Where Are We In The Market Cycle?

Before you can determine where you are going, you first have to know where you are now. Seems like a simple concept. A similar approach is taken when we are developing the investment strategy for our client portfolios. The question more specifically that we are trying to answer is “where are we at in the market cycle?” Is there more upside

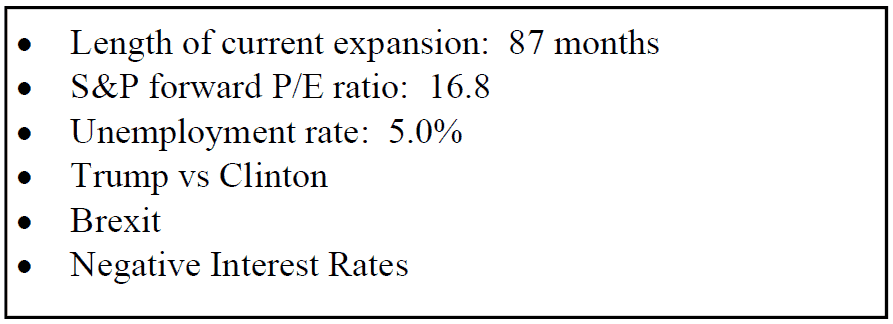

Before you can determine where you are going, you first have to know where you are now. Seems like a simple concept. A similar approach is taken when we are developing the investment strategy for our client portfolios. The question more specifically that we are trying to answer is “where are we at in the market cycle?” Is there more upside to the market? Is there a downturn coming? No one knows for sure and there is no single market indicator that has proven to be an accurate predicator of future market trends. Instead, we have to collect data on multiple macroeconomic indicators and attempt to plot where we are in the current market cycle. Here is a snapshot of where we are at now:

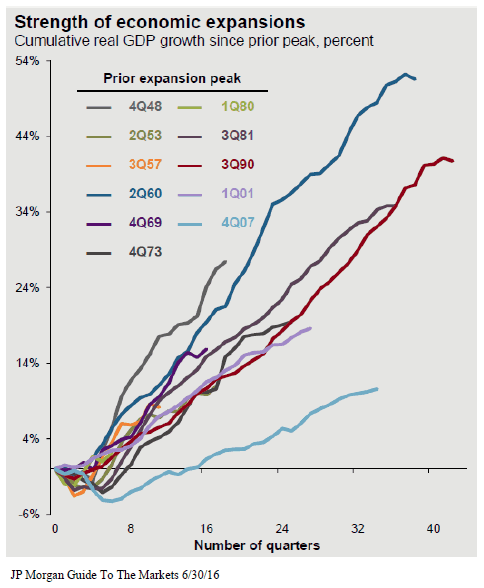

The length of the current bull market is starting to worry some investors. Living through the tech bubble and the 2008 recession, those were healthy reminders that markets do not always go up. We are currently in the 87th month of the expansion which is the 4th longest on record. Since 1900, the average economic expansion has lasted 46 months. This leaves many investors questioning, “is the bull market rally about to end?” We are actually less concerned about the “duration” of the expansion. We prefer to look at the “magnitude” of the expansion. This recovery has been different. In most economic recoveries the market grows rapidly following a recession. If you look at the magnitude of this expansion that started in the 4th quarter of 2007 versus previous expansions, it has been lackluster at best. See the chart on the next page. This may lead investors to conclude that there is more to the current economic expansion.

Next up, employment. Over the past 50 years, the unemployment rate has averaged 6.2%. We are currently sitting at an unemployment rate of 5.0%. Based on that number it may be reasonable to conclude that we are close to full employment. Once you get close to full employment you begin to lose that surge in growth that the economy receives from adding 250,000+ jobs per month. It may also imply that we are getting closer to the end of this market cycle.

