Tax-Loss Harvesting Rules: Short-Term vs Long-Term, 30-Day Wash Rule, $3,000 Tax Deduction, and More…….

As an investment firm, November and December is considered “tax-loss harvesting season”, where we work with our clients to identify investment losses that can be used to offset capital gains that have been realized throughout the year to reduce their tax liability for the year. But there are a lot of IRS rules surrounding what “type” of realized losses can be used to offset realized gains, and retail investors are often unaware of these rules which can lead to errors in their lost harvesting strategies. In this article, we will cover loss harvesting rules for:

Realized Short-term Gains

Realized Long-term Gains

Mutual Fund Capital Gains Distributions

The $3,000 Annual Realized Loss Income Deduction

Loss Carryforward Rules

Wash Sale Rules

Real Estate Investments

Business Gains or Losses

Short-Term vs Long-Term Gain and Losses

Investment gains and losses fall into two categories: Long-Term and Short-Term. Any investment, whether it’s a stock, mutual fund, or real estate, if you buy it and then sell it within 12 months, that gain or loss is classified as a “short-term” capital gain or loss and is taxed to you as ordinary income.

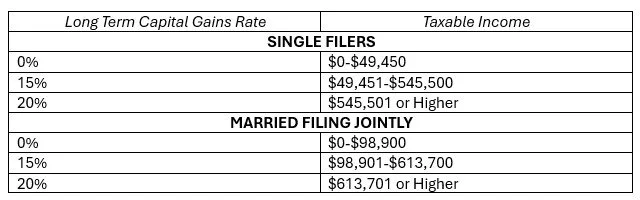

If you make an investment and hold it for more than 1 year before selling it, your gain or loss is classified as a “long-term” capital gain or loss. If it’s a gain, it’s taxed at the preferential long-term capital gains rates. The long-term capital gains tax rate that you pay varies based on the amount of your income for the year (including the amount of the long-term capital gain). For 2026, here is the table:

Note: For individuals in the top tax bracket, there is a 3.8% Medicare surcharge added on top of the federal 20% long-term capital gains tax rate, so the top long-term capital gains rate ends up being 23.8%. For individuals that live in states with income tax, many do not have special tax rates for long-term capital gains and they are simply taxed as additional ordinary income at the state level.

What Is Year End Loss Harvesting?

Loss harvesting is a tax strategy where investors intentionally sell investments that have lost value to generate a realized loss to offset a realized gain that they may have experienced in another investment. Example, if a client sold Nvidia stock in May 2025 and realized a long-term capital gain of $100,000 in November and they look at their investment portfolio an notice that their Plug Power stock has an unrealized loss of $100,000, if they sell the Plug Power stock and generate a $100,000 realized loss, it would completely wipes out the tax liability on the $100,000 gain that they realized on the sale of their Nvidia stock earlier in the year.

Loss harvesting is not an all or nothing strategy. In that same example above, even if that client only had $30,000 in unrealized losses in Plug Power, realizing the loss would at least offset some of the $100,000 realized gain in their Nvidia stock sale.

Long-Term Losses Only Offset Long-Term Gains

It's common for investors to have both short-term realized capital gains and long-term realized capital gains in a given tax year. It’s important for investors to understand that there are specific IRS rules as to what TYPE of investment losses offset investment gains. For example, realized long-term losses can only be used to offset realized long-term capital gains. You cannot use realized long-term losses to offset a short-term capital gain.

Short-Term Losses Can Offset Both Short-Term & Long-Term Gain

However, realized short-term losses can be used to offset EITHER short-term or long-term capital gains. If an investor has both short-term and long-term gains, the short-term realized losses are first used to offset any short-term gains, and then the remainder is used to offset the long-term gains.

Loss Carryforward

What happens when your realized loss is greater than your realized gain? You have what’s called a “loss carryforward”. If you have unused realized investment losses, those unused losses can be used to offset investment gains in future tax years. Example, Joe sells company XYZ and has a $30,000 realized long-term loss. The only other investment income that Joe has is a short-term gain of $5,000. Since you cannot use a long-term loss to offset a short-term gain, Joe’s $30,000 in realized long-term losses cannot be used in this tax year. However, that $30,000 loss will carryforward to the next tax year, and if Joe has a long-term realized gain of $40,000 that next year, he can use the $30,000 carryforward loss to offset a larger portion of that $40,000 realized gain.

When do carryforward losses expire? Answer: never (except for when you pass away). The carryforward loss will continue until you have a gain to offset it.

$3,000 Capital Loss Annual Tax Deduction

Even if you have no realized capital gains for the year, it may still make sense from a tax standpoint to generate a $3,000 realized loss from your investment accounts because the IRS allows you deduct up to $3,000 per year in capital losses against your ordinary income. Both short-term and long-term losses qualify toward that $3,000 annual tax deduction.

