STAR Property Tax Credit: Make Sure You Know The New Income Limits

The STAR Credit is a great way to reduce your property taxes in New York. If you are over the age of 65, it gets even better with the Enhanced STAR Credit. But you have to know the income limits associated with the credit otherwise you could unexpectedly lose the credit which could cost you thousands of dollars in additional property taxes. They

The STAR Credit is a great way to reduce your property taxes in New York. If you are over the age of 65, it gets even better with the Enhanced STAR Credit. But you have to know the income limits associated with the credit otherwise you could unexpectedly lose the credit which could cost you thousands of dollars in additional property taxes. They made some big changes to the credit that a lot of homeowners are not aware of. In this article we will review:

The income limits for the STAR Credit

Eligibility requirements for the Enhanced STAR Credit

How much money the STAR credit saves you

The most common mistakes that people make that disqualify them from the credit

The changes that were made to the property tax credit

STAR Property Tax Exemption

Let’s start with the basics. STAR stands for School Tax Relief. It’s a partial exemption from school taxes for your primary residence. There are two different STAR programs:

Basic STAR

Enhanced STAR

You Have To Apply For The Credit

You have to apply for the credit to receive it. It’s not automatic. Also, if you turn 65 this year and you want to further reduce your property taxes, there is a special application process for the Enhanced STAR Credit which requires you to enroll in the annual Income Verification Program (IVP). We will cover this in more detail later on in the article.

How Does The STAR Credit Work

The STAR credit exempts a specified dollar amount from the assessed value of your house prior to the calculation of your school tax bill. Here are the current exemption amounts:

Basic STAR: $30,000

Enhanced STAR: $65,000

The actual dollar amount that you save in school taxes will vary based on where you live in New York State. But if you live in a $300,000 house, you qualify for Basic STAR, and your school taxes before the STAR’s credit are $7,000. It could save you around $700 per year in school taxes. If you qualify for the enhanced STAR, you can more than double that savings number. In a high property tax state like New York, every little bit helps.

Income Limits For The STAR Credit

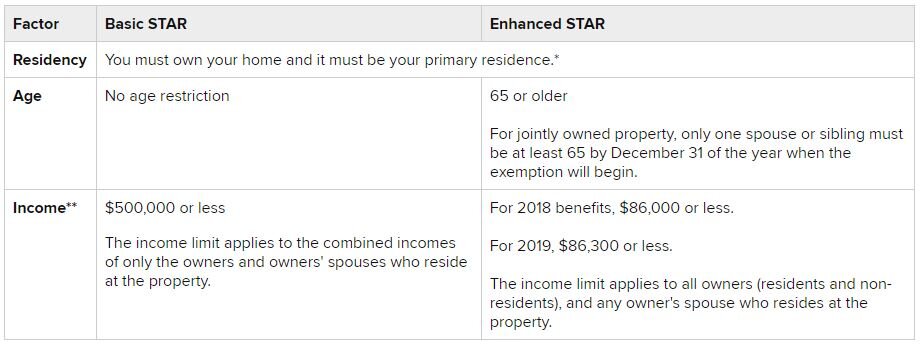

Here is a table from NYS Department of Taxation and Finance that summarizes the eligibility requirements for the Basic STAR and Enhanced STAR credit:

Requirement #1: It must be your primary residence. The credit does not apply for rental properties or second homes.

Requirement #2: To qualify for the Enhanced STAR, one of the homeowners must be age 65

Requirement #3: The income limitations. We see fewer issues with the Basic STAR since the income limit is $500,000. We see a lot more issues with the Enhanced STAR credit with the income limit at $86,300. Mainly because when you add up social security, pension payments, and required minimum distributions from IRA’s, you have homeowners that flirt with that income limit on a year by year basis. Crossing the income line would drop you back into the Basic STAR program which will most likely result in an unfriendly property tax surprise.

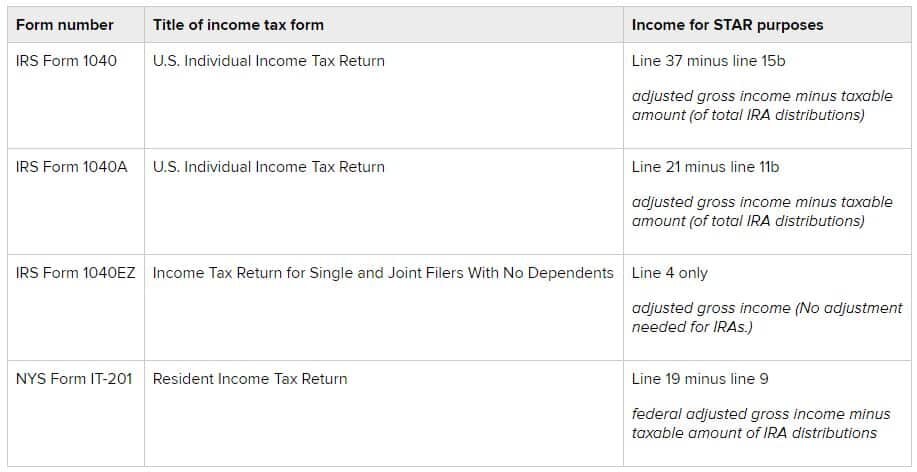

Income Calculation

The eligibility for the 2019 STAR credit is actually based on your income from 2017. You can reference your 2017 federal and state tax returns against the table listed below:

Enhanced STAR Credit

Once you or your spouse turn age 65, you are then eligible to apply for the Enhanced STAR program.

Unlike the basic STAR program, the Enhanced STAR program required homeowners to file renewal applications with their local assessor each year to remain in the program. Under the new rules, new applicants are required to enroll in the Enhanced STAR Income Verification Process.

The application deadline is typically March 1st if you are filing at the county level but it can vary from county to county. You should contact your assessor to verify the application deadline in your area. The good news about enrolling in the Enhance STAR Income Verification Program is you only have to do it once. Once enrolled you will receive the Enhanced STAR credit each year as long as your income is below the required threshold.

Common Mistakes With The Enhanced STAR Credit

Since the income threshold for the Enhanced STAR program is much lower than the Basic STAR program this is where we see homeowners get into trouble. For most retirees, their income is relatively the same from year to year. However, there are frequently one-time events that occur that can push a retiree’s income higher for a given year. Not only do they end up with a large tax bill when they file their taxes but they also find out that they lost the Enhanced STAR Credit for that year. Double ouch!!

Here are the most common income events that retirees have to watch out for:

Capital gains and dividends from taxable investment accounts

Taking larger distributions from IRA’s or pre-tax retirement plans

Age 70 ½ - Required minimum distributions start from IRA’s

Receive an inheritance (some sources can be taxable)

Sell real estate or land other than the primary residence

Surrendering a life insurance policy

Part-time income

The year you turn on social security benefits

If you experience financial events that are expected to increase your taxable income for a given year, you should work closely with you financial advisor or accountant during those years because there may be ways to reduce your income to maintain the Enhanced STAR credit with some advanced planning.