Now let’s look at the valuation levels in the stock market. In other words, in general are the stocks in the S&P 500 Index cheap to buy, fairly valued, or expensive to buy at this point? We measure this by the forward price to earning ratio (P/E) of the S&P 500 index. The average P/E of the S&P 500 over the last 25 years is 15.9. Back in 2008, the P/E of the S&P 500 was around 9.0. From a valuation standpoint, back in 2008, stocks were very cheap to buy. When stocks are cheap, investors tend to hold them regardless of what’s happening in the global economy with the hopes that they will at least become “fairly valued” at some point in the future. Right now the P/E Ratio of the S&P 500 Index is about 16.8 which is above the 15.9 historic average. This may indicate that stock are starting to become “expensive” from a valuation standpoint and investors may be tempted to sell positions during periods of volatility.

Even though stocks may be perceived as “overvalued” that does not necessarily mean they are not going to become more overvalued from here. In fact, often times after long bull rallies “the plane will overshoot the runway”. However, it does typically mean that big gains are harder to come by since a large amount of the future earnings expectations of the S&P 500 companies are already baked into the stock price. It leaves the door open for more quarterly earning disappointments which could rise to higher levels of volatility in the markets.

The most popular question of the year goes to: “Trump or Hillary? And how will the outcome impact the stock market?” I try not to get too deep in the weeds of politics mainly because history has shown us that there is no clear evidence whether the economy fares better under a Republican president or a Democratic president. However, here is the key point. Markets do not like uncertainty and one of the candidates that is running (I will let you guess which one) represents a tremendous amount of uncertainty regarding the actions that they may take if elected president of the United States. Still, under these circumstances, it is very difficult to develop a sound investment strategy centered around political outcomes that may or may not happen. We really have to “wait and see” in this case.

Let’s travel over the Atlantic. Brexit was a shock to the stock market over the summer but the long term ramifications of the United Kingdom’s exit from the European Union is yet to be known. The exit process will most likely take a number of years as the EU and the UK negotiate terms. In our view, this does not pose an immediate threat to the global economy but it will represent an ongoing element of uncertainty as the EU continues to restart sustainable economic growth in the region.

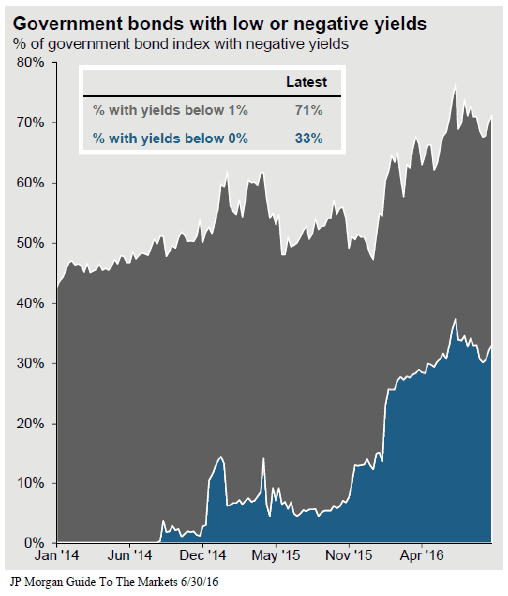

The chart below is one of the most important illustrations that allows us to gauge the overall level of risk that exists in the global economy. When a country wants to jump start its economy it will often lower the reserve rate (similar to our Fed Funds Rate) in an effort to encourage lending. An increase in borrowing hopefully leads to an increase in consumer spending and economic growth. Unfortunately, countries around the globed have taken this concept to an extreme level and have implemented “negative rates”. If you buy a 10 year government bond in Germany or Japan, you are guaranteed to lose money over that 10 year period. If you have a checking account at a bank in Japan, instead of receiving interest from the bank, the bank may charge you a fee to hold onto your own money. Crazy right? It’s happening. In fact, 33% of the countries around the world have a negative yield on their 10 year government bond. See the chart below. When you look around the globe 71% of the countries have a 10 year government bond yield below 1%. The U.S. 10 Year Treasury sits just above that at 1.7%.

So, what does that mean for the global economy? Basically, countries around the world are starving for economic growth and everyone is trying to jump start their economy at the same time. Possible outcomes? On the positive side, the stage is set for growth. There is “cheap money” and favorable interest rates at levels that we have never seen before in history. Meaning a little growth could go a long ways.

