How to Title Your House To Avoid Probate

When we are working with clients on their estate plan, one of the primary objectives is to assist them with titling their assets so they avoid the probate process after they pass away. For anyone that has had to serve as the executor of an estate, you have probably had firsthand experience of how much of a headache the probate processes which is why it's typically a goal of an estate plan to avoid the probate process altogether.

When we are working with clients on their estate plan, one of the primary objectives is to assist them in titling their assets so they avoid the probate process after they pass away. For anyone that has had to serve as the executor of an estate, you have probably had firsthand experience with how much of a headache the probate process is. For that reason, it's typically a goal of an estate plan to avoid the probate process altogether.

While it’s fairly easy to protect an IRA, a brokerage account, bank accounts, and life insurance policies from the probate process, it has historically been more difficult to protect the primary residence from the probate process without setting up a trust to own the house.

But there is good news on this front, especially for residents of New York State. As of July 2024, New York allows residence to add a Transfer on Death (TOD) designation to their deed. Adding a TOD designation is like naming beneficiaries on an IRA account or brokerage account. Prior to July 2024, residents of New York State were not allowed to add a TOD designation to a deed for real estate, so their only ways to protect their house from the probate process was:

Gift the house to their child before they die (Not a good option)

Gift the house with a life estate (Ok….but not great)

Set up either a Revocable or Irrevocable Trust to own the house

Those three options are still available but now there is a fourth option which is simple and costs less money than setting up a trust. Change the deed on your house to a “TOD deed”.

32 States Now Allow TOD Deeds

While New York just made this option available in 2024, there were already 31 other states that already allowed residents to add a TOD designation to their deed. Depending on which state you live in, a simple Google search or contacting a local estate attorney, will help you determine if your state offers the TOD deed option.

What Is The Probate Process?

Why is it a common goal of an estate plan to have your assets avoid the probate process? The probate process can be expensive and time consuming depending on what state you live in. In New York, the state that we are located in, it’s a headache. Any asset that is not owned by a trust or does not have beneficiaries directly assigned to it, pass to your beneficiaries through your will. The process of moving assets from your name (the decedent) to the beneficiaries of your estate, it a formal legal process called the “probate process”.

It is not as easy as when someone passes away with a house, they just look at their will which list their children as beneficiaries of their estate, and then the ownership of the house is transferred to the kids the next day. The probate process is a formal legal process in which the court system is involved, an estate attorney may need to be hired to help the executor through the probate process, an accountant may need to be hired to file an estate tax return, an appraiser may need to be hired to value real estate holdings, and investment advisors may be involved to help retitle assets to the beneficiaries. All of this costs money and takes time to navigate the process. We have seen some estates take years to settle before the beneficiaries receive their inheritance.

How Assets Pass to Beneficiaries of an Estate

There are three ways that assets pass to a beneficiary of an estate:

Probate

By Contract

By Trust

Assets That Pass By Contract

Assets that pass “by contract” to beneficiaries of an estate avoid the probate process because there are beneficiaries contractually designated on those accounts. Examples of these types of assets are retirement accounts, IRAs, annuities, life insurance policies, and an asset with a TOD designation like a brokerage account, bank account, or a house with a TOD deed. For these types of assets, you simply look at the beneficiary form that was completed by the account owner, and that's who the account passes to immediately after the decedent passes away. It does NOT pass by the decedent’s will.

Example: Someone could list their two children as 50/50 beneficiaries of their estate in their will but if they list their cousin as their 100% primary beneficiary on their IRA, when they pass away, that IRA balance will go 100% to their cousin because IRA assets transfer by contract and not through the probate process. Any assets that go through the probate process are distributed in accordance with a person’s will.

Asset That Pass By Trust

One of the primary reasons for an individual to set up either a revocable trust or irrevocable trust to own their house or other assets is to avoid the probate process, because assets that are owned by a trust pass directly to the beneficiaries listed in the trust document outside of the will. Example: your brokerage account is owned by your Revocable Trust, when you pass away, the assets can be immediately distributed to the beneficiaries listed in the trust document without going through the probate process. The beneficiaries listed in your trust document may or may not be different than the beneficiaries listed in your will.

House With A Transfer of Death Deed

Prior to New York allowing residents to attach a TOD designation to the deed on their house, the only options for titling the house to avoid the probate process were to:

Gift the house to the kids before they pass (not a good option)

Gifting the house with a life estate

Setting up a trust to own the house

The most common solution was setting up a trust to own the house which costs money because you typically have to engage an estate attorney to draft the trust document. If the ONLY objective of establishing the trust was for the house to avoid probate, the new TOD deed option could replace that option and be an easier, more cost-effective option going forward.

How To Change The Deed to a TOD Deed

Changing the deed on your house to a TOD deed is very simple. You just need to file the appropriate form at your County Clerk’s Office. The TOD designation on your house does not become official until it has been formally filed with the County Clerk’s Office.

What If You Still Have A Mortgage?

Having a mortgage against your primary residence should not preclude you from changing your current deed to a TOD deed. Even after you file the TOD deed, you still own the house, the bank still maintains a lien against your house for the outstanding amount, and even if you pass and the house transfers to the kids via the TOD designation, it does not remove the lien that the bank has against the property. If the kids tried to sell the house after you pass, they would first need to satisfy the outstanding mortgage, potentially with proceeds from the sale of the house.

The TOD Deed Does Not Protect The House From Medicaid

While changing the deed on your house to a TOD deed will successfully help the house to avoid the probate process, it does not protect the house from a future long-term care event. While the primary residence is not a countable asset for Medicaid, Medicaid, depending on the county that you live in, could put a lien against your house for the amount that they paid to the nursing home for your long-term care. Individuals that want to fully protect their house from a future long-term care event will often set up an Irrevocable Trust, otherwise known as a Medicaid Trust, to own their house to avoid these Medicaid liens. That is an entirely different but important topic that we have a separate article on. If you are looking for more information on how to protect your house from probate AND a long-term care event, here are our articles on those topics:

Article: Gifting Your House with a Life Estate vs Medicaid Trust

Article: Don’t Gift Your House To Your Children!!

Article: How to Protect Assets From A Nursing Home

Changing the House TOD Beneficiaries

The question frequently comes up during our estate planning meetings, “What if I change my mind on who I want listed as the beneficiary of my house?” With a TOD Deed, it’s an easy change. You just go back to the County Clerks Office and file a new TOD Deed with your updated beneficiary designations. Remember, once you Change the deed to a TOD deed, the house no longer passes in accordance with your will, it passes by contract to the beneficiaries list on that TOD designation.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is a Transfer on Death (TOD) deed?

A Transfer on Death (TOD) deed allows you to name beneficiaries who will automatically inherit your home when you pass away—without having to go through probate. It works similarly to naming beneficiaries on an IRA, bank, or brokerage account.

Does New York State allow TOD deeds?

Yes. As of July 2024, New York residents can add a TOD designation to their property deed. Before this change, homeowners in New York had to use trusts or life estates to avoid probate. New York now joins 31 other states that already allow TOD deeds.

Why should I want to avoid probate?

The probate process can be costly and time-consuming. It often requires attorneys, accountants, and court filings before beneficiaries can receive their inheritance. In some cases, estates can take years to settle. A TOD deed allows real estate to transfer immediately to beneficiaries, avoiding this process entirely.

How do assets pass to beneficiaries?

Assets can pass three ways: through probate (by will), by contract (through named beneficiaries), or by trust. TOD deeds fall under the “by contract” category, which means the property goes directly to the listed beneficiaries without court involvement.

How is a TOD deed different from a trust?

A TOD deed is simpler and less expensive to set up than a trust. It only applies to real estate, while a trust can manage multiple types of assets. For homeowners who only want to avoid probate on their house, a TOD deed may be an easier solution than creating a trust.

How do you file a TOD deed in New York?

You must complete and file the appropriate form with your County Clerk’s Office. The TOD designation is not valid until it has been officially recorded by the county. Once filed, your home will automatically transfer to the listed beneficiaries when you pass away.

Can you still file a TOD deed if you have a mortgage?