Changes To The STAR Credit

New York made some significant changes to both the Basic STAR and the Enhanced STAR credit that not many homeowners are aware of. The amount of the credit did not change but the methods for applying for and receiving the credit did change.

If you were receiving the Basic STAR credit before and you have not moved since 2016, there is nothing that you have to do. Everything will continue to operate the same. However, if you move or if you are new homeowner, the STAR process will be different. Under the old method, you would simply see a deduction for your STAR credit on your school tax bill. Going forward, when you buy a new house, you will have to pay your full school tax bill, and then New York will mail you a physical check for your STAR credit. In order to receive your check in September, you must register for the Basic STAR program through the state Department of Taxation and Finance by July 1st.

After July 1st, you can still apply for the STAR credit, and the state will provide you with a check, but you may receive the check after September. The same manual check process is applicable with the Enhanced STAR program as well.

If you were receiving the Enhanced STAR and you have not moved, New York is allowing those homeowners to continue to file their renewal applications with their local assessor each year without having to enroll in the new Enhanced STAR Income Verification Program. However, if you move, you will have to enroll in the Income Verification Program in order to remain in the Enhanced STAR Program.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Warning To All Employees: Review The Tax Withholding In Your Paycheck Otherwise A Big Tax Bill May Be Waiting For You

As a result of tax reform, the IRS released the new income tax withholding tables in January and your employer probably entered those new withholding amounts into the payroll system in February. It was estimated that about 90% of taxpayers would see an increase in their take home pay once the new withholding tables were implemented.

As a result of tax reform, the IRS released the new income tax withholding tables in January and your employer probably entered those new withholding amounts into the payroll system in February. It was estimated that about 90% of taxpayers would see an increase in their take home pay once the new withholding tables were implemented. While lower tax rates and more money in your paycheck sounds like a good thing, it may come back to bite you when you file your taxes.

The Tax Withholding Guessing Game

Knowing the correct amount to withhold for federal and state income taxes from your paycheck is a bit of a guessing game. Withhold too little throughout the year and when you file your taxes you have a tax bill waiting for you equal to the amount of the shortfall. Withhold too much and you will receive a big tax refund but that also means you gave the government an interest free loan for the year.

There are two items that tell your employer how much to withhold for federal income tax from your paycheck:

Income Tax Withholding Tables

Form W-4

The IRS provides your employer with the Income Tax Withholding Tables. On the other hand, you as the employee, complete the Form W-4 which tells your employer how much to withhold for taxes based on the “number of allowances” that you claim on the form.

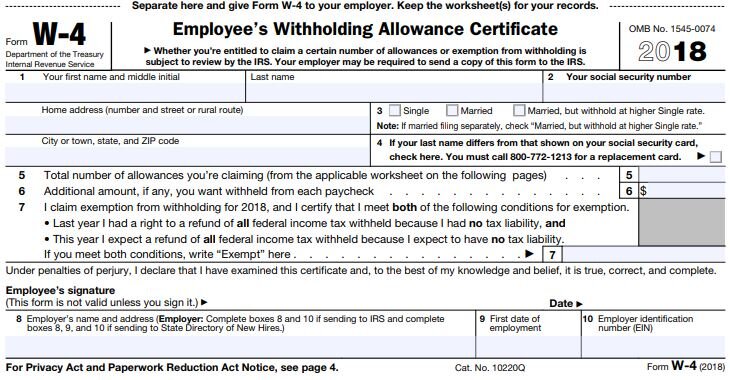

What Is A W-4 Form?

The W-4 form is one of the many forms that HR had you complete when you were first hired by the company. Here is what it looks like:

Section 3 of this form tells your employer which withholding table to use:

Single

Married

Married, but withhold at higher Single Rate

Section 5 tells your employer how many "allowances" you are claiming. Allowance is just another word for "dependents". The more allowances your claim, the lower the tax withholding in your paycheck because it assumes that you will have less "taxable income" because in the past you received a deduction for each dependent. This is where the main problem lies. Due to the changes in the tax laws, the tax deduction for personal exemptions was eliminated. This may adversely affect some taxpayers the were claiming a high number of allowances on their W-4 form because even though the number of their dependents did not change, their taxable income may be higher in 2018 because the deduction for personal exemptions no longer exists.

Even though everyone should review their Form W-4 form this year, employees that claimed allowances on their W-4 form are at the highest risk of either under withholding or over withholding taxes from their paychecks in 2018 due to the changes in the tax laws.

How Much Should I Withhold From My Paycheck For Taxes?

So how do you go about calculating that right amount to withhold from your paycheck for taxes to avoid an unfortunate tax surprise when you file your taxes for 2018? There are two methods:

Ask your accountant

Use the online IRS Withholding Calculator

The easiest and most accurate method is to ask your personal accountant when you meet with them to complete your 2017 tax return. Bring them your most recent pay stub and a blank Form W-4. Based on the changes in the tax laws, they can assist you in the proper completion of your W-4 Form based on your estimated tax liability for the year.If you complete your own taxes, I would highly recommend visiting the updated IRS Withholding Calculator. The IRS calculator will ask you a series of questions, such as:

How many dependents you plan to claim in 2018

Are you over the age of 65

The number of children that qualify for the dependent care credit

The number of children that will qualify for the new child tax credit

Estimated gross wages

How much fed income tax has already been withheld year to date

Payroll frequency

At the end of the process it will provide you with your personal results based on the data that you entered. It will provide you with guidance as to how to complete your Form W-4 including the number of allowances to claim and if applicable, the additional amount that you should instruct your employer to withhold from your paycheck for federal income taxes. Additional withholding requests are listed in Section 6 of the Form W-4.

Avoid Disaster

Having this conversation with your accountant and/or using the new IRS Withholding Calculator will help you to avoid a big tax disaster in 2018. Unfortunately, many employees may not learn about this until it's too late. Employees that are used to getting a tax refund may find out in the spring of next year that they owe thousands of dollars to the IRS because the combination of the new tax tables and the changes in the tax law that caused them to inadvertently under withhold federal income taxes throughout the year.

Action Item!!

