposit was made timely. The tax preparer should then treat the distribution as a non-taxable event.

About Rob.........

Hi, I'm Rob Mangold. I'm the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Simple IRA vs. 401(k) - Which one is right for your company?

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

compare simple ira and 401k

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

What are the company's primary goals for establishing the plan?

How much the owner(s) plan to contribute to the plan?

How many employees does the company have?

Do you want to restrict the plan to only full time employees?

The cost of maintaining each plan?

Does the company intend to make an employer contribution to the plan?

Diversity of the investment menu

Below is a chart that contains a quick comparison of some of the main features of each type of plan:

simple ira vs 401K comparison chart

For many small companies it often makes sense to start with a Simple IRA plan and then transition to a 401K plan as the company grows or when the owner intends to start accessing the upper deferral limits offered by the 401(k) plan.

Simple IRA's are relatively easy to setup and the administrative fees to maintain these plans are typically lower in comparison to 401(k) plans. Most Simple IRA providers will only charge $10 - $30 to custody the accounts.

By comparison, 401(k) plans are ERISA covered plans which require a TPA Firm (third party administrator) to maintain the plan documents, conduct year end plan testing, and file the 5500 each year. The TPA fees vary based on the provider and the number of employees eligible to participate in the plan. A ballpark range is $1,500 - $2,500 for companies with under 50 employees.

However, the additional TPA fees associated with establishing a 401(k) plan may be justified if:

The owners intend to max out their employee deferrals

The owners are approaching retirement and need to make big contributions

The company wants to maintain flexibility with the employer contribution

The company would like to make Roth contributions, loans, or rollovers available

WARNING: Most investment providers are "one trick ponies". They will talk about 401(k) plans and not present other options because they either do not have a thorough understand of how Simple IRA plans work or they are only able to offer 401(k) plans. Before establishing a retirement plan it is important to work with a firm that presents both options, helps you to understand the difference between the two types of plans, and assist you in evaluating which plan would best meet your company's goals and objectives.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

401(k) March 15th Deadline

For all companies that sponsor a 401(k) plan, the March 15th deadline is quickly approaching. March 15th is deadline for processing corrective distributions for failed actual deferred percentage (ADP) test. Failure to meet the deadline will result in a 10% excise penalty for any refund amounts that were due to the Highly Compensated Employees

401k march 15 deadline

For all companies that sponsor a 401(k) plan, the March 15th deadline is quickly approaching. March 15th is deadline for processing corrective distributions for failed actual deferred percentage (ADP) test. Failure to meet the deadline will result in a 10% excise penalty for any refund amounts that were due to the Highly Compensated Employees (HCE).

HCE’s are defined as an employee that is 5%+ owner or $115,000+ in annual compensation. The ADP test compares what the HCE’s deferred into the 401(k) versus what the Non-Highly Compensated Employees Deferred (NHCE). If there is too large of a gap between the average of the HCE’s versus the average of the NHCE, the plan is required to refund contributions to the HCE’s until the contribution level can pass testing. The typical rule of thumb is the HCE’s cannot defer more than 2% of the average of the NHCE’s to pass testing but this amount will vary based on the actual testing results.

If you are a safe harbor plan, you do not have to worry about the March 15th deadline because safe harbor plans are automatically deemed to pass the ADP test regardless of how much the HCE’s defer into plan. This makes safe harbor plans a very effective plan design for owners that are looking to max out their 401(k) deferrals in a given plan year.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.