Yes. Having a mortgage doesn’t prevent you from using a TOD deed. The bank’s lien on the property remains in place, and your beneficiaries will need to pay off or refinance the loan if they sell or keep the property after your death.

Does a TOD deed protect your home from Medicaid?

No. A TOD deed only avoids probate—it does not protect the property from potential Medicaid liens for long-term care expenses. Homeowners concerned about Medicaid recovery typically use an Irrevocable (Medicaid) Trust instead.

Can you change TOD deed beneficiaries later?

Yes. You can change beneficiaries at any time by filing a new TOD deed with your County Clerk’s Office. The most recently filed TOD deed overrides all prior versions.

What Is A Donor Advised Fund and How Do They Work for Charitable Contributions?

Due to changes in the tax laws, fewer individuals are now able to capture a tax deduction for their charitable contributions. In an effort to recapture the tax deduction, more individuals are setting up Donor Advised Funds at Fidelity and Vanguard to take full advantage of the tax deduction associated with giving to a charity, church, college, or other not-for-profit organizations.

Due to changes in the tax laws, fewer individuals are now able to capture a tax deduction for their charitable contributions. In an effort to recapture the tax deduction, more individuals are setting up Donor Advised Funds at Fidelity and Vanguard to take full advantage of the tax deduction associated with giving to charity, church, college, or other not-for-profit organizations.

In this article, we will review:

The reason why most taxpayers can no longer deduct charitable contributions

What is a Donor Advised Fund?

How do Donor Advised Funds operate?

Gifting appreciated securities to Donor Advised Funds

How are Donor Advised Funds invested?

How to set up a self-directed Donor Advised Fund

The Problem: No Tax Deductions For Charitable Contributions

When the Tax Cut and Jobs Act was passed in 2017, it greatly limited the number of taxpayers that were able to claim a tax deduction for their charitable contributions. Primarily because in order to claim a tax deduction for charitable contributions, you have to itemize when you file your taxes because charitable contributions are an itemized deduction.

When you file your taxes, you have to choose whether to elect the standard deduction or to itemize. The Tax Cut & Jobs Act greatly increased the amount of the standard deduction, while at the same time it capped two of the largest itemized tax deductions for taxpayers - which is state income tax paid and property taxes. SALT (state and local taxes) are now capped at $10,000 per year if you itemize.

In 2025, the standard deduction for single filers is $15,000 and $30,000 for married filing joint, which means if you are a married filer, and you want to deduct your charitable contributions, assuming you reach the SALT cap at $10,000 for state income and property taxes, you would need another $20,000 in tax deductions before your reached that amount of the standard deduction. That’s a big number to hurdle for most taxpayers.

Example: Joe and Sarah file a joint tax return. They pay state income tax of $8,000 and property taxes of $6,000. They donate $5,000 to their church and a variety of charities throughout the year. They can elect to take the standard deduction of $30,000, or they could itemize. However, if they itemize while their state income tax and property taxes total $14,000, they are capped at $10,000 and the only other tax deduction that they could itemize is their $5,000 to church and charity which brings them to a total of $15,000. Since the standard deduction is $14,000 higher than if they itemized, they would forgo being able to deduct those charitable contributions, and just elect that standard deduction.

How many taxpayers fall into the standard deduction category? According to the Tax Policy Center, in 2020, about 90% of taxpayers claimed the standard deduction. Prior to the passing of the Tax Cut and Jobs Act, only about 70% of taxpayers claimed the standard deduction meaning that more taxpayers were able to itemize and capture the tax deduction for their charitable contributions.

What Is A Donor Advised Fund

For individuals that typically take the standard deduction, but would like to regain the tax deduction for their charitable contributions, establishing a Donor Advised Fund may be a solution.

A Donor Advised Fund looks a lot like a self-directed investment account. You can make contributions to your donor advisor fund, you can request distributions to be made to your charities of choice, and you can direct the investments within your account. But the account is maintained and operated by a not-for-profit organization, a 501(c)(3), that serves as the “sponsoring organization”. Two of the most recognized providers within the Donor Advised Fund space are Fidelity and Vanguard.

Both Fidelity and Vanguard have their own Donor Advised Fund program. These large investment providers have established a not-for-profit arm for the sole purpose of allowing investors to establish, operate, and invest their Donor Advised Account for their charitable giving.

Why Do People Contribute To A Donor Advised Fund?

We just answered the “What” question, now we will address the “Why” question. Why do people contribute to these special investment accounts at Fidelity and Vanguard and what is it about these accounts that allow taxpayers to capture the tax deduction for their charitable giving that was previously lost?

The short answer - it allows taxpayers that give to charity each year, to make a large lump sum contribution to an investment account designated for their charitable giving. That then allows them to itemize when they file their taxes and capture the deduction for their charitable contributions in future years.

Here’s How It Works

As an example, Tim and Linda typically give $5,000 per year to their church and charities throughout the year. Since they don’t have any other meaningful tax deductions outside of their property taxes and state income taxes that are capped at $10,000, they take the $30,000 standard deduction when they file their taxes, and do not receive any additional tax deductions for their $5,000 in charitable contributions, because they did not itemize.

Instead, Tim and Linda establish a Donor Advised Fund at Fidelity, and fund it with a one-time $50,000 contribution. Since they made that contribution to a Donor Advised Fund which qualifies as an IRS approved charitable organization, the year that they made the $50,000 contribution, they will elect to itemize when they file their taxes and they’ll be able to capture the full $50,000 tax deduction, since that amount is well over the $30,000 standard deductions.

But the $50,000 that was contributed to their Donor Advised Fund does not have to be distributed to charities all in that year. Each Donor Advised Program has different minimum annual charitable distribution requirements, but at the Fidelity program it’s just $50 per year. In other words, taxpayers that make these contributions to the Donor Advised Fund can capture the full tax benefit in the year they make the contributions, but that account can then be used to fund charitable contribution for many years into the future, they just have to distribute at least $50 per year to charity.

It gets better, Tim and Linda then get to choose how they want to invest their Donor Advised Fund, and they select a 60% stock / 40% bond portfolio. So not only are they able to give from the $50,000 that they contributed, but all of the investment returns continue to accumulate in that account that Tim and Linda will never pay tax on, that they can then use for additional charitable giving in the future.

How Do Donor Advised Funds Operate?

The example that I just walked you through laid the groundwork for how these Donor Advised Fund to operate, but I want to dive a little bit deeper into some features that are important with these types of accounts.

Funding Minimums

All Donor Advised Funds operate differently depending on the provider. One example is the minimum funding requirement to open a Donor Advised Fund. The Fidelity program does not have an investment minimum, so they can be opened with any amount. However, the Vanguard program currently has a $20,000 investment minimum.

Fees Charged By Donor Advised Sponsor

Both Vanguard and Fidelity assess an annual “administration fee” against the assets held within their Donor Advised Fund program. This is how the platform is compensated for maintaining the not-for-profit entity, processing contributions and distributions, investment services, issuing statements, trade confirmations, and other administrative responsibilities. At the time that I’m writing this article, both the Fidelity and Vanguard program charge an administrative fee of approximately 0.60% per year.

How Charitable Distributions Are Made From Donor Advised Funds

Once the Donor Advised Account is funded, owners are able to either login online to their account and request money to be sent directly to their charity of choice, or they can call the sponsor of the program and provide payment instructions over the phone.

For example, if you wanted to send $1,000 to the Red Cross, you would log in to your Donor Advised account and request that $1,000 be sent directly from your Donor Advised account to the charity. You never come into contact with the funds. The charitable distributions are made directly from your account to the charity.

When you login to their online portals, they have a long list of pre-approved not-for-profit organizations that have been already established on their platform, but you are able to give to charities that are not on that pre-approved list. A common example is a church or a local not-for-profit organization. You can still direct charitable contributions to those organizations, but you would need to provide the platform with the information that they need to issue the payment to the not-for-profit organization not on their pre-approved list.

Annual Grant Requirement

As I mentioned earlier, different donor advised programs have different requirements as to how much you are required to disperse from your account each year and some platforms only require a disbursement every couple of years. For example, the Vanguard program only requires that a $500 charitable distribution be made once every three years, but they do not require an annual distribution to be made.