Take action now. The longer you wait to run this calculation or to have this conversation with your accountant, the larger the adjustment may be to your paycheck. It's easier to make these adjustments now when you have nine months left in the year as opposed to waiting until November.I would strongly recommend that you share this article with your spouse, children in the work force, and co-workers to help them avoid this little known problem. The media will probably not catch wind of this issue until employees start filing their tax returns for 2018 and they find out that there is a tax bill waiting for them.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Big Changes For 401(k) Hardship Distributions

While it probably seems odd that there is a connection between the government passing a budget and your 401(k) plan, this year there was. On February 9, 2018, the Bipartisan Budget Act of 2018 was passed into law which ended the government shutdown by raising the debt ceiling for the next two years. However, also buried in the new law were

While it probably seems odd that there is a connection between the government passing a budget and your 401(k) plan, this year there was. On February 9, 2018, the Bipartisan Budget Act of 2018 was passed into law which ended the government shutdown by raising the debt ceiling for the next two years. However, also buried in the new law were changes to rules that govern hardship distributions in 401(k) plans.

What Is A Hardship Distribution?

A hardship distribution is an optional distribution feature within a 401(k) plan. In other words, your 401(k) plan may or may not allow them. To answer that question, you will have to reference the plan’s Summary Plan Description (SPD) which should be readily available to plan participants.

If your plan allows hardship distributions, they are one of the few in-service distribution options available to employees that are still working for the company. There are traditional in-service distributions which allow employees to take all or a portion of their account balance after reaching the age 59½. By contrast, hardship distributions are for employees that have experienced a “financial hardship”, are still employed by the company, and they are typically under the age of 59½.

Meeting The "Hardship" Requirement

First, you have to determine if your financial need qualifies as a "hardship". They typically include:

Unreimbursed medical expenses for you, your spouse, or dependents

Purchase of an employee's principal residence

Payment of college tuition and relative education costs such as room and board for the next 12 months for you, your spouse, dependents, or children who are no longer dependents.

Payment necessary to prevent eviction of you from your home, or foreclosure on the mortgage of your primary residence

For funeral expenses

Certain expenses for the repair of damage to the employee's principal residence

Second, there are rules that govern how much you can take out of the plan in the form of a hardship distribution and restrictions that are put in place after the hardship distribution is taken. Below is a list of the rules under the current law:

The withdrawal must not exceed the amount needed by you

You must first obtain all other distribution and loan options available in the plan

You cannot contribute to the 401(k) plan for six months following the withdrawal

Growth and investment gains are not eligible for distribution from specific sources

Changes To The Rules Starting In 2019

Plan sponsors need to be aware that starting in 2019 some of the rules surrounding hardship distributions are going to change in conjunction with the passing of the Budget Act of 2018. The reasons for taking a hardship distribution did not change. However, there were changes made to the rules associated with taking a hardship distribution starting in 2019. More specifically, of the four rules listed above, only one will remain.

No More "6 Month Rule"

The Bipartisan Budget Act of 2018 eliminated the rule that prevents employees from making 401(k) contributions until 6 months after the date the hardship distribution was issued. The purpose of the 6 month wait was to deter employees from taking a hardship distribution. In addition, for employees that had to take a hardship it was a silent way of implying that “if things are bad enough financially that you have to take a distribution from your retirement account, you probably should not be making contributions to your 401(k) plan for the next few months.”

However, for employees that are covered by a 401(k) plan that offers an employer matching contribution, not being able to defer in the plan for 6 months also meant no employer matching contribution during that 6 month probationary period. Starting in 2019, employees will no longer have to worry about that limitation.

Loan First Rule Eliminated

Under the current 401(k) rules, if loans are available in the 401(k) plan, the plan participant was required to take the maximum loan amount before qualifying for a hardship distribution. That is no longer a requirement under the new law.

We are actually happy to see this requirement go away. It never really made sense to us. If you have an employee, who’s primary residence is going into foreclosure, why would you make them take a loan which then requires loan payments to be made via deductions from their paycheck? Doesn’t that put them in a worse financial position? Most of the time when a plan participant qualifies for a hardship, they need the money as soon as possible and having to go through the loan process first can delay the receipt of the money needed to remedy their financial hardship.

Earnings Are Now On The Table

Under the current 401(k) rules, if an employee requests a hardship distribution, the portion of their elective deferral source attributed to investment earnings was not eligible for withdrawal. Effective 2019, that rule has also changed. Both contributions and earnings will be eligible for a hardship withdrawal.

Still A Last Resort

We often refer to hardship distributions as the “option of last resort”. This is due to the taxes and penalties that are incurred in conjunction with hardship distributions. Unlike a 401(k) loan which does not trigger immediate taxation, hardship distributions are a taxable event. To make matters worse, if you are under the age of 59½, you are also subject to the 10% early withdrawal penalty.

For example, if you are under the age of 59½ and you take a $20,000 hardship distribution to make the down payment on a house, you will incur taxes and the 10% penalty on the $20,000 withdrawal. Let’s assume you are in the 24% federal tax bracket and 7% state tax bracket. That $20,000 distribution just cost you $8,200 in taxes.

Gross Distribution: $20,000

Fed Tax (24%): ($4,800)

State Tax (7%): ($1,400)

10% Penalty: ($2,000)

Net Amount: $11,800

There is also an opportunity cost for taking that money out of your retirement account. For example, let’s assume you are 30 years old and plan to retire at age 65. If you assume an 8% annual rate of return on your 401(K) investment that $20,000 really cost you $295,707. That’s what the $20,000 would have been worth, 35 years from now, compounded at 8% per year.

Plan Amendment Required

These changes to the hardship distribution rule will not be automatic. The plan sponsor of the 401(k) will need to amend the plan document to adopt these new rules otherwise the old hardship distribution rules will still apply. We recommend that companies reach out to their 401(k) providers to determine whether or not amending the plan to adopt the new hardship distribution rules makes sense for the company and your employees.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

What Happened The Last Time The Dow Dropped By More Than 4% In A Day?

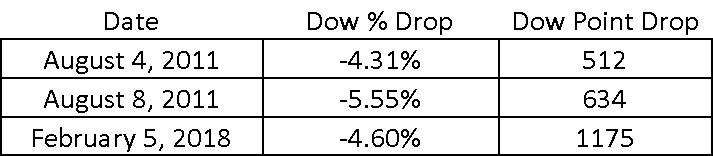

Yesterday was an “ouch”. The Dow Jones Industrial average dropped by more than 1000 points resulting in a 4.60% drop in the value of the index. While yesterday marked the largest “point” decline in the history of the Dow Jones Index, it was not anywhere near the largest percentage decline which is the metric that we care about.

Yesterday was an “ouch”. The Dow Jones Industrial average dropped by more than 1000 points resulting in a 4.60% drop in the value of the index. While yesterday marked the largest “point” decline in the history of the Dow Jones Index, it was not anywhere near the largest percentage decline which is the metric that we care about.

Below is a chart that shows the largest daily “point” losses in the history of the Dow Jones Industrial Index:

You will find yesterday at the top of the chart. Now look at the column all the way to the right labelled “% change”. You will notice that while yesterday topped the chart from a point decline, it does not come anywhere near the largest percentage decline that we have seen. In fact, it does not even make it in the top 20 worse days for the Dow. See the chart below that shows the largest daily percentage declines in the Dow’s history:

What Happened Last Time?