On the negative side, these central banks around the global are pretty much out of ammunition. They have fired every arrow that they have at this point to prevent their economy from contracting. If they cannot get their economy to grow and begin to normalize rates in the near future, when they get hit by the next recession they will have nothing to combat it with. It’s like the fire department showing up to a house fire with no water in the truck. The U.S. is not immune to this situation. Everyone wants the Fed to either not raise rates or raise rates slowly for the fear of the negative impact that it may have on the stock market or the value of the dollar. But would you rather take a little pain now or wait for the next recession to hit and have no way to stop the economy from contracting? It seems like a risky game.

When we look at all of these economic factors as a whole it suggests to us that the U.S. economy is continuing to grow but at a slower pace than a year ago. The data leads us to believe that we may be entering the later stages of the recent bull market rally and that now is a prudent time to revisit the level of exposure to risk assets in our client portfolios. At this point we are more concerned about entering a period of long term stagnation as opposed to a recession. With the rate of economic growth slowing here in the U.S. and the rich valuations already baked into the stock market, we could be entering a period of muted returns from both the stock and bond market. It is important that investors establish a realistic view of where we are in the economic cycle and adjust their return expectations accordingly.

As always, please feel free to contact me if you’d like to discuss your portfolio or our outlook for the economy.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Market Alert - UK Votes To Exit EU

We have been working through the night to monitor the UK exit vote in Europe and wanted to get this information out as soon as possible.Today is a historic day. Last night the UK voted whether or not to leave the European Union. The polls closed at 10 p.m. last night, the votes were counted, and at 2 a.m. this morning it was announced that the UK had

We have been working through the night to monitor the UK exit vote in Europe and wanted to get this information out as soon as possible.Today is a historic day. Last night the UK voted whether or not to leave the European Union. The polls closed at 10 p.m. last night, the votes were counted, and at 2 a.m. this morning it was announced that the UK had voted 51.9% in favor of leaving the EU. To put this situation in context, this would be similar to New York deciding to leave the United States to form its own country.

This was not the expected outcome and is largely an unprecedented event. Going into the vote yesterday most polls expected the UK “stay” vote to prevail given the economic headwinds that the UK would face if the “leave” vote were to win. David Cameron, the prime minister of the UK, was largely in favor of the UK staying in the EU. Today at 3:30 a.m., Cameron announced that he would step down as the prime minister since new leadership, that is in favor of the exit, should be in place to negotiate Britain’s exit from the EU.

The European Union (EU) is made up of 28 countries. It was originally formed back in 1957 with the goal of preventing wars and strengthening the economic bond between the European countries in its membership. The UK joined the EU in 1973. Members of the EU benefit from:

Freedom of movement between countries

Freedom of trade for goods, services, and capital

EU human rights protection

Euro currency (the UK does not participate in the euro currency)

The Argument To Stay In The EU

Supporters of the UK to stay in the EU believe that the Union is better for the British economy and that concerns about migration and other issues stemming from EU membership are not important enough to outweigh the economic consequences of leaving. Many economists agree with this claim. Europe is Britain’s most important export market and its greatest source of foreign direct investment. An exit of the EU could jeopardize its financial status in the world and the high paying jobs that come with that status.

Those who voted to stay were not necessarily defending the EU but were basically arguing that the UK is stronger with the EU than without.

Argument To Leave The EU

Those in favor of the UK leaving the EU believe that leaving the European Union is necessary for the UK to restore the country’s identity. Immigration has been one of the largest issue on the agenda with refugees entering the UK under the EU’s permission and “taking jobs” in the place of UK citizens. Voters in the middle to lower income classes are viewed as more likely to support leaving the Union due to a feeling of being “abandoned by their country” in lieu of the EU policies.

In a way Britain feels like they used to matter to the world as an independent country but over the years have lost their identity now that they are lumped into the EU. This group of individuals wants to be able to have full control over the country’s economic policy, culture, political system, and judicial system.

What Happens Next?

Now that the UK has voted to leave the EU, it has become clear that there needs to be new leadership in government that supports the UK exit since most of the current leaders, including the prime minister, were in favor of the UK staying in the EU. We would expect this to happen in a fairly short period of time.