Irrevocable Contributions

It’s important to understand that contributions made to Donor Advised Funds are irrevocable, meaning they cannot be reversed. Once the money is in your Donor Advised Account, you cannot ask for that money back. The platform just gives you “control” over the investment allocation, and how and to who the funds are disbursed to for your charitable giving.

What Happens To The Balance In The Donor Advised Fund After The Owner Passes Away?

Since some of our clients have substantial balances in these Donor Advised Funds, we had to ask the question, “What happens to the remaining balance in the account after the owner of the account passes away?”. Again, the answer can vary from platform to platform, but most platforms offer a few options.

Option 1: The owner of the account can designate any number of charities as final beneficiaries of the account balance after they pass away, and then the full account balance is distributed to those charities after they pass.

Option 2: The owner can name one or more successor owners for the account that will take over control of the account and the charitable giving after the original owner passes away. As planners, we then asked the additional question, “What if they have multiple children, and each child has different charitable preferences?”. The response from Vanguard was that the Donor Advisor Fund can be split into separate Donor Advised accounts controlled by each child, Then, each child can dictate how the funds in their account are distributed to charity.

Gifting Cash or Appreciated Securities

There are two main funding options when making contributions to a Donor Advised Fund. You can make a cash contribution or you can fund it by transferring securities from a brokerage account. Funding with cash is easy and straightforward. When you establish your Donor Advised Fund, you can set up bank instructions to attach your checking account to their Donor Advised Fund for purposes of making contributions to the account. There are limits on the tax deductions for cash contributions in a given year. For cash contributions, donors can receive a tax deduction up to 60% of their AGI for the year.

Funding the donor advised fund with appreciated securities from your taxable brokerage account has additional tax benefits. First, you receive the tax deduction for making the charitable contribution just like it was made in cash, but, if you transfer a stock or security directly from your taxable brokerage account to the Donor Advised Fund, the owner of the brokerage account avoids having to pay tax on the unrealized capital gains built up in that security.

For example, Sue bought $10,000 of Apple stock 10 years ago and it’s now worth $50,000. If she sells the stock, she will have to pay long term capital gains taxes on the $40,000 gain in that holding. If instead, she sets up a Donor Advised Fund and transfers the $50,000 in Apple stock directly from her brokerage account to her Donor Advised account at Fidelity, she may receive a tax deduction for the full $50,000 fair market value of the stock and avoids having to pay tax on the unrealized capital gain.

An important note regarding the deduction limits for gifting appreciated securities - the tax deduction is limited to 30% of the taxpayers AGI for the year. Example, if Sue has an AGI of $100,000 for 2025 and wants to fund her Donor Advised Fund with her appreciated stock, the most she can take a deduction for in 2025 is $30,000. ($100,000 AGI x 30% limit).

As you can see, transferring appreciated stock to a Donor Advised Fund can be beneficial, but cash offers a higher threshold for the tax deduction in a single year.

Donor Advised Funds Do Not Make Sense For Everyone

While establishing and funding a Donor Advised Fund may be a viable solution for many taxpayers, it’s definitely not for everyone. In short, your annual charitable contributions have to be large enough for this strategy to make sense.

First example, if you are contributing approximately $2,000 per year to charity, and you don’t intend on making bigger contributions to charities in the future, it may not make sense to contribute $40,000 to a Donor Advised Fund. Remember, the whole idea is you have to make a large enough one-time contribution to hurdle the standard deduction limit for itemizing to make sense. You also have to itemize to capture the tax deduction for your charitable contributions.

If you are a single filer, you don’t have any tax deductions, and you make a $5,000 contribution to a Donor Advised Fund - that is still below the $15,000 standard deduction amount. In this case, you are not realizing the tax benefit of making that contribution to the Donor Advised Fund. If instead, you made a $30,000 contribution as a single filer, now it may make sense.

Second example, not enough taxable income. For our clients that are retired, many of them are showing very little income (on purpose). If we have a client that is only showing $50,000 for their AGI, the tax deduction for their cash contributions would be limited to $30,000 (60% of AGI) and gift appreciated securities would be limited to $15,000 (30% of AGI). Unless they have other itemized deductions, that may not warrant making a contribution to a Donor Advised Fund because they are right there at the Standard Deduction amount. PLUS, they are already in a really low tax bracket, so they don’t really need the deduction.

This Strategy is Frequently Used When A Client Sells Their Business

Our clients commonly use this Donor Advised Fund strategy during abnormally large income years. The most common is when a client sells their business. They may realize a few million dollars in income from the sale of their business in a single year, and if they have some form of charitable intent either now or in the future, they may be able to fund a Donor Advised Fund with $100,000+ in cash or appreciated securities. This takes income off the table at potentially the highest tax brackets and they now have an account that is invested and growing that will fund their charitable gifts for the rest of their life.

How to Set-up A Donor Advised Fund

Setting up a Donor Advised Fund is very easy. Here are the links to the Fidelity and Vanguard Platforms for their Donor Advised Fund solutions:

Fidelity Donor Advised Fund Link: Fidelity Charitable Fund Link

Vanguard Donor Advised Fund Link: Vanguard Charitable Fund Link

Disclosure: We want to provide the links as a convenience to our readers, but it does not represent an endorsement of either platform. Investors should seek guidance from their financial professionals.

These Donor Advised Funds for the most part are self-directed platforms which allow you to select the appropriate investment allocation from their investment menu when you set up your account.

Contact Us With Questions if you have any questions on the Donor Advised Fund tax strategy, please feel free to reach out to us.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Why can fewer taxpayers deduct charitable contributions now?

After the 2017 Tax Cuts and Jobs Act (TCJA), the standard deduction nearly doubled and capped state and local tax (SALT) deductions at $10,000. Because of this, most taxpayers now take the standard deduction instead of itemizing, which means they can’t deduct charitable donations.

What is a Donor Advised Fund (DAF)?

A Donor Advised Fund is a charitable investment account that allows you to make a large, tax-deductible contribution in one year, invest the funds for potential growth, and distribute money to charities over time. Providers like Fidelity and Vanguard operate these programs through nonprofit foundations.

How does a Donor Advised Fund help restore the tax deduction for charitable giving?

By making a single large contribution to a DAF, donors can exceed the standard deduction threshold and itemize on their tax return in that year. The donor then uses the fund to make charitable gifts gradually over future years, even though they already received the full tax deduction upfront.

Can you fund a Donor Advised Fund with appreciated stock?

Yes. You can contribute appreciated securities instead of cash. This approach allows you to receive a tax deduction for the full fair market value of the stock while also avoiding capital gains taxes on the appreciation.

What are the tax deduction limits for contributions?

Cash contributions to a DAF are deductible up to 60% of your adjusted gross income (AGI), while appreciated securities are deductible up to 30% of AGI. Any excess contributions can be carried forward for up to five years.

When does a Donor Advised Fund make sense?

DAFs make the most sense for individuals with large charitable intent who want to bunch multiple years of giving into one tax year—often after a major income event like selling a business or receiving a large bonus.

What Vehicle Expenses Can Self-Employed Individuals Deduct?

Self-employed individuals have a lot of options when it comes to deducting expenses for their vehicle to offset income from the business. In this video we are going to review:

1) What vehicle expenses can be deducted: Mileage, insurance, payments, registration, etc.

2) Business Use Percentage

3) Buying vs Leasing a Car Deduction Options

4) Mileage Deduction Calculation

5) How Depreciation and Bonus Depreciation Works

6) Depreciation recapture tax trap

7) Can you buy a Ferreri through the business and deduct it? (luxury cars)

8) Tax impact if you get into an accident and total the vehicle

Self-employed individuals have a lot of options when it comes to deducting expenses for their vehicle to offset income from the business. In this video we are going to review:

What vehicle expenses can be deducted: Mileage, insurance, payments, registration, etc.

Business Use Percentage

Buying vs Leasing a Car Deduction Options

Mileage Deduction Calculation

How Depreciation and Bonus Depreciation Works

Depreciation recapture tax trap

Can you buy a Ferreri through the business and deduct it? (luxury cars)

Tax impact if you get into an accident and total the vehicle

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What vehicle expenses can self-employed individuals deduct?