Whenever there is a big drop in the stock market, I immediately start looking back in history to find market events that are similar to the current one. So when was the last time the market dropped by more than 4% in a single day?

The answer: August 8, 2011

If you remember, 2011 was the start of the European Sovereign Debt Crisis. That was when Greece, Portugal, Spain, and Ireland announced that they were unable to repay their government debt and needed a bailout package from the European Union to survive. There were two single day declines in the month of August that rivaled what we saw yesterday.

How Long Did It Take The Market To Come Back?

If we are looking to history as a guide, how long did it take for the market to recoup the losses after these large single day declines? On July 31, 2011 the Dow Jones Industrial closed at 11,444, the Europe debt crisis hit, and the market experienced those two 4%+ decline days on August 4th and August 8th. By September 11, 2011, the Dow Jones closed at 11,509, recouping all of its losses from the beginning of August. Thus making the answer to the question: 38 days. The market took 38 days to recoup all of the losses from not one but two 4%+ decline days in 2011.

We Don’t Have A Crisis

The main difference between 2011 and now is we don’t have a global economic crisis. In my opinion, the market correction in 2011 was warranted. There was a real problem in Europe. We were not sure how and if those struggling Eurozone countries could be saved so the market dropped.

The only trigger that I hear analysts pointing to in an effort to explain the selloff yesterday is the 2.9% wage growth number that we got on Friday. This in turn has sparked inflation fears and in reaction, the Fed may decide to hike rates four times this year instead of three. Hardly a “crisis”. Outside of that nothing else meaningful has happened to trigger the volatility that we are seeing in the stock market. OK……so what should you do in reaction to this? Sometimes the right answer is “nothing”. It’s difficult to hear that because emotionally you want to pull money out of the market and run to cash or bonds but absent a sound economic reason for making that move, at this point, the best investment decision may be to just stay the course.

We Have Forgotten What Volatility Feels Like

When you are in a market environment like 2017, you very quickly forget what normal market volatility feels like. In 2017, the stock market just gradually climbed throughout the year without any hiccups. That’s not normal. Below is a chart that shows the magnitude of market corrections each year going back to 1990. As you will see, on average, when the economy is not in a recession, the market averages an 11.56% correction at some point during the year. In 2017, we only experienced a 3% correction.

intra year drops in the S&P 500 Index

Now the next chart shows you the big picture. Not only does it illustrate the amount of the largest market correction during the year but it also shows the return of the S&P 500 for the year.

Look at 2016. In 2016, at some point in the year the S&P 500 Index dropped by 11%. If you just held through it, the S&P 500 returned 10% for the year.

In 2011, the S&P 500 dropped by 19% during the year!! If you didn’t sell and just held through the volatility, you would have had a breakeven year.

Easier Said Than Done

Every big market correction feels like a new world ending crisis. It’s not. We have been fortunate enough to have a nice easy ride for the past 12 months but it seems like we are returning to more historical levels of volatility. Days like February 5, 2018 will test your patience and make you feel compelled to react. It’s easy to look back and confess that “yes, I should have just held through it” but it’s easier said than done.

It’s important to understand the catalysts that are driving the volatility in the markets. Sometimes the markets are dropping for a good reason and other times it’s just plain old fashion volatility. Based on what we have seen over the past few days and absent the emergence of a new economic, political, or global crisis, we expect it to be the later of the two.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

More Taxpayers Will Qualify For The Child Tax Credit

There is great news for parents in the middle to upper income tax brackets in 2018. The new tax law dramatically increased the income phaseout threshold for claiming the child tax credit. In 2017, parents were eligible for a $1,000 tax credit for each child under the age of 17 as long as their adjusted gross income (“AGI”) was below $75,000 for single

There is great news for parents in the middle to upper income tax brackets in 2018. The new tax law dramatically increased the income phaseout threshold for claiming the child tax credit. In 2017, parents were eligible for a $1,000 tax credit for each child under the age of 17 as long as their adjusted gross income (“AGI”) was below $75,000 for single filers and $110,000 for married couples filing a joint return. If your AGI was above those amounts, the $1,000 credit was reduced by $50 for every $1,000 of income above those thresholds. In other words, the child tax credit completely phased out for a single filer with an AGI greater than $95,000 and for a married couple with an AGI greater than $130,000.

Note: If you are not sure what the amount of your AGI is, it’s the bottom line on the first page of your tax return (Form 1040).

New Phaseout Thresholds In 2018+

Starting in 2018, the new phaseout thresholds for the Child Tax Credit begin at the following AGI levels:

Single Filer: $200,000

Married Filing Joint: $400,000

If your AGI falls below these thresholds, you are eligible for the full Child Tax Credit. For taxpayers with an AGI amount that exceeds these thresholds, the phaseout calculation is the same as 2017. The credit is reduced by $50 for every $1,000 in income over the AGI threshold.

Wait......It Gets Better

Not only will more families qualify for the child tax credit in 2018 but the amount of the credit was doubled. The new tax law increased the credit from $1,000 to $2,000 for each child under the age of 17.

In 2017, a married couple, with three children, with an AGI of $200,000, would have received nothing for the child tax credit. In 2018, that same family will receive a $6,000 tax credit. That’s huge!! Remember, “tax credits” are more valuable than “tax deductions”. Tax credits reduce your tax liability dollar for dollar whereas tax deductions just reduce the amount of your income subject to taxation.

Tax Reform Giveth & Taketh Away

While the change to the tax credit is good news for most families with children, the elimination of personal exemptions starting in 2018 is not.

In 2017, taxpayers were able to take a tax deduction equal to $4,050 for each dependent (including themselves) in addition to the standard deduction. For example, a married couple with 3 children and $200,000 in income, would have been eligible received the following tax deductions:

Standard Deduction: $12,700

Husband: $4,050

Wife: $4,050

Child 1: $4,050

Child 2: $4,050

Child 3: $4,050

Total Deductions $32,950

Child Tax Credit: $0

This may lead you to the following question: “Does the $6,000 child tax credit that this family is now eligible to receive in 2018 make up for the loss of $20,250 ($4,050 x 5) in personal exemptions?”

By itself? No. But you have to also take into consideration that the standard deduction is doubling in 2018. For that same family, in 2018, they will have the following deductions and tax credits:

Standard Deduction: $24,000

Personal Exemptions: $0

Total Deductions: $24,000

Child Tax Credit: $6,000

Even though $24,000 plus $6,000 is not greater than $32,950, remember that credits are worth more than tax deductions. In 2017, a married couple, with $200,000 in income, put the top portion of their income subject to the 28% tax bracket. Thus, $32,950 in tax deductions equaled a $9,226 reduction in their tax bill ($32,950 x 28%).