Once the new leadership is in place, the negotiation will begin between the UK and the EU for the exit. There is not a precedence for this process which leaves a lot of unknowns. Immediately, nothing changes. Most likely while the negotiations are taking place over the course of next few months, or more likely years since the UK is still technically an EU member, UK citizens will still be able to move about the Eurozone countries freely, trade will continue, etc.

However, there will most likely be an immediate negative impact on the UK economy given the expectation of the exit. The British pound (currency) will most likely drop significantly. The profitability of the multinational companies and banks that are headquartered in the UK will come into question since they will eventually lose the benefits of free trade and capital movements with other EU countries.

Overall we are entering a period of increased uncertainty. Unfortunately, in our view, there is a larger issue at hand. Yes, the UK exiting the EU is a significant event but the larger issue is for the first time they are laying the ground work that will allow a country to exit the EU. There are other countries in the EU that may take up similar votes to leave the European Union since a precedence is now being set for the UK to exit. If the entire EU were to further destabilize it would most likely cause further disruption across the global economy.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Backdoor Roth IRA Contribution Strategy

This strategy is for high income earners that make too much to contribute directly to a Roth IRA. In recent years, some of these high income earners have been implementing a “backdoor Roth IRA conversion strategy” to get around the Roth IRA contribution limitations and make contributions to Roth IRA’s via “conversions”. For the 2020 tax year, your

backdoor roth ira strategy

This strategy is for high income earners that make too much to contribute directly to a Roth IRA. In recent years, some of these high income earners have been implementing a “backdoor Roth IRA conversion strategy” to get around the Roth IRA contribution limitations and make contributions to Roth IRA’s via “conversions”. For the 2021 tax year, your ability to make contributions to a Roth IRA begins to phase out at the following AGI thresholds based on your filing status:

Single: $125,000

Married Filing Jointly: $198,000

Married Filing Separately: $0

However, in 2010 the IRS removed the income limits on “IRA Conversions” which open up an opportunity……if executed correctly…….for high income earners to make “backdoor” contributions to a Roth IRA.

Why would a high income earning want to contribute to a Roth IRA? Once high income earners have maxed out their contributions to their employer sponsored retirement plans, they usually begin to fund plain vanilla investment management accounts or whole life insurance policies. When assets accumulate in an investment management account, once liquidated, the account owner typically has to pay either short-term or long term capital gains on the appreciation. For whole life insurance, even though the accumulation is tax deferred, if the policy is surrendered, the policy owner pays ordinary income tax on the gain in the policy.

With a Roth IRA, after tax contributions are made to the account and the gains in the account are withdrawn TAX FREE if the account owner at the time of withdrawal is over the age of 59½ and the Roth IRA has been in existence for 5 years. A huge tax benefit for high income earners who are typically in a medium to higher tax bracket even in retirement.

Here is how the strategy works

Rollover all existing pre-tax IRA’s into your employer sponsored retirement plan

Make a non-deductible contribution to a Traditional IRA

Convert the Traditional IRA to a Roth IRA

Here are the pitfalls in the execution process

Over the years, more and more individuals have become aware of this wealth accumulation strategy. However, there are risks associated with executing this strategy and if not executed correctly could result in adverse tax consequences.

Here are the top pitfalls:

Forget to aggregate Pre-Tax IRA’s

Do not understand that SEP IRA’s and Simple IRA’s are included in the Aggregation Rule

They create a “step transaction”

Pitfall #1: IRS Aggregation Rule

The IRA aggregate rule stipulates that when an individual has multiple IRAs, they will allbe treated as one account when determining the tax consequences of any distributions (including a distribution out of the account for a Roth conversion).

This creates a significant challenge for those who wish to do the backdoor Roth strategy, but have otherexisting IRA accounts already in place (e.g., from prior years’ deductible IRA contributions, or rollovers from prior 401(k) and other employer retirement plans). Because the standard rule for IRA distributions (and Roth conversions) is that any after-tax contributions come out along with any pre-tax assets (whether from contributions or growth) on a pro-rata basis, when all the accounts are aggregated together, it becomes impossible to justconvert the non-deductible IRA.

picture

If an individual has pre-tax IRA’s we typically recommend that they rollover those IRA’s into their employer sponsored retirement plans which eliminates all of their pre-tax IRA balance and then open the opportunity to execute this backdoor Roth IRA contribution strategy.