Self-employed individuals can generally deduct expenses related to the business use of their vehicle, including gas, insurance, registration, maintenance, repairs, lease payments, and loan interest. You can use either the standard mileage method or the actual expense method—but not both for the same vehicle in a given year.

How do you calculate the business-use percentage?

If your car is used for both personal and business purposes, only the business portion is deductible. To determine your business-use percentage, divide your business miles by your total annual miles. For example, if you drove 20,000 miles during the year and 12,000 were for business, you can deduct 60% of eligible expenses.

Is it better to buy or lease a car for business?

Both options can be tax-efficient. Lease payments are deductible based on the business-use percentage, but leased cars don’t qualify for depreciation. Purchased vehicles allow you to claim depreciation (including bonus depreciation and Section 179 deductions), but you can’t deduct the full purchase price in one year unless it qualifies for special rules.

How does the mileage deduction work?

For 2025, the IRS standard mileage rate is set annually (e.g., 67 cents per mile in 2024). Simply multiply your total business miles by that rate. This rate includes depreciation, gas, maintenance, and insurance, so you can’t deduct those costs separately if you use this method.

How does vehicle depreciation work—and what’s bonus depreciation?

If you purchase a vehicle, you can depreciate the business-use portion of its cost over several years. Heavy vehicles (over 6,000 pounds) may qualify for accelerated write-offs, including 80% bonus depreciation in 2025 or full expensing under Section 179 up to certain limits. However, “luxury” cars like Ferraris or Lamborghinis are subject to strict IRS caps that limit the deduction.

What happens if the vehicle is sold or totaled?

If you sell or total a business vehicle that has been depreciated, you may owe “depreciation recapture” tax on the portion of depreciation claimed. Essentially, you pay ordinary income tax on the amount of depreciation you previously deducted, up to your gain on the sale or insurance payout.

Social Security Will Only Increase by 2.5% In 2025

The Social Security Administration recently announced that the cost-of-living adjustment (COLA) for 2025 will only be 2.5% for 2025. That is a much lower COLA increase than we have seen in the past few years, with a COLA increase of 3.2% in 2024 and an increase of 8.7% in 2023. According to the Social Security Administration, the 2.5% increase in 2025 will result, on average, in a $50 per month increase to social security recipients.

The Social Security Administration recently announced that the cost-of-living adjustment (COLA) for 2025 will only be a 2.5% increase. This is significantly lower than the COLA increases in the past few years, which included a 3.2% increase in 2024 and a notable 8.7% increase in 2023. According to the Social Security Administration, the 2.5% increase in 2025 will result in an average $50 per month increase for Social Security recipients.

Immediately after the announcement, many retirees expressed concerns that a modest 2.5% increase is not sufficient to keep pace with the rising costs they face for groceries, insurance, rent, and other everyday expenses.

Medicare Premiums May Increase by More Than 2.5%

While the Medicare Part B and Part D premium amounts for 2025 have yet to be released, consensus expects increases greater than 3% for both Part B and Part D. If this holds true, retirees may gain an average of $50 per month from the COLA increase in their Social Security benefits, but a substantial portion of that could be offset by higher Medicare premiums, which are deducted directly from their monthly Social Security payments.

In 2024, the COLA increase for Social Security was 3.2%, but Medicare Part B premiums rose by 5.9%, leaving many retirees already behind in keeping up with inflation. We could potentially see a similar situation in 2025.

COLA Calculation Controversy

In recent years, there has been growing controversy over how the Social Security Administration calculates the annual cost-of-living adjustment for benefits. While the COLA is based on the Consumer Price Index (CPI), which tracks the prices of various goods and services within the U.S. economy, questions have arisen about whether the specific goods and services included in the CPI basket are still a good reflection of overall price increases across the economy.

Many consumers would agree that it feels like prices increased by more than 3.2% in 2024. If the Federal Reserve successfully delivers a soft landing, avoids a recession, and the economy starts growing at a faster pace, what are the chances that prices will rise by more than 2.5% in 2025? I'd say the chances are high.

Retirees Are in a Tough Spot

Many retirees live on fixed incomes, and Social Security benefits often represent a large portion of their total yearly income. If the COLA increases for Social Security do not adequately keep pace with rising costs, retirees may be forced to either reduce their spending or consider re-entering the workforce on a part-time basis to generate more income to meet their expenses.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the Social Security COLA increase for 2025?

The Social Security Administration announced a 2.5% cost-of-living adjustment (COLA) for 2025. This means the average Social Security recipient will see about a $50 per month increase starting in January 2025.

How does the 2025 COLA compare to recent years?

The 2025 COLA is much smaller than recent increases—3.2% in 2024 and 8.7% in 2023. Those higher adjustments reflected elevated inflation during and after the pandemic, while the latest 2.5% figure reflects slower inflation in 2024.

Will higher Medicare premiums offset the COLA increase?

Possibly. Medicare Part B and Part D premiums for 2025 are expected to rise by more than 3%, which could absorb much of the $50 monthly COLA increase. Since Medicare premiums are deducted directly from Social Security checks, retirees may see little or no net increase in their take-home benefits.

How is the Social Security COLA calculated?

The COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which measures average price changes for goods and services. Critics argue that this index doesn’t accurately reflect the higher inflation retirees face in healthcare, housing, and food costs.

Why are retirees concerned about the 2025 COLA?

Many retirees are worried that a 2.5% increase won’t keep up with rising living expenses, especially as insurance, rent, and grocery prices remain elevated. For those on fixed incomes, even small shortfalls between benefit increases and inflation can erode purchasing power.

What can retirees do if their benefits aren’t keeping up with inflation?

Some retirees may need to adjust their spending, draw more from savings, or consider part-time work to supplement their income. Financial planners often recommend reviewing budgets annually to account for inflation and exploring strategies to reduce taxable income to preserve more of their benefits.

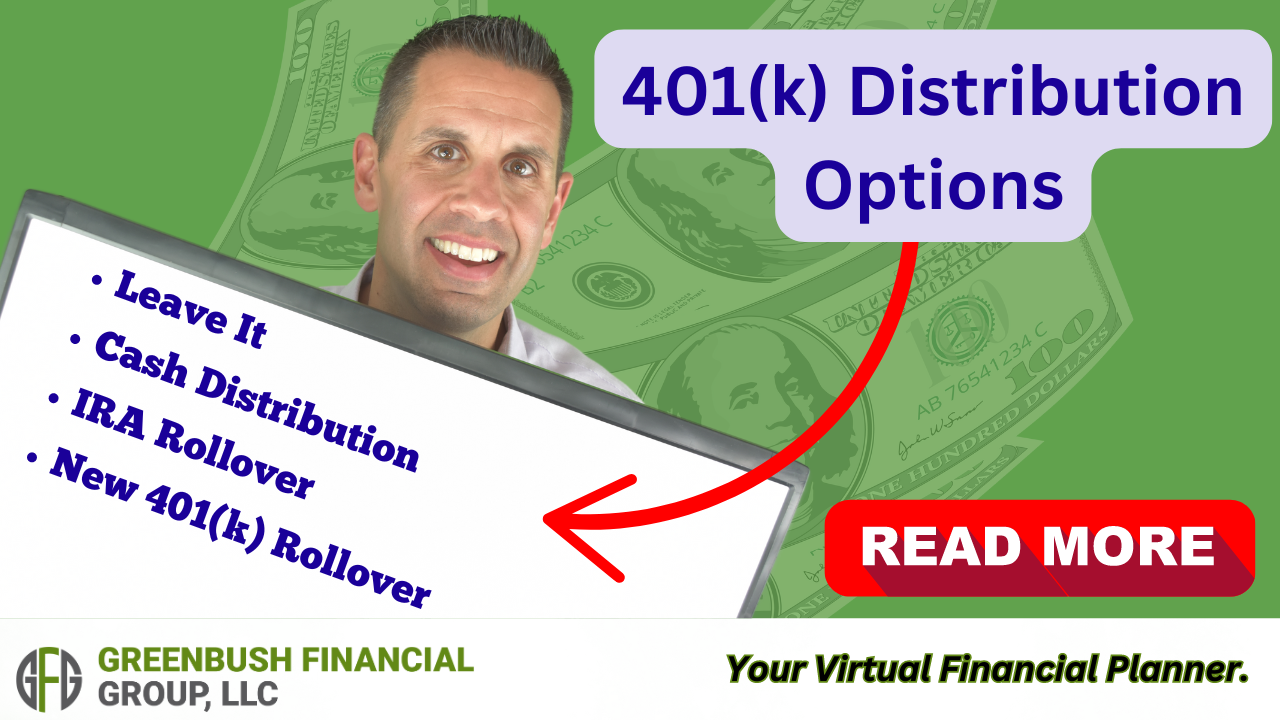

Leaving Your Job? What Should You Do With Your 401(k)?