Example: Sarah has no realized capital gains for the year, but on December 15th she intentionally sells shares of a mutual fund to generate a $3,000 long-term realized loss. Sarah can now use that $3,000 loss to take a deduction against her ordinary income.

Tax Note: You do not need to itemize to take advantage of the $3,000 tax deduction for capital losses. You can elect to take the standard deduction when filing your taxes and still capture the $3,000 tax deduction for capital losses.

The $3,000 annual loss tax deduction can also be used to eat up carryforward losses. If we go back to our example with Joe who had the $30,000 realized long-term loss, if he does not have any future capital gains to offset them with the carryforward loss, he could continue to deduct $3,000 per year against his ordinary income over the next 10 years, until the loss has been fully deducted.

Mutual Fund Capital Gain Distribution

For investors that use mutual funds as an investment vehicle within a taxable investment account, certain mutual funds will issue a “capital gains distribution”, typically in November or December of each year, which then generates taxable income to the shareholder of that mutual fund, whether they sold any shares during the year.

When mutual funds issue capital gains distributions, it’s common that a majority of the capital gains distributions will be long-term capital gains. Similar to normal realized long-term capital gains, investors can loss harvest and generate realized losses to offset the long-term capital gains distribution from their mutual fund holdings in an effort to reduce their tax liability.

The Wash Sale Rule

When loss harvesting, investors have to be aware of the IRS “Wash Sale Rule”. The wash sale rule states that if you sell a security at a loss and the rebuy a substantially identical security within 30 days following the date of the sale, a realized loss cannot be captured by the taxpayer.

Example: Scott sells the Nike stock on December 1, 2026 which generates a $10,000 realize loss, but then Scott repurchases Nike stock on December 25, 2025. Since Scott repurchased Nike stock within 30 days of the sell day, he can no longer use the $10,000 realized loss generated by his sell transaction on December 1st due to the IRS 30 Day Wash Rule.

Also make note of the term “substantially identical” security. If you sell the Vanguard S&P 500 Index ETF to realize a loss but then purchase the Fidelity S&P 500 Index ETF 15 days later, while they are two different investments with different ticker symbols, the IRS would most likely consider them substantially identical triggering the Wash Sale rule.

Real Estate & Business Loss Harvesting

While most of the examples today have been centered around stock investments, the lost harvesting strategy can be used across various asset classes. We have had clients that have sold their business, generating a large long-term capital gain, and then we have them going into their taxable brokerage account looking for investment holdings that have unrealized losses that we can realize to offset the taxable long-term gain from the sale of their business.

The same is true for real estate investments. If a client sells a property at a gain, they may be able to use either carryforward losses from previous tax years or intentionally realize losses in their investment accounts in the same tax year to offset the taxable gain from the sale of their investment property.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is tax-loss harvesting?

Tax-loss harvesting is a year-end tax strategy where investors sell investments that have declined in value to realize a loss that can be used to offset realized capital gains for the year. For example, if you realized a $100,000 gain from one stock, selling another stock with a $100,000 loss could eliminate the tax liability from that gain.

What is the difference between short-term and long-term capital gains and losses?

Short-term gains or losses come from investments held for one year or less and are taxed as ordinary income. Long-term gains or losses come from investments held for more than one year and qualify for lower, preferential long-term capital gains tax rates.

Can long-term losses offset short-term gains?

No. Realized long-term losses can only be used to offset realized long-term gains. However, realized short-term losses can be used to offset both short-term and long-term capital gains.

What happens if my realized losses are greater than my gains?

If your realized losses exceed your gains, the remaining amount becomes a loss carryforward. You can carry forward unused losses indefinitely and use them to offset future realized gains.

What is the $3,000 capital loss deduction?

Even if you have no capital gains, you can deduct up to $3,000 in realized capital losses per year against ordinary income. For married couples filing separately, the limit is $1,500. Any remaining unused losses can continue to carry forward to future tax years.

What are mutual fund capital gain distributions?

Mutual funds often distribute capital gains to shareholders at the end of the year, usually in November or December. These distributions create taxable income for the investor—even if no shares were sold. Tax-loss harvesting can help offset the tax impact of these mutual fund capital gains distributions.

What is the wash sale rule?

The IRS wash sale rule disallows a realized loss if you sell a security at a loss and buy a “substantially identical” security within 30 days before or after the sale. For instance, selling a Vanguard S&P 500 Index ETF and repurchasing a similar Fidelity S&P 500 ETF within 30 days would likely violate the wash sale rule.

Do loss harvesting rules apply to real estate and business sales?

Yes. The same loss-harvesting concept can apply when selling real estate or a business at a gain. Investors can use realized losses from their taxable brokerage accounts or carryforward losses from prior years to offset taxable gains from these sales.