Pitfall #2: SEP IRA & Simple IRA's count

Many smaller companies and self-employed individuals sponsor SEP IRA’s or Simple IRA Plans. Many individuals just assume that these are “employer sponsored retirement plans” not subject to the aggregation rules. Wrong. In the eyes of the IRS these are “pre-tax IRA’s” and are subject to the aggregation rules. If you have a Simple IRA or SEP IRA, make sure you take this common pitfall into account.

Pitfall #3: Beware IRS Step Transaction Rule

This is probably the most common pitfall that we see when executing this strategy. Individuals and investment advisors alike will make deposits to the non-deductible traditional IRA and then the next day process the conversion to the Roth IRA. In doing this, you run the risk of creating a “step transaction”.

There is a very long explanation tied to “step transactions” and how to avoid a “step transactions” but I will provide you with a brief summary of the concept.

Here it is, if you use legal loop holes in the tax system in an obvious effort to side step other IRS limitations (like the Roth IRA income limit) it could be considered a “step transaction” by the IRS and the IRS may disallow the conversion and assess tax penalties.

Disclosure: Backdoor Roth IRA Conversion Strategy

It is highly recommend that you work closely with your financial advisor and tax advisor to determine whether or not this is a viable wealth accumulation strategy based on your personal financial situation.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Simple IRA vs. 401(k) - Which one is right for your company?

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

compare simple ira and 401k

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

What are the company's primary goals for establishing the plan?

How much the owner(s) plan to contribute to the plan?

How many employees does the company have?

Do you want to restrict the plan to only full time employees?

The cost of maintaining each plan?

Does the company intend to make an employer contribution to the plan?

Diversity of the investment menu

Below is a chart that contains a quick comparison of some of the main features of each type of plan:

simple ira vs 401K comparison chart

For many small companies it often makes sense to start with a Simple IRA plan and then transition to a 401K plan as the company grows or when the owner intends to start accessing the upper deferral limits offered by the 401(k) plan.

Simple IRA's are relatively easy to setup and the administrative fees to maintain these plans are typically lower in comparison to 401(k) plans. Most Simple IRA providers will only charge $10 - $30 to custody the accounts.

By comparison, 401(k) plans are ERISA covered plans which require a TPA Firm (third party administrator) to maintain the plan documents, conduct year end plan testing, and file the 5500 each year. The TPA fees vary based on the provider and the number of employees eligible to participate in the plan. A ballpark range is $1,500 - $2,500 for companies with under 50 employees.

However, the additional TPA fees associated with establishing a 401(k) plan may be justified if:

The owners intend to max out their employee deferrals

The owners are approaching retirement and need to make big contributions

The company wants to maintain flexibility with the employer contribution

The company would like to make Roth contributions, loans, or rollovers available

WARNING: Most investment providers are "one trick ponies". They will talk about 401(k) plans and not present other options because they either do not have a thorough understand of how Simple IRA plans work or they are only able to offer 401(k) plans. Before establishing a retirement plan it is important to work with a firm that presents both options, helps you to understand the difference between the two types of plans, and assist you in evaluating which plan would best meet your company's goals and objectives.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Comparing Different Types of Employer Sponsored Retirement Plans

Employer sponsored retirement plans are typically the single most valuable tool for business owner when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

But with all of the different types of plans to choose from which one is the right one for your business? Most business owners are familiar with how 401(k) plans work but that might not be the right fit given variables such as:

comparison of different types of retirement plans

Employer sponsored retirement plans are typically the single most valuable tool for business owner when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

But with all of the different types of plans to choose from which one is the right one for your business? Most business owners are familiar with how 401(k) plans work but that might not be the right fit given variables such as:

# of Employees

Cash flows of the business

Goals of the business owner

There are four main stream employer sponsored retirement plans that business owners have to choose from:

SEP IRA

Single(k) Plan

Simple IRA

401(k) Plan

Since there are a lot of differences between these four types of plans we have included a comparison chart at the conclusion of this newsletter but we will touch on the highlights of each type of plan.