In 2018, due to the changes in the tax brackets, instead of their top tax bracket being 28%, it’s now 24%. The $24,000 standard deduction reduces their tax bill by $5,760 ($24,000 x 24%) but now they also have a $6,000 tax credit with reduces their remaining tax bill dollar for dollar, resulting in a total tax savings of $11,760. Taxes saved over last year: $2,534. Not a bad deal.

For many families, the new tax brackets combined with the doubling of the standard deduction and the doubling of the child tax credit with higher phaseout thresholds, should offset the loss of the personal exemptions in 2018.

This information is for educational purposes only. Please consult your accountant for personal tax advice.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform Could Lead To A Spike In The Divorce Rate In 2018

The Tax Cut & Jobs Act that was recently passed has already caused taxpayers to accelerate certain financial decisions as we transition from the current tax laws to the new tax laws over the course of the next two years.

The Tax Cut & Jobs Act that was recently passed has already caused taxpayers to accelerate certain financial decisions as we transition from the current tax laws to the new tax laws over the course of the next two years.

Current Tax Law: Alimony Is Tax Deductible

Under the current tax law, alimony payments are taxable income to the ex-spouse receiving the payments and they are tax deductible to the ex-spouse making the payments. When alimony is awarded pursuant to a divorce, it’s typically because there was a disparity in the level of income between the two spouses during the marriage. The ex-spouse paying the alimony, in most cases, is the higher income earning spouse both before and after the divorce finalized.

Let’s look at this in a real life example. Jim and Sarah have decided to get a divorce. Jim makes $300,000 per year and Sarah is a homemaker with $0 income. Pursuant to the divorce agreement, Jim will be required to pay Sarah $50,000 per year for 5 years. Jim will be able to deduct the $50,000 each year against his taxable income and Sarah will claim the $50,000 as taxable income on her tax return. Based on the 2018 Individual Tax Brackets, the top end of Jim’s income is in the 35% tax bracket. Thus, paying $50,000 in alimony really results in an “after-tax” expense to Jim of $32,500.

$50,000 x 35% = $17,500 (fed tax savings)

$50,000 – $17,500 = $32,500 (after tax expense to Jim)

Sarah will claim that $50,000 in alimony payments as income and let’s assume that the alimony payments are her only income for the year. Next year, as a single filer, Sarah will receive a standard deduction of $12,000, and the remainder of the $38,000 will be taxed at a blend of her 10% & 12% tax rate. As a result, Sarah will only pay about $4,400 in taxes on the $50,000 in alimony income.

To sum it all up, if the $50,000 is taxed to Sarah, approximately $4,400 will be paid to the IRS in taxes and she nets $45,600 in after tax income. However, if Jim was not able to deduct the alimony payments and had to pay tax on that $50,000, he would first have to pay the $17,500 in taxes to the IRS, and then he would hand Sarah a check for $32,500 after tax. Sarah is worse off because she received less after tax income. Jim would ultimately be worse off because he would need to part with more pre-tax income to create the same after tax benefit for Sarah. The IRS is the only one that wins.

Gaming The System

Since divorce agreements, in most states, are not required to adhere to predefined calculations for splitting assets, alimony payments, and in some cases child support, the tax game can be played when there is a high income earning spouse and alimony payments in the mix. In exchange for fewer assets or less child support, some divorce agreements have purposefully shifted more to alimony. The ex-spouse with the big income gets a bigger tax deduction and the ex-spouse receiving the alimony payment is able to take full advantage of their lower tax brackets and maximize their after tax income.

Alimony Is No Longer Deductible

To stop the tax game, included in the new tax bill was a provision that specifically states that alimony payments will no longer be deductible by the payor, nor reportable as income by the recipient, for divorce agreements signed after December 31, 2018.

The good news is this will not impact the ability to deduct alimony payments for divorce agreements that are currently in place. The bad news is for divorce agreements signed after December 31, 2018, the high income earner will no longer be able to deduct the alimony payments. That eliminates the tax arbitrage that has been used in the past to make the pie larger for both spouses. In general, if you shrink the size of the asset and income pie, it leaves more to fight about because each spouse is trying to preserve their standard of living as much as possible post-divorce.

For couples that have been sitting on the fence about getting divorced, this could be the catalyst to start the process in 2018 to make sure they have a signed agreement prior to December 31, 2018.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: Changes To 529 Accounts & Coverdell IRA's

Included in the new tab bill were some changes to the tax treatment of 529 accounts and Coverdell IRA's. Traditionally, if you used the balance in the 529 account to pay for a "qualified expense", the earnings portion of the account was tax and penalty free which is the largest benefit to using a 529 account as a savings vehicle for college.So what's the

Included in the new tab bill were some changes to the tax treatment of 529 accounts and Coverdell IRA's. Traditionally, if you used the balance in the 529 account to pay for a "qualified expense", the earnings portion of the account was tax and penalty free which is the largest benefit to using a 529 account as a savings vehicle for college.So what's the change? Prior to the Tax Cuts and Jobs Act (tax reform), qualified distributions were only allowed for certain expenses associated with the account beneficiary's college education. Starting in 2018, 529 plans can also be used to pay for qualified expenses for elementary, middle school, and high school.

Kindergarten – 12th Grade Expenses

Tax reform included a provision that will allow owners of 529 account to take tax-free distributions from 529 accounts for K – 12 expenses for the beneficiary named on the account. This is new for 529 accounts. Prior to this provision, 529 accounts could only be used for college expenses. Now 529 account holders can distribute up to $10,000 per student per year for K – 12 qualified expenses. Another important note, this is not limited to expenses associated with private schools. K – 12 qualified expense will be allowed for:

Private School

Public School

Religious Schools

Homeschooling

529 Accounts Will Largely Replace Coverdell IRA's

Prior to this rule change, the only option that parents had to save and accumulate money tax-free to K – 12 expenses for their children were Coverdell IRA's. But Coverdell IRA's had a lot of hang ups

Contributions were limited to $2,000 per year

You could only contribute to a Coverdell IRA if your income was below certain limits

You could not contribution to the Coverdell IRA after your child turned 18

Account balance had to be spend by the time the student was age 30

By contrast, 529 accounts offer a lot more flexibility and higher contributions limits. For example, 529 accounts have no contribution limits. The only limits that account owners need to be aware of are the "gifting limits" since contributions to 529 accounts are considered a "gift" to the beneficiary listed on the account. In 2018, the annual gift exclusion will be $15,000. However, 529 accounts have a provision that allow account owners to make a "5 year election". This election allows account owners to make an upfront contribution of up to 5 times the annual gift exclusion for each beneficiary without trigger the need to file a gift tax return. In 2018, a married couple could contribution up to $150,000 for each child to a 529 account without trigger a gift tax return.If I have a child in private school, they are in 6th grade, and I'm paying $20,000 in tuition each year, that means I have $140,000 that I'm going to spend in tuition between 6th grade – 12th grade and then I have college tuition to pile on top of that amount. Instead of saving that money in an after-tax investment account which is not tax sheltered and I pay capital gains tax when I liquidate the account to pay those expenses, why not setup a 529 account and shelter that huge dollar amount from income tax? It will probably saves me thousands, if not tens of thousands of dollars in taxes, in taxes over the long run. Plus, if I live in a state that allows tax deductions for 529 contributions, I get that benefit as well.