When you separate service from an employer, you have to make decisions with regard to your 401K plan. It’s important to understand the pros and cons of each option while also understanding that the optimal solution often varies from person to person based on their financial situation and objectives. The four primary options are:

1) Leave it in the existing 401(k) plan

2) Rollover to an IRA

3) Rollover to your new employer’s 401(k) plan

4) Cash Distribution

When you separate from an employer, there are important decisions to make regarding your 401(k) plan. It’s crucial to understand the pros and cons of each option, as the optimal solution often varies depending on individual financial situations and objectives. The four primary options are:

Leave it in the existing 401(k) plan

Rollover to an IRA

Rollover to your new employer’s 401(k) plan

Cash Distribution

Option 1:Leave It In The Existing 401(k) Plan

If your 401(k) balance exceeds $7,000, your employer is legally prohibited from forcing you to take a distribution or roll over the funds. You can keep your balance invested in the plan. While no new contributions are allowed since you’re no longer employed, you can still change your investment options, receive statements, and maintain online access to the account.

PROS to Leaving Your Money In The Existing 401(k) Plan

#1: No Urgent Deadline to Move

Leaving a job often coincides with major life changes—whether retiring, job hunting, or starting a new position. It’s reassuring to know that you don't need to make an immediate decision regarding your 401(k), allowing time to evaluate options and choose the best one.

#2: You May Not Be Eligible Yet For Your New Employer’s 401(k) Plan

One of the distribution options that we will address later in this article is rolling over your balance from your former employer's 401(k) plan into your new employer’s 401(k) plan. However, it's not uncommon for companies to have a waiting period for new employees before they're eligible to participate and the new company’s 401(k) plan. If you must wait a year before you have the option to roll over your balance into your new employer's plan, the prudent solution may be just to leave the balance in your former employer’s 401(k) plan, and just roll it over once you become eligible for the new 401(k) plan.

#3: Fees May Be Lower

It's also prudent to do a fee assessment before you move your balance out of your former employer’s 401(k) plan. If you work for a large employer, it's not uncommon for there to be significant assets within that company’s 401(k) plan, which can result in lower overall fees to any plan participants that maintain a balance within that plan. For example, if you work for Company ABC, which is a big publicly traded company, they may have $500 million in their 401(k) plan when you total up all the employee's balances. That may result in total annual fees of under 0.50% depending on the platform. If your balance in the plan is $100,000, and you roll over your balance to either an IRA or a smaller employer’s 401(k) plan, the total fees could be higher because you are no longer part of a $500 million pool of assets. You may end up paying 1% or more in fees each year, depending on where you roll over your balance.

#4: Age 55 Rule

401(k) plans have a special distribution option that if you separate from service with the employer after reaching age 55, you are allowed to request cash distributions directly from that 401(k) plan, but you avoid the 10% early withdrawal penalty that normally exists in IRA accounts for taking distributions under the age of 59 ½. For individuals that retire after age 55, not before age 59 ½, this is one of the primary reasons why we advise some clients to maintain their balance in the former employer’s 401(k) plan and take distributions from that account to avoid the 10% penalty. If they were to inadvertently roll over the entire balance to an IRA, that 10% early withdrawal penalty exception would be lost.

CONS to Leaving Your Money In The Existing 401(k) Plan

#1: Scattered 401(k) Balance

I have met with individuals who have three 401(k) plans, all with former employers. When I start asking questions about the balance in each account, how each 401(k) account is invested, and who the providers are, most individuals with more than one 401(k) account have trouble answering those questions. From both a planning and investment strategy standpoint, it's often more efficient to have all your retirement dollars in one place so you can very easily assess your total retirement nest egg, how that nest egg is invested, and you can easily make investment changes or updates to your personal information.

#2: Forgetting to Update Addresses

It's not uncommon for individuals to move after they've left employment with a company, and over the course of the next 10 years, it's not uncommon for someone to move multiple times. Oftentimes, plan participants forget to go back to all their scattered 401K plans and update their mailing addresses, so they are no longer receiving statements on many of those accounts which makes it very difficult to keep track of what they have and what it's invested in.

#3: Limited Investment Options

401(k) plans typically limit plan participants to a set menu of investments which the plan participant has no control over. Rolling your balance into a new employer’s plan or an IRA could provide a broader range of investment options.

OPTION 2: Rollover to an IRA

The second option for plan participants is to roll over their 401(k) balance to an IRA(s). The primary advantage of the IRA rollover is that it allows employees to remove their balance from their former employers' 401(k) plan, but it does not generate tax liability. The pre-tax dollars within the 401(k) plan can be rolled directly to a Traditional IRA, and any Roth dollars in the 401(k) plan can be rolled over into a Roth IRA.

PROS of 401K Rollover to IRAs

#1: Full Control of Investment Options

As I just mentioned in the previous section, 401(k)’s typically have a set menu of investments available to plan participants by rolling over their balance to an IRA. The plan participant can choose to invest their IRA balance in whatever they would like - individual stocks, bonds, mutual funds, CD, etc.

#2: Consolidating Retirement Accounts

Since it's not uncommon for employees to have multiple employers over their career, as they leave employment with each company, if the employee has an IRA in their own name, they can keep rolling over the balances into that central IRA account to consolidate all their retirement accounts into a single account.

#3: Ease of Distributions in Retirement

It is sometimes easier to take distributions from an IRA than it is from a 401(k) plan. When you request a distribution from a 401(k) plan, you typically have to work through the plan’s administrator. The plan trustee may need to approve each distribution, and some plans are “lump-sum only,” which means you can’t take partial distributions from the 401(k) account. With those lump-sum-only plans, when you request your first distribution from the account, you have to remove your entire balance. When you roll over the balance to an IRA, you can often set up monthly reoccurring distributions, or you can request one-time distributions at your discretion.

#4: Avoid the 401(k) 20% Mandatory Fed Tax Withholding

When you request Distributions from a 401(k) plan, by law, they are required to withhold 20% for Federal Taxes from each distribution (unless it’s an RMD or hardship). But what if you don’t want them to withhold 20% for Fed taxes? With 401(k) plans, you don’t have a choice. By rolling over your balance to an IRA, you have the option to not withhold any taxes or electing a Fed amount less than 20% - it’s completely up to you.

#5: Discretionary Management

Most 401(k) investment platforms are set up as participant-directed platforms which means the plan participant has to make investment decisions with regard to their accounts without an investment advisor overseeing the account and trading it actively on their behalf. Some individuals like the idea of having an investment professional involved to actively manage their retirement accounts on their behalf, and rolling over the balance from 401(k) to an IRA can open up that option after the employee has separated from service.

CONS of 401(k) Rollover to IRAs

Here is a consolidated list based on some of the pros and cons already mentioned:

Fees could be higher in an IRA compared to the existing 401(k)

The Age 55 10% early withdrawal exception could be lost

No point in rolling to an IRA if the plan is just to roll over to the new employer’s plan once you have met the plan’s eligibility requirements

OPTION 3: Rollover to New Employer’s 401(k) Plan

To avoid repeating many of the pros and cons already mentioned here is a quick hit list of the pros and cons

PROS:

Keep retirement accounts consolidated in new employer plan

No tax liability incurred for rollover

Potentially lower fees compared to rolling over to an IRA

If the new plan allows 401(k) loans, rollover balances are typically eligible toward the max loan amount

Full balance eligible for age 55 10% early withdrawal penalty exception

A new advantage that I would add to this list is for employees over the age of 73 who are still working; if you keep your pre-tax retirement account balance within your current employer’s 401(k) plan, you can avoid the annual RMD requirement. When you turn certain ages, currently 73 but soon to be 75, the IRS forces you to start taking taxable distributions out of your pre-tax retirement accounts. However, there is an exception to that rule for any pretax balances maintained in a 401(k) plan with your current employer. The balance in your 401(k) plan with your CURRENT employer is not subject to annual RMDs so you avoid the tax hit associated with taking distributions from a pre-tax retirement account.

