Turn on Social Security at 62 and Your Minor Children Can Collect The Dependent Benefit

Not many people realize that if you are age 62 or older and have children under the age of 18, your children are eligible to receive social security payments based on your earnings history, and it’s big money. However, social security does not advertise this little know benefit, so you have to know how to apply, the rules, and tax implications.

Not many people realize that if you are age 62 or older and have children under the age of 18, your children are eligible to receive social security payments based on your earnings history, and it’s big money. However, social security does not advertise this little know benefit, so you have to know how to apply, the rules, and tax implications. In this article, I will walk you through the following:

The age limit for your children to be eligible to receive SS benefits

The amount of the payments to your kids

The family maximum benefit calculation

How the benefits are taxed to your children

How to apply for the social security dependent benefits

Pitfall: You may have to give the money back to social security…..

Eligibility Requirements for Dependent Benefits

Three requirements make your children eligible to receive social security payments based on your earnings history:

You have to be age 62 or older

You must have turned on your social security benefit payments

Your child must be unmarried and meet one of the following eligibility requirements:

Under the age of 18

Between the ages of 18 and 19 and a full-time student K – 12

Age 18 or older with a disability that began before age 22

How Much Does Your Child Receive?

If you are 62 or older, you have turned on your social security benefits, and your child meets the criteria above, your child would be eligible to receive 50% of your Full Retirement Age (FRA) Social Security Benefit EVERY YEAR, until they reach age 18. This can sometimes change a parent’s decision to turn on their social security benefit at age 62 instead of waiting until their Full Retirement Age of 67 (for individuals born in 1960 or later). But it gets better because the 50% of your FRA social security benefit is for EACH child.

For example, Jim is retired, age 62, and he has one child under age 18, Josh, who is age 12. If he turns on his social security benefit at age 62, he would receive $