SEP IRA PLAN

This is the only employer sponsored retirement plan that can be setup after 12/31 for the previous tax year. So when you are sitting with your accountant in the spring and they deliver the bad news that you are going to have a big tax liability for the previous tax year, you can establish a SEP IRA up until your tax filing deadline plus extension, fund it, and take a deduction for that year.

However, if the company has employees that meet the plan’s eligibility requirement, these plans become very expensive very quickly if the owner(s) want to make contributions to their own accounts. The reason being, these plans are 100% employer funded which means there are no employee contributions allowed and the employer contribution is uniform for all plan participants. For example, if the owner contributes 15% of their income to the SEP IRA, they have to make an employer contribution equal to 15% of compensation for each employee that has met the plans eligibility requirement. If the 5305-SEP Form, which serves as the plan document, is setup correctly a company can keep new employees out of the plan for up to 3 years but often times it is either not setup correctly or the employer cannot find the document.

Single(k) Plan or “Solo(k)”

These plans are for owner only entities. As soon as you have an employee that works more than 1000 hours in a 12 month period, you cannot sponsor a Single(k) plan.

The plans are often times the most advantageous for self-employed individuals that have no employees and want to have access to higher pre-tax contribution levels. For all intensive purposes it is a 401(k) plan, same contributions limits, ERISA protected, they allow loans and Roth contributions, etc. However, they can be sponsored at a much lower cost than traditional 401(k) plans because there are no non-owner employees. So there is no year-end testing, it’s typically a boiler plate plan document, and the administration costs to establish and maintain these plans are typically under $400 per year compared to traditional 401(k) plans which may cost $1,500+ per year to administer.

The beauty of these plans is the “employee contribution” of the plan which gives it an advantage over SEP IRA plans. With SEP IRA plans you are limited to contributes up to 25% of your income. So if you make $24,000 in self-employment income you are limited to a $6,000 pre-tax contribution.

With a Single(k) plan, for 2016, I can contribute $18,000 per year (another $6,000 if I’m over 50) up to 100% of my self-employment income and in addition to that amount I can make an employer contribution up to 25% of my income. In the previous example, if you make $24,000 in self-employment income, you would be able to make a salary deferral contribution of $18,000 and an employer contribution of $6,000, effectively wiping out all of your taxable income for that tax year.

Simple IRA

Simple IRA’s are the JV version of 401(k) plans. Smaller companies that have 1 – 30 employees that are looking to start a retirement plan will often times start with implementing a Simple IRA plan and eventually graduate to a 401(k) plan as the company grows. The primary advantage of Simple IRA Plans over 401(k) Plans is the cost. Simple IRA’s do not require a TPA firm since they are self-administered by the employer and they do not require annual 5500 filings so the cost to setup and maintain the plan is usually much less than a 401(k) plan.

What causes companies to choose a 401(k) plan over a Simple IRA plan?

Owners want access to higher pre-tax contribution limits

They want to limit to the plan to just full time employees

The company wants flexibility with regard to the employer contribution

The company wants a vesting schedule tied to the employer contributions

The company wants to expand the investment menu beyond just a single fund family

401(k) Plans

These are probably the most well recognized employer sponsored plans since at one time or another each of us has worked for a company that has sponsored this type of plan. So we will not spend a lot of time going over the ins and outs of these types of plan. These plans offer a lot of flexibility with regard to the plan features and the plan design.

We will issue a special note about the 401(k) market. For small business with 1 -50 employees, you have a lot of options regarding which type of plan you should sponsor but it’s our personal experience that most investment advisors only have a strong understanding of 401(k) plans so they push 401(k) plans as the answer for everyone because it’s what they know and it’s what they are comfortable talking about. When establishing a retirement plan for your company, make sure you consult with an advisor that has a working knowledge of all these different types of retirement plans and can clearly articulate the pros and cons of each type of plan. This will assist you in establishing the right type of plan for your company.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.