I put CURRENT in all caps because this 401(k) RMD exception does not apply to balances in former employer 401(k) plans. You must be employed by that company for the entire year to avoid the RMD requirement. Balances in former employer 401(k) plans are still subject to the RMD requirement.

CONS:

Potentially limited to investment options offered via the 401(k) investment menu

You may not be allowed to take distribution at any time from your 401(k) account after the rollover, whereas a rollover IRA would allow you to keep that option open.

Your personal investment advisor cannot manage those assets within the 401(k) plan

Possible distribution and tax withholding restrictions depend on the plan design

OPTION 4: Cash Distributions

I purposely saved cash distributions for last because it is rarely the optimal distribution option. When you request a cash distribution from a 401(k) plan and you are under the age of 59 ½, you will incur fed taxes, potentially state taxes depending on what state you reside in, and a 10% early withdrawal penalty. When you begin to total up the taxes and penalties, sometimes you’re losing 30% - 50% of your balance in the plan to taxes and penalties.

When you lose 30 to 50% of your retirement account balance in one shot, it can set you back years in the future when it comes to trying to figure out what date you can retire. While, it's not uncommon for a 25-year-old to not be overly concerned with their retirement date; making the decision to withdraw their entire account balance can end up being a huge regret when they are 75 and still working while all their friends retired 10 years before them.

However, as financial planners, we do acknowledge that someone losing their job can create financial disruption, and sometimes a balance needs to be reached between a cash distribution to help them bridge the financial gap to their next career while maintaining as much of their retirement account as possible. The good news is it's not an all-or-nothing decision. For clients that have a high degree of uncertainty, it can sometimes be prudent to roll over the balance from the 401(k) to an IRA which gives them maximum flexibility as to how much they can take from that IRA account for distributions, but usually reserves the right to allow them to roll over that IRA balance into a future employer’s 401(k) plan at their discretion.

Example: Samantha Was just laid off by Company XYZ; she has a $50,000 balance in their 401(k) plan and she is worried that she's not going to be able to pay her bills for the next few months while she's looking for her next job. She may want to roll over that $50,000 balance to an IRA so she can distribute $10,000 from the IRA, pay the taxes and the penalties, but continue to maintain the remaining $40,000 in the IRA untaxed. But if she struggles to continue to find her next career, she can always go back to the IRA and take additional distributions. Samantha then gets hired by Company ABC and is eligible to participate in that company's 401(k) plan after three months. At that time, she can make the decision to either roll over the IRA balance to her new 401(k) plan or just keep the IRA where it is.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are my options for my 401(k) after leaving an employer?

You have four main options:

Leave the balance in your existing 401(k) plan

Roll it over to an IRA

Roll it into your new employer’s 401(k) plan

Take a cash distribution

Each option has pros and cons depending on your age, employment status, investment goals, and tax situation.

When does it make sense to leave my 401(k) with my former employer?

If your balance is over $7,000, you can keep it in the plan. This may make sense if:

The plan offers low fees or strong investment options

You’re not yet eligible for your new employer’s plan

You separated from service at age 55 or later and may want penalty-free withdrawals under the “Age 55 Rule”

What are the benefits of rolling my 401(k) to an IRA?

Rolling to an IRA offers full investment control, potential for professional management, and simplified account consolidation. It also avoids mandatory 20% federal tax withholding on withdrawals. However, you lose the age 55 penalty exception and may pay slightly higher fees depending on your IRA provider.

Why might I roll my old 401(k) into my new employer’s plan?

This option keeps your retirement accounts consolidated and allows you to continue deferring taxes. It can also be advantageous if you’re over age 73 and still working, since RMDs (required minimum distributions) don’t apply to your current employer’s 401(k). However, investment options may be limited, and you may lose access to flexible withdrawals.

What happens if I take a cash distribution from my 401(k)?

A cash-out triggers ordinary income taxes and, if you’re under 59½, a 10% early withdrawal penalty. Between taxes and penalties, you could lose 30–50% of your balance. In most cases, this option should be avoided unless absolutely necessary.

Focusing On Buying Dividend Paying Stocks Is A Mistake

Picking the right stocks to invest in is not an easy process but all too often I see retail investors make the mistake of narrowing their investment research to just stocks that pay dividends. This is a common mistake that investors make and, in this article, we are going to cover the total return approach versus the dividend payor approach to investing.

Picking the right stocks to invest in is not an easy process, but all too often I see retail investors make the mistake of narrowing their investment research to just stocks that pay dividends. This is a common mistake that investors make, and in this article, we are going to cover the total return approach versus the dividend payor approach to investing.

Myth: Stocks That Pay Dividends Are Safer

Retail investors sometimes view dividend paying stocks as a “safer” investment because if the price of the stock does not appreciate, at least they receive the dividend. There are several flaws to this strategy. First, when times get tough in the economy, dividends can be cut, and they are often cut by companies to preserve cash. For example, prior to the 2008/2009 Great Recession, General Electric stock was paying a solid dividend, and some retirees were using those dividends to supplement their income. When the recession hit, GE dramatically cut it dividends, forcing some shareholders to sell the stock at lower levels just to create enough cash to supplement their income. Forcing a buy high, sell low scenario.

The Magnificent 7 Stocks Do Not Pay Dividends

In more recent years, when you look at the performance of the “Magnificent 7” tech stocks which have crushed the performance of the S&P 500 Index over the past 1 year, 5 years, and 10 years, there is one thing most of those Magnificent 7 stocks have in common. As I write this article today, Nvidia, Microsoft, Google, Amazon, and Meta either don’t pay a dividend or their dividend yield is under 1%. So, if you were an investor that had a bias toward dividend paying stocks, you may have missed out on the “Mag 7 rally” that has happened over the past 10 years.

Growth Companies = No Dividends

When a company issues a dividend, they are returning capital to the shareholders as opposed to reinvesting that capital into the company. Depending on the company and the economic environment, a company paying a dividend could be viewed as a negative action because maybe the company does not have a solid growth plan, so instead of reinvesting the money into the company, they default to just returning that excess capital to their investors. It’s may feel good to have some investment income coming back to you, but if you are trying to maximize investment returns over the long term, will that dividend paying stock be able to outperform a growth company that is plowing all of their cash back into more growth?

Companies Taking Loans to Pay Their Dividend

For companies that pay a solid dividend, they are probably very aware that there are subsets of shareholders that are holding their stock for the dividend payments, and if they were to significantly cut their dividend or stop it all together, it may cause investors to sell their stock. When these companies are faced with tough financial conditions, they may resist cutting the dividends long after they really should have, putting the company in a potentially worse financial position knowing that shareholders may sell their stock as soon as the dividend cut is announced.

Some companies may even go to the extreme that since they don’t have the cash on hand to pay the dividend, they will issue bonds (go into debt) to raise enough cash for the sole purpose of being able to continue to pay their dividends, which goes completely against the reason why most companies issue dividends.

If a company generates a profit, they can decide to reinvest that profit back into the company, return that capital to investors by paying a dividend, or some combination of two. However, if a company goes into debt just to avoid having to cut the dividend payments to investors, I would be very worried about the growth prospects for that company.