Income Limits and Tax Deductions

Unlike Coverdell IRA's, 529 accounts do not have income restrictions for making contributions. Plus, some states have a state tax deduction for contributions to 529 account. In New York, a married couple filing joint, receive a state tax deduction for up to $10,000 for contribution to 529 account. A quick note, that is $10,000 in aggregate, not $10,000 per child or per account.

Rollovers Count Toward State Tax Deductions

Here is a fun fact. If you live in New York and you have a 529 account established in another state for your child, if you rollover the balance into a NYS 529 account, the rollover balance counts toward your $10,000 annual NYS state tax deduction. Also, you can rollover balances in Coverdell IRA's into 529 accounts and my guess is many people will elect to do so now that 529 account can be used for K – 12 expenses.

Contributions Beyond Age 18

Unlike Coverdell IRA's which restrict contributions once the child reaches age 18, 529 accounts have no age restriction for contributions. We will often encourage clients to continue to contribute their child's 529 account while they are attending college for the sole purpose of continuing to capture the state tax deduction. If you receive the tuition bill in the mail today for $10,000, you can send in a $10,000 check to your 529 account provider as a current year contribution, as soon as the check clears the account you can turn around and request a qualified withdrawal from the account for the tuition bill, and pay the bill with the cash that was distributed from the 529 account. A little extra work but if you live in NYS and you are in a high tax bracket that $10,000 deduction could save you $600 - $700 in state taxes.

What Happens If There Is Money Left In The 529 Account?

If there is money left over in a 529 account after the child has graduated from college, there are a number of options available. For more on this, see our article "5 Options For Money Left Over In College 529 Plans"

Qualified Expenses

The most frequent question that I get is "what is considered a qualified expense for purposes of tax-free withdrawals from a 529 account?" Here is a list of the most common:

Tuition

Room & Board

Technology Items: Computers, Printers, Required Software

Supplies: Books, Notebooks, Pens, Etc.

Just as important, here are a list of expense that are NOT considered a "qualified expense" for purposes of tax free withdrawals from a 529 account:

Transportation & Travel: Expense of going back and forth from school / college

Student Loan Repayment

General Electronics and Cell Phone Plans

Sports and Fitness Club Memberships

Insurance

If there is ever a question as to where or not an expense is a qualified expense or not, I would recommend that you contact the provider of your 529 account before making the withdrawal form your 529 account. If you take a withdrawal for an expense that is not a "qualified expenses" you will pay income taxes and a 10% penalty on the earnings portion of the withdrawal.

Do I Have To Close My Coverdell IRA?

While 529 accounts have a number of advantages compared to Coverdell IRA's, current owners of Coverdell IRAs will not be required to close their accounts. They will continue to operate as they were intended. Like 529 accounts, Coverdell IRA withdrawals will also qualify for the tax-free distributions for K – 12 expenses including the provision for expenses associated with homeschooling.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Pass-Through Income Will Be Taxed For Small Business Owners

While one of the most significant changes incorporated in the new legislation was reducing the corporate tax rate from the current 35% rate to a 21% rate in 2018, the tax bill also contains a big tax break for small business owners. Unlike large corporations that are taxed at a flat rate, most small businesses, are "pass-through" entities, meaning that the

While one of the most significant changes incorporated in the new legislation was reducing the corporate tax rate from the current 35% rate to a 21% rate in 2018, the tax bill also contains a big tax break for small business owners. Unlike large corporations that are taxed at a flat rate, most small businesses, are "pass-through" entities, meaning that the profits from the business flow through to the business owner's personal tax return and then are taxed at ordinary income tax rates.While pass-through income will continue to be taxed at ordinary income tax rates, many small business owners will be eligible to deduct 20% of their "qualified business income" (QBI) starting in 2018. In other words, some pass-through entities will only be taxes on 80% of their pass-through income.

Pass-through entities include

Sole proprietorships

Partnerships

LLCs

S-Corps

Unanswered Questions

I wanted to write this article to give our readers the framework of what we know at this point about the treatment of the pass-through income in 2018. However, as many accountants will acknowledge, there seems to be more questions at this point then there are answers. The IRS will need to begin issuing guidance at the beginning of 2018 to clear up many of the unanswered questions as to who will be eligible and not eligible for the new 20% deduction.

Above or Below "The Line"

This 20% deduction will be a below-the-line deduction which is an important piece to understand. Tax lingo makes my head spin as well, so let's pause for a second to understand the difference between an "above-the-line deduction" and a "below-the-line deduction".The "line" refers to the AGI line on your tax return which is the bottom line on the first page of your Form 1040. While both above-the-line and below-the-line deductions reduce your taxable income, it's important to understand the difference between the two.

Above-The-Line Deductions

Above-the-line deductions happen on the first page of your tax return. These deductions reduce your gross income to eventually reach your AGI (adjusted gross income) for the year. Above-the-line deductions include:

Contributions to health savings accounts

Contributions to retirement plans

Deduction for one-half of the self-employment taxes

Health insurance premiums paid

Alimony paid, student loan interest, and a few others

The AGI is important because the AGI is used to determine your eligibility for certain tax credits and it will also have an impact on which below-the-line deductions you are eligible for. In general, the lower your AGI is, the more deductions and credits you are eligible to receive.

Below-The-Line Deductions

Below-the-line deductions are reported on lines that come after the AGI calculation. They are comprised mainly of your “standard deduction” or “itemized deductions” and “personal exemptions” (most of which will be gone starting in 2018). The 20% deduction for qualified business income will fall into this below-the-line category. It will lower the income of small business owners but it will not lower their AGI.

