Should I Gift A Stock To My Kids Or Just Let Them Inherit It?

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is largely influenced by the amount of appreciation or depreciation in the stock.

Gifting Stock

When you make a non-cash gift such as a stock, house, or even a business, the person receiving the gift assumes your cost basis in the assets. They do not receive a “step-up” in basis at the time the gift is made. Example, I buy XYZ Corp stock in 1995 for $10,000. In 2017, those shares of XYZ are now worth $100,000. If I gift them to my kids, no one owes tax on the gift at the time that the gift is made but my kids carry over my cost basis in the stock. If my kids hold the stock for 10 more years and sell it for $150,000, their basis in the stock is $10,000, and they owe capital gains tax on the $140,000 gain. Thus, creating an adverse tax consequence for my kids.

Inheriting Stock

Instead, let’s say I continue to hold XYZ stock and when I pass away my kids inherited the stock. If I pass away in 10 years and the stock is worth $150,000 then my kids receive a “step-up” in basis which means that their cost basis in the stock is the value of the stock as of the date of my death. They inherit the stock at $150,000 value, sell it the next day, and they owe $0 in taxes due to the step-up in basis upon my death.

In general, if you have assets that have low cost basis it is usually better for your heirs to inherit the assets as opposed to gifting it to them.

The concept is often times reversed for assets that have depreciated in value…..with an important twist. If I purchase XYZ Corp stock in 1995 for $10,000 but in 2017 it’s only worth $5,000, if I sold the stock myself I would capture the realized investment loss and could use it to offset investment gains or reduce my income by $3,000 for the IRS realized loss allowance.

Here is a very important rule......

In most cases, do not gift a depreciated asset to someone else. Why? When you gift an asset that has depreciated in value the carry over basis rules change. For an asset that has depreciated in value, the carry over basis for the person receiving the gift is the higher of the fair market value of the asset or the cost basis of the person making the gift. In other words, the loss evaporates when I gift the asset to someone else and no one gets the tax advantage of using the realized loss for tax purposes. It would be better if I sold the stock, captured the investment loss, and then gifted the cash.

If they inherit the stock that has lost value there is no value to the step-up in basis because the stock has not appreciated in value.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Inherited IRA's: How Do They Work?

An Inherited IRA is a retirement account that is left to a beneficiary after the owner’s death. It is important to have a general knowledge of how Inherited IRA’s work because a minor error in how the account is set up could lead to major tax consequences.

how do inherited ira's work

An Inherited IRA is a retirement account that is left to a beneficiary after the owner’s death. It is important to have a general knowledge of how Inherited IRA’s work because a minor error in how the account is set up could lead to major tax consequences.

Before going into the different kinds of Inherited IRA’s, if you are the sole beneficiary of your spouse’s IRA, you are able to transfer the assets to your own existing IRA or to a new IRA through what is called a “Spousal Transfer”. This account is not treated as an Inherited IRA and therefore is subject to all the rules a Traditional IRA would be subject to as if it was always held in your name. If the spouse needs to have access to the money before age 59 ½, it would probably make sense to set up an Inherited IRA because this would give the spouse options to access the money without incurring a 10% early withdrawal penalty.

Withdrawal Rules for Spouse & Non-Spouse Beneficiaries

The SECURE Act that passed in December 2019 dramatically changed the distribution options that are available to non-spouse beneficiaries. If you are spousal beneficiary please reference the following article:

10 Year Method

All the assets must be distributed by the 10th year after the year in which the account holder died. This option may make sense compared to the Lump Sum option explained next to spread out the tax liability over a longer period.

Lump Sum Distribution

You may take a lump sum distribution when the account is inherited. It is recommended that you consult your tax preparer to discuss the tax consequences of this method since you may move up into a different tax bracket.

Additional Takeaways

If the decedent was required to take a distribution in the year of death, it is important to determine whether or not the decedent took the distribution. If the decedent was required to take a RMD but did not do so in the year they passed, the inheritor must take the distribution based on the life expectancy of the decedent or the distribution will be subject to a 50% penalty. Distributions going forward will be based on the life expectancy of the inheritor.

It is important to be sure a beneficiary form is completed for the Inherited IRA. If there is no beneficiary and the account goes to an estate then the inheritor will have limited choices on which distribution method to choose among other tax consequences.

You are only able to combine Inherited IRA’s if they were inherited from the same individual. If you have multiple Inherited IRA’s from different individuals, you cannot commingle the assets because of the distributions that must be taken.

There is no 60 day rule with Inherited IRA’s like there is with other Traditional IRA’s. The 60 day rule allows someone to withdraw money from an IRA and as long as it’s replenished within 60 days there is no tax consequence. This is not available with Inherited IRA’s, all non-Roth distributions are taxable.

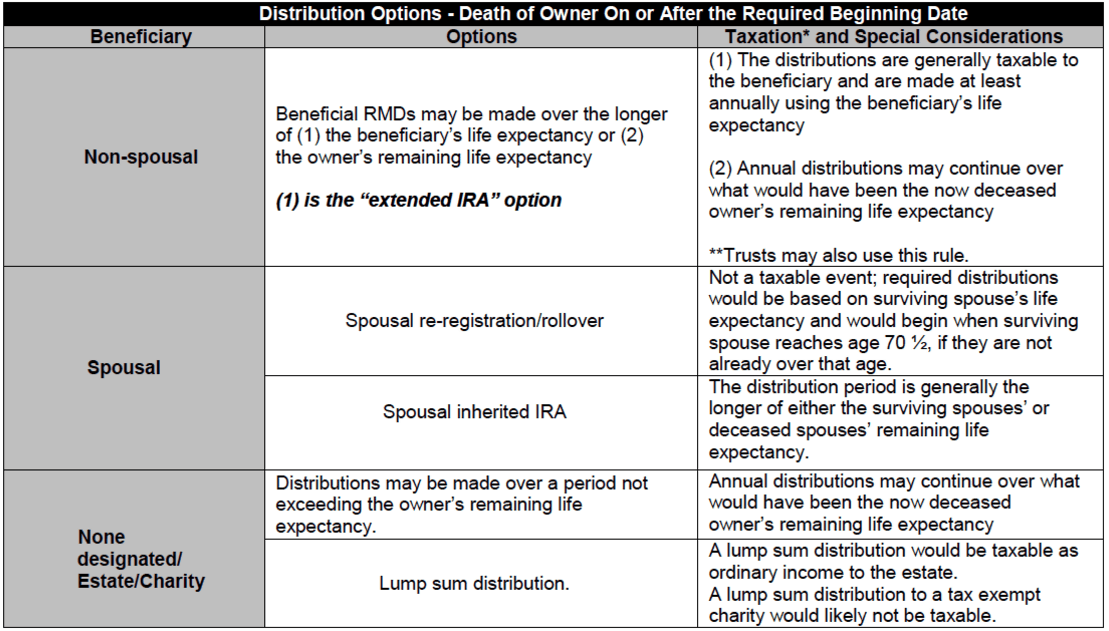

The charts below are from insurancenewsnet.com publication titled “Extended IRA Quick Reference Guide” give another look at the details of Inherited IRA’s.

inherited ira options

inherited ira distribution options

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.