Focus on Total Return

I’m a huge fan on focusing on total return. The total return of a stock equals both how much the value of the stock has appreciated AND any dividends that the stock pays while the investor holds the stock. If I gave someone the option of owning Stock ABC that does not pay a dividend and Stock XYZ that pays a 5% dividend, a lot of individuals will automatically start to build a strong bias toward buying XYZ over ABC without digging much deeper into the analysis. However, if Stock ABC does not pay a dividend due to its significant growth prospects and rises 30% in a year, while Stock XYZ pays a 5% dividend but only appreciates 8%, the total return for Stock XYZ is just 13%. This means the investor missed out on an additional 17% return by choosing the lower-performing stock.

Diversification Is Still Prudent

The purpose of this article is not to encourage investors to completely abandon dividend paying stocks for growth stocks that don’t pay dividends. Having a diversified portfolio is still a prudent approach, especially since growth stocks tend to be more volatile over time. Instead, the purpose of this article is to help investors understand that just because a stock pays a dividend does not mean it’s a “safer investment” or that it’s a “better” long-term investment from a total return standpoint.

Accumulation Phase vs Distribution Phase

We categorize investors into two phases: the Accumulation Phase and the Distribution Phase. The Accumulation Phase involves building your nest egg, during which you either make contributions to your investment accounts or refrain from taking distributions. In contrast, the Distribution Phase refers to individuals who are drawing down from their investment accounts to supplement their income.

During the Accumulation Phase, a total return approach can be prudent, as most investors have a longer time horizon and can better weather market volatility without needing to sell investments to supplement their income. These investors are typically less concerned about whether their returns come primarily from appreciation or dividends.

As you enter the Distribution Phase, often in retirement, the strategy shifts. Reducing portfolio volatility becomes crucial because you are making regular withdrawals. For instance, if you need to withdraw $50,000 annually from your Traditional IRA and the market drops, you may be forced to liquidate investments at an inopportune time, negatively impacting long-term performance. In the Accumulation Phase, you can ride out market declines since you are not making withdrawals.

Times Are Changing

Traditionally, investors would buy and hold 10 to 30 individual dividend-paying stocks indefinitely. This is why inherited stock accounts often include companies like GE, AT&T, and Procter & Gamble, known for their consistent dividends.

However, the S&P 500 now features seven tech companies that make up over 30% of the index's total market cap, driving a significant portion of stock market returns over the past decade, with very few paying meaningful dividends. This article highlights the need for investors to adapt their stock selection methodologies as the economy evolves. It’s essential to understand the criteria used when selecting investments to maximize long-term returns.

Special Disclosure: This article does not constitute a recommendation to buy or sell any of the securities mentioned and is for educational purposes only.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Are dividend-paying stocks safer investments?

Not necessarily. Many investors view dividend-paying stocks as “safer,” but dividends can be reduced or eliminated when companies face financial challenges. For example, during the 2008–2009 recession, General Electric slashed its dividend, forcing some investors to sell shares at depressed prices. A company’s dividend does not guarantee stability or protection against losses.

Why do some high-performing stocks not pay dividends?

Many of the best-performing companies in recent years—such as Nvidia, Google, Amazon, and Meta—pay little to no dividends because they reinvest profits into growth opportunities. This reinvestment strategy has historically produced higher total returns than dividend payouts.

What is the difference between dividend income and total return?

Dividend income only reflects the cash paid to shareholders, while total return measures both price appreciation and dividend income combined. For example, a non-dividend stock that rises 30% may outperform a 5%-dividend stock that only appreciates 8%, producing a higher overall total return.

Can companies borrow money just to keep paying dividends?

Yes, and that’s often a red flag. Some firms issue debt to sustain dividend payments when cash flow is tight, which can signal financial strain. A healthy dividend policy should come from profits, not borrowing.

Should investors focus only on dividend-paying stocks?

No. Focusing solely on dividend payers can cause investors to miss out on major growth opportunities. A balanced portfolio—combining both dividend-paying and growth-oriented stocks—can help manage volatility while capturing more total return potential.

When does a dividend-focused strategy make sense?

Dividend-focused investing can make sense during the distribution phase (retirement), when investors rely on portfolio income and prefer lower volatility. During the accumulation phase (while saving for retirement), focusing on total return and reinvestment often leads to greater long-term wealth.

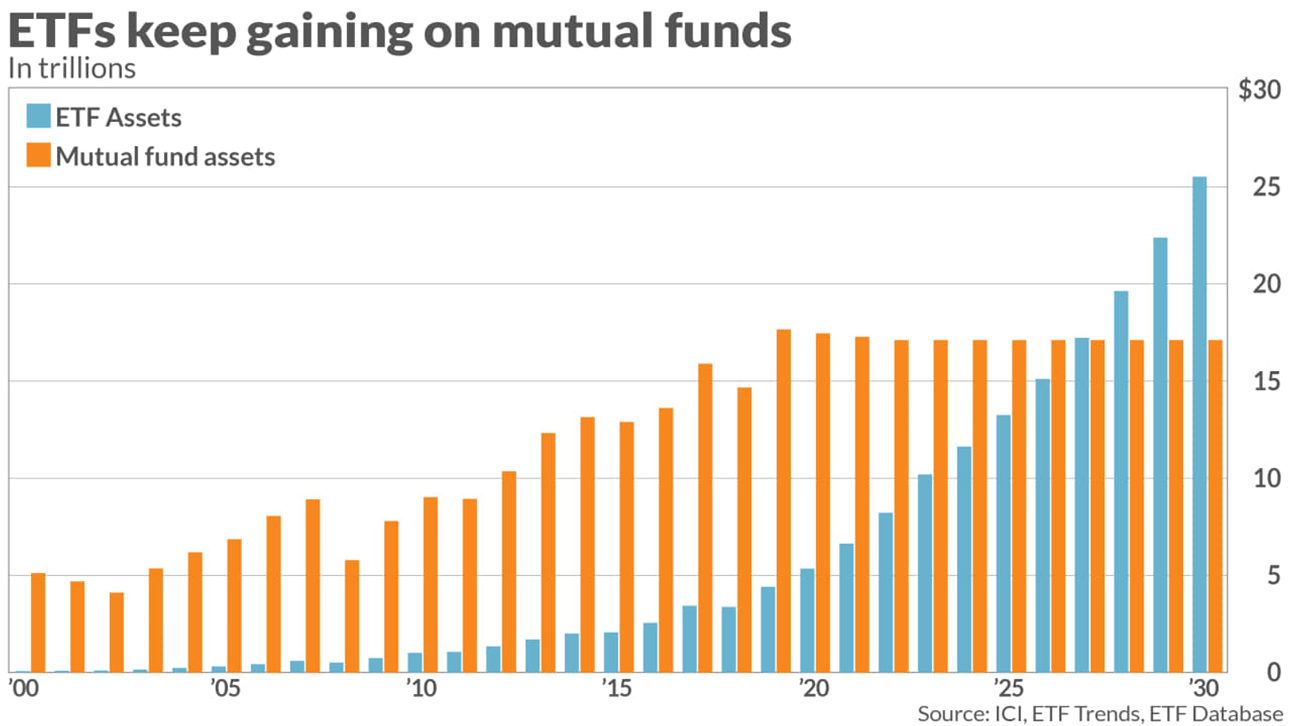

What Is an ETF & Why Have They Surpassed Mutual Funds in Popularity?

There is a sea change happening in the investment industry where the inflows into ETF’s are rapidly outpacing the inflows into mutual funds. When comparing ETFs to mutual funds, ETFs sometimes offer more tax efficiency, trade flexibility, a wider array of investment strategies, and in certain cases lower trading costs and expense ratios which has led to their rise in popularity among investors. But there are also some risks associated with ETFs that not all investors are aware of……..

There is a sea change happening in the investment industry where the inflows into ETF’s are rapidly outpacing the inflows into mutual funds. See the chart below, showing the total asset investments in ETFs vs Mutual Funds going back to 2000, as well as the Investment Company Institute’s projected trends going out to 2030.

Why is this happening? While mutual funds and ETFs may look similar on the surface, there are several dramatic differences that are driving this new trend.

What is an ETF?

ETF stands for Exchange Traded Fund. On the surface, an ETF looks very similar to an index mutual fund. It’s a basket of securities often used to track an index or an investment theme. For example, Vanguard has the Vanguard S&P 500 Index EFT (Ticker: VOO), but they also have the Vanguard S&P 500 Index Fund (Ticker: VFIAX); both aim to track the performance of the S&P 500 Index, but there are a few differences.