However, it was stated in the tax legislation that even though the 20% qualified business deduction will be a below –the-line deduction it will not be considered an “itemized deduction”. This is a huge win!!! Why? If it’s not an itemized deduction, then small business owners can claim the 20% qualified business income deduction and still claim the standard deduction. This is an important note because many small business owners may end up taking the standard deduction for the first time in 2018 due to all of the deductions and tax exemptions that were eliminated in the new tax bill. The tax bill took away a lot of big deductions:

Capped state and local taxes at $10,000 (this includes state income taxes and property taxes)

Eliminated personal exemptions ($4,050 for each individual) (Eliminated in 2018)

Family of 4 = $4,050 x 4 = $16,200 (Eliminated in 2018)

Miscellaneous itemized deductions subject to 2% of AGI floor (Eliminated in 2018)

Restrictions On The 20% Deduction

If life were easy, you could just assume that I'm a sole proprietor, I make $100,000 all in pass-through income, so I will get a $20,000 deduction and only have to pay tax on $80,000 of my income. For many small business owners it may be that easy but what's a tax law without a list of restrictions.The restriction were put in place to prevent business owners from reclassifying their W2 wages into 100% pass-through income to take advantage of the 20% deduction . They also wanted to restrict employees from leaving their company as a W2 employee, starting a sole proprietorship, and entering into a sub-contractor relationship with their old employer just to reclassify their W2 wages into 100% pass-through income.

S-Corps

Qualified business income will specifically exclude "reasonable compensation" paid to the owner-employee of an S-corp. While it would seem like an obvious reaction by S-corp owners to reduce their W2 wages in 2018 to create more pass through income, they will still have to adhere to the "reasonable compensation" restriction that exists today.

Partnerships & LLCs

Qualified business income will specifically exclude guaranteed payments associated with partnerships and LLCs. This creates a grey area for these entities. Partnerships do not have a “reasonable compensation” requirement like S-corps since companies taxed as partnerships are not allowed to pay W2 wages to the owners. Also the owners of partnerships are not required to take guaranteed payments. My guess is, and this is only a guess, that as we get further into 2018, the IRS may require partnerships to classify a percentage of a owners total compensation as a “guaranteed payment” similar to the “reasonable compensation” restriction that S-corps currently adhere too. Otherwise, partnerships can voluntarily eliminate guaranteed payments and take the 20% deduction on 100% of the pass-through income.

This may also prompt some S-corps to look at changing their structure to a partnership or LLC. For high income earners, S-corps have an advantage over the partnership structure in that the owners do not pay self-employment tax on the pass-through income that is distribution to the owner over and above their W2 wages. However, S-corp owners will have to weigh the self-employment tax benefit against the option of changing their corporate structure to a partnership and potentially receiving a 20% deduction on 100% of their income.

Sole Proprietors

Sole proprietors do not have "reasonable compensation" requirement or "guaranteed payments" so it would seem that 100% of the income generated by sole proprietors will count as qualified business income. Unless the IRS decides to enact a "reasonable compensation" requirement for sole proprietors in 2018, similar to S-corps. Before everyone runs from a single member LLC to a sole proprietorship, remember, a sole proprietorship offers no liability barrier between the owner and liabilities that could arise from the business.

Income Restrictions

There are limits that are imposed on the 20% deduction based on how much the owner makes in “taxable income”. The thresholds are set at the following amounts:

Individual: $157,500

Married: $315,000

The thresholds are based on each business owner’s income level, not on the total taxable income of the business. We need help from the IRS to better define what is considered “taxable income” for purposes of this phase out threshold. As of right now, it seems that “taxable income” will be defined as the taxpayer’s own taxable income (not AGI) less deductions.

If the owner’s taxable income is below this threshold, then the calculation is a simple 20% deduction of the pass-through income. If the owner’s taxable income exceeds the threshold, the qualified business deduction is calculated as follows:

The LESSER of:

20% of its business income OR 50% of the total wages paid by the business to its employees

Let’s look at this in a real life situation. A manufacturing company has a net profit of $2M in 2018 and pays $500,000 in wages to its employees during the year. That company would only be able to take the qualified business income deduction for $250,000 since 50% of the total employee wages ($500,000 x 50% = $250,000) are less than 20% of the net income of the business ($2M x 20% = $400,000).

This creates another grey area because it seems that the additional calculation is triggered by the taxable income of each individual owner but the calculation is based on the total profitability and wages paid by the company. For the owners that required this special calculation for exceeding the threshold, how is their portion of the lower deduction amount allocated? Multiplying the lower total deduction amount by the percent of their ownership? Just more unanswered questions.:

Restrictions For "Service Business"

There will be restrictions on the 20% deduction for pass-through entities that are considered a "service business" under IRC Section 1202(e)(3)(A). The businesses specifically included in this definition as a services business are:

Health

Law

Accounting

Actuarial Sciences

Performing Arts

Consulting

Athletics

Financial Services

Any other trade or business where the principal asset of the business is the reputation or skill of 1 or more of its employees

In a last minute change to the regulations, to their favor, engineers and architects were excluded from the definition of “service businesses”.

This is another grey area. Many small businesses that fall outside of the categories listed above will undoubtedly be asking the question: “Am I considered a service business or not?” Outside of the industries specifically listed in the tax bill, we really need more guidance from the IRS.

If you are a “services business”, when the tax reform was being negotiated it looked like service businesses were going to be completely excluded from the 20% deduction. However, the final regulations were more kind and instead implemented a phase out of the 20% deduction for owners of service businesses over a specified income threshold. The restriction will only apply to those whose “taxable income” exceeds the following thresholds:

Individual: $157,500

Married: $315,000

If you are a consultant or owner of a services business and your taxable income is below these thresholds, it would seem at this point that you will be able to capture the 20% deduction for your pass-through income. As mentioned above, we need help from the IRS to clarify the definition of “taxable income”.

Phase Out For Service Businesses

The amounts listed above: $157,500 for individual and $315,000 for a married couple filing joint, are where the thresholds for the phase out begins. The service business owners whose income rises above those thresholds will phase out of the 20% deduction over the next $50,000 of taxable income for individual filers and $100,000 of taxable income for married filing joint. This means that the 20% pass-through deduction is completely gone by the following income levels:

Individual: $207,500

Married: $415,000

Any taxpayer’s falling in between the threshold and the phase out limit will receive a portion of the 20% deduction.

Since the thresholds are assessed based on the taxpayer’s own taxable income and not the total income of the business, a service business could be in a situation, like in an accounting firm, where the partners with the largest ownership percentage may not qualify for 20% deduction but the younger partners may qualify for the deduction because their income is lower.

Tax Planning For 2018

It's an understatement to say that most small business owners will need to spend a lot of time with their accountant in the first quarter of 2018 to determine the best of course of action for their company and their personal tax situation.While we are still waiting for clarification on a number of very important items associated with the 20% deduction for qualified business income, hopefully this article has provided our small business owners with a preview of things to come in 2018.