ETFs Trade Intraday

Unlike a mutual fund that only trades at 4pm each day, an ETF can be traded like a stock intraday, so if you want to see $10,000 of the Vanguard S&P 500 ETF at 10am, you can do that, versus if you are invested in the Vanguard S&P 500 Index Fund, it will only trade at 4pm which may be at a better or worse price depending where the S&P 500 index finished the trading day compared to the price at 10am.

How ETFs Are Traded

When it comes to comparing ETFs to Mutual Funds, a big difference is not only WHEN they trade, but also HOW they trade. When you sell a mutual fund, your shares are sold back to the mutual fund company at 4pm and settled in cash. An exchange traded fund trades like a stock where shares are “exchanged” between a buyer and a seller in the open market, which is where ETF’s get their name from. They are “exchanged”, not redeemed like mutual fund shares.

ETF Tax Advantage Over Mutual Funds

One of the biggest advantages of ETFs over mutual funds is their tax efficiency, which relates back to what we just covered about how ETFs are traded. When you redeem mutual fund shares, if the fund company does not have enough in its cash reserve within the mutual fund itself, it has to go on the open market and sell securities to raise cash to meet the redemptions. Like any other type of investment account, if the security that they sell has an unrealized gain, selling the security to raise cash creates a taxable realized gain, and then the mutual fund distributes those gains to the existing shareholders, typically at the end of the calendar year as “capital gains distributions” which are then taxed to the current holders of the mutual funds.

If the current shareholders are holding that mutual fund in a taxable account when the capital gains distribution is issued, the shareholder needs to report that capital gains distribution as taxable income. This never seemed fair because that shareholder didn't redeem any shares, however since the mutual fund had to redeem securities to meet redemptions, the shareholders that remain unfortunately bear the tax burden.

Example: Jim and Sarah both own ABC Growth Fund in their brokerage accounts. ABC has performed well for the past few years, so Sarah decides to sell her shares. The mutual fund company then has to sell shares of stock within its portfolio to meet the redemption request, generating a taxable gain within the mutual fund portfolio. At the end of the year, ABC Growth Fund issues a capital gain distribution to Jim, which he must pay tax on, even though Jim did not sell his shares, Sarah did.

ETFs do not trigger capital gains distributions to shareholders because the shares are exchanged between a buyer and a seller, an ETF company does not have to redeem securities within its portfolio to meet redemptions. So, you could technically have an ABC Growth Mutual Fund and an ABC Growth ETF, same holdings, but the investor that owns the mutual fund could be getting hit with taxed on capital gains distribution each year while the holder of the ETF has no tax impact until they sell their shares.

Holding ETFs In A Taxable Account vs Retirement Account

Tax efficiency matters the most in taxable accounts, like brokerage accounts. If you are holding an ETF or mutual fund within an IRA or 401(k) account, since retirement accounts by nature are tax deferred, the capital gains distributions being issued by the mutual fund companies do not have an immediate tax impact on the shareholders because of the tax deferred nature of retirement accounts. For this reason, there has been less urgency to transition from mutual funds to ETFs in retirement accounts.

Many ETFs Don’t Trade In Fractional Shares

The second reason why ETFs have been slower to be adopted into employer sponsored retirement plans, like 401(k) plans, is most ETFs, like stocks, only trade in whole shares. Example: If you want to buy 1 share of Google, and Google is trading for $163 per share, you have to have $163 in cash to buy one whole share. You can’t buy $53 of Google because it’s not enough to purchase a whole share. Most ETF’s work the same way. They have a share price like a stock, and you have to purchase them in whole shares. Mutual funds by comparison trade in fractional shares, meaning while the “share price” or “NAV” of a mutual fund may be $80, you can buy $25.30 of that mutual fund because they can be bought and sold in fractional shares.

This is why from an operational standpoint, mutual funds can work better in 401(k) accounts because you have employees making all different levels of contributions each pay period to their 401(K) accounts - Jim is contributing $250 per pay period, Sharon $423 per pay period, Scott $30 per pay period. Since mutual funds can trade in fractional shares, the full amount of those contributions can be invested each pay period, whereas if it was a menu of ETFs that only traded in full shares, there would most likely be uninvested cash left over each pay period because only whole shares can be purchased.

ETF’s Do Not Have Minimum Initial Investments

Another advantage that ETF’s have over mutual funds is they do not have “minimum initial investments” like many mutual funds do. For example, if you look up the Vanguard S&P 500 Index Mutual Fund (Ticker VFIAX), there is a minimum initial investment of $3,000, meaning you must have at least $3,000 to buy a position in that mutual fund. Whereas the Vanguard S&P 500 Index ETF (Ticker: VOO) does not have a minimum initial investment, the current share price is $525.17, so you just need $525,17 to purchase 1 share.

NOTE: I’m not picking on Vanguard, they are in a lot of my example because we use Vanguard in our client portfolios, so we are very familiar with how their mutual funds and ETFs operate.

ETFs Do Not CLOSE To New Investors

Every now and then a mutual fund will declare either a “soft close” or “hard close”. A soft close means the mutual fund is closed to “new investors” meaning if you currently have a position in the mutual fund, you are allowed to continue to make deposits, but if you don’t already own the mutual fund, you can no longer buy it. A “hard close” is when both current and new investors are no longer allowed to purchase shares of the mutual fund, existing shareholders are only allowed to sell their holdings.

Mutual Funds will sometimes do this to protect performance or their investment strategy. If you are managing a Small Cap Value Mutual Fund and you receive buy orders for $100 billion, it may be difficult, if not impossible to buy enough of the publicly traded small cap stock to put that cash to work. Then, the fund manager might have to expand the stock holding to “B team” selections, or begin buying mid-cap stock which creates style drift out of the core small cap value strategy. To prevent this, the mutual fund will announce either a soft or hard close to prevent these big drifts from happening.

Arguably a good thing, but if you love the fund, and they tell you that you can’t put any more money into it, it can be a headache for current shareholders.

Since ETFs trade in the open market between buyers and sellers, they cannot implement hard or soft closes, it just becomes, ‘how much are the current holders of the ETF willing to sell their shares for in the open market to the buyers’.

ETFs Can Offer A Wider Selection of Investment Strategies

With ETFs, there are also a wider variety of investment strategies to choose from and the number of ETFs available in the open market are growing rapidly.

For example, if you want to replicate the performance of Brazil’s stock market within your portfolio, iShares has an ETF called MSCI Brazil (Ticker: EWZ) which seeks to track the investment results of an index composed of Brazilian equities. While traditional indexes exist within the ETF world like tracking the total bond market or S&P 500 Index, EFTs can provide access to more limited scope investment strategies.

ETF Liquidity Risk

But this brings me to one of the risks that shareholders need to be aware of when buying thinly traded ETFs. Since they are exchange traded funds, if you want to sell your position, you need a buyer that wants to buy your shares, otherwise there is no way to sell your position. One of the metrics we advise individuals to look at before buying an ETF is the daily trade volume of that security to determine how easily or difficult it would be to find a buyer for your shares if you wanted to sell them.

For example, VOO, the Vanguard S&P 500 Index ETF has an average trading volume right now about 5 million shares and as the current share price is about $2.6 Billion in activity each day, there is a high probability that if you wanted to sell $500,000 of your VOO, that order could be easily filled. If instead, you are holding a very thinly traded ETF that only has an average trading volume of 100,000 share per day and you are holding 300,000 shares, it may take you a few days or weeks to sell your position and your activity could negatively impact the price as you try to sell because it could move the market with your trade given the light trading volume. Or worse, there is no one interested in buying your shares, so you are stuck with them. You just have to do your homework when investing the more thinly traded ETFs.

Passive & Active ETFs

Similar to mutual funds, there are both passive and active ETF’s. Passive ETFs aim to replicate the performance of an existing index like the S&P 500 Index or a bond index, while active strategy ETFs are trying to outperform a specific index through the implementation of their investment strategy within the ETF.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

How do ETFs differ from mutual funds in how they trade?