Disclosure: I'm a Certified Financial Planner® but not an accountant. The information contained in this article was generated from hours and hours of personal research on the topic. I advise each of our readers to consult with your personal tax advisor for tax advice.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: Summary Of The Changes

The conference version of the tax bill was released on Friday. The House and the Senate will be voting to approve the updated tax bill this week with what seems to be wide spread support from the Republican party which is all they need to sign the bill into law before Christmas. Most of the changes will not take effect until 2018 with new tax rates for

The conference version of the tax bill was released on Friday. The House and the Senate will be voting to approve the updated tax bill this week with what seems to be wide spread support from the Republican party which is all they need to sign the bill into law before Christmas. Most of the changes will not take effect until 2018 with new tax rates for individuals set to expire in 2025. At which time the tax rates and brackets will return to their current state. Here is a run down of some of the main changes baked into the updated tax bill:

Individual Tax Rates

They are keeping 7 tax brackets with only minor changes to percentages in each bracket. The top tax bracket was reduced from 39.6% to 37%.

Capital Gains Rates

There were no changes to the capital gains rates and they threw out the controversial mandatory FIFO rule for calculating capital gains tax when selling securities.

Standard Deduction and Personal Exemptions

They did double the standard deduction limits. Single tax payers will receive a $12,000 standard deduction and married couples filing joint will receive a $24,000 standard deduction.The personal exemptions are eliminated.

Mortgage Interest Deduction

New mortgages would be capped at $750,000 for purposes of the home mortgage interest deduction.

State and Local Tax Deductions

State and local tax deduction will remain but will be capped at $10,000. An ouch for New York State. That $10,000 can be a combination of your property tax and either sales or income tax (whichever is larger or will get you to the cap of $10,000).Oh and you cannot prepay your 2018 state income taxes in 2017 to avoid the cap. They made it clear that if you prepay your 2018 state income taxes in 2017, you will not be able to deduct them in 2017.

Medical Expense Deductions

Medical expense deductions will remain for 2017 and 2018 and they lowered the AGI threshold to 7.5%. Beginning in 2019, the threshold will change back to the 10% threshold.

Miscellaneous Expense Deductions

Under the current rules, you are able to deduct miscellaneous expenses that exceed 2% of your AGI. That was eliminated. This includes unreimbursed business expenses and home office expenses.

A Few Quick Ones

Student Loan Interest: Still deductible

Teacher Out-of-Pocket Expenses: Still deductible

Tuition Waivers: Still not taxable

Fringe Benefits (including moving expenses): Will be taxable starting in 2018 (except for military)

Child Tax Credit: Doubled to $2,000 per child

Gain Exclusion On Sale Of Primary Residence: No Change

Obamacare Individual Mandate: Eliminated

Corporate AMT: Eliminated

Individual AMT: Remains but exemption is increased: Individuals: $70,300 Married: $109,400

Corporate Tax Rate: Drops to 21% in 2018

Federal Estate Tax: Remains but exemption limit doubles

Alimony

For divorce agreements signed after December 31, 2018, alimony will no longer be deducible. This only applies to divorce agreements executed or modified after December 31, 2018.

529 Plans

Under current tax law, you do not pay taxes on the earnings for distributions from 529 accounts for qualified college expenses. The new tax reform allows 529 account owners to distribute up to $10,000 per student for public, private and religious elementary and secondary schools, as well as home school students.

Pass-Through Income For Business

This is still a little cloudy but in general under the conference bill, owners of pass-through companies and sole proprietors will be taxed at their individual tax rates less a 20% deduction for business-related income, subject to certain wage limits and exceptions. The deduction would be disallowed for businesses offering "professional services" above a threshold amount; phase-ins begin at $157,500 for individual taxpayers and $315,000 for married taxpayers filing jointly.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: Your Company May Voluntarily Terminate Your Retirement Plan

Make no mistake, your company retirement plan is at risk if the proposed tax reform is passed. But wait…..didn’t Trump tweet on October 23, 2017 that “there will be NO change to your 401(k)”? He did tweet that, however, while the tax reform might not directly alter the contribution limits to employer sponsored retirement plans, the new tax rates

Make no mistake, your company retirement plan is at risk if the proposed tax reform is passed. But wait…..didn’t Trump tweet on October 23, 2017 that “there will be NO change to your 401(k)”? He did tweet that, however, while the tax reform might not directly alter the contribution limits to employer sponsored retirement plans, the new tax rates will produce a “disincentive” for companies to sponsor and make employer contributions to their plans.

What Are Pre-Tax Contributions Worth?

Remember, the main incentive of making contributions to employer sponsored retirement plans is moving income that would have been taxed now at a higher tax rate into the retirement years, when for most individuals, their income will be lower and that income will be taxed at a lower rate. If you have a business owner or executive that is paying 45% in taxes on the upper end of the income, there is a large incentive for that business owner to sponsor a retirement plan. They can take that income off of the table now and then realize that income in retirement at a lower rate.

This situation also benefits the employees of these companies. Due to non-discrimination rules, if the owner or executives are receiving contributions from the company to their retirement accounts, the company is required to make employer contributions to the rest of the employees to pass testing. This is why safe harbor plans have become so popular in the 401(k) market.

But what happens if the tax reform is passed and the business owners tax rate drops from 45% to 25%? You would have to make the case that when the business owner retires 5+ years from now that their tax rate will be below 25%. That is a very difficult case to make.

An Incentive NOT To Contribute To Retirement Plans

This creates an incentive for business owners NOT to contribution to employer sponsored retirement plans. Just doing the simple math, it would make sense for the business owner to stop contributing to their company sponsored retirement plan, pay tax on the income at a lower rate, and then accumulate those assets in a taxable account. When they withdraw the money from that taxable account in retirement, they will realize most of that income as long term capital gains which are more favorable than ordinary income tax rates.

If the owner is not contributing to the plan, here are the questions they are going to ask themselves:

Why am I paying to sponsor this plan for the company if I’m not using it?

Why make an employer contribution to the plan if I don’t have to?

This does not just impact 401(k) plans. This impacts all employer sponsored retirement plans: Simple IRA’s, SEP IRA’s, Solo(k) Plans, Pension Plans, 457 Plans, etc.

Where Does That Leave Employees?

For these reasons, as soon as tax reform is passed, in a very short time period, you will most likely see companies terminate their retirement plans or at a minimum, lower or stop the employer contributions to the plan. That leaves the employees in a boat, in the middle of the ocean, without a paddle. Without a 401(k) plan, how are employees expected to save enough to retire? They would be forced to use IRA’s which have much lower contribution limits and IRA’s don’t have employer contributions.

Employees all over the United States will become the unintended victim of tax reform. While the tax reform may not specifically place limitations on 401(k) plans, I’m sure they are aware that just by lowering the corporate tax rate from 35% to 20% and allowing all pass through business income to be taxes at a flat 25% tax rate, the pre-tax contributions to retirement plans will automatically go down dramatically by creating an environment that deters high income earners from deferring income into retirement plans. This is a complete bomb in the making for the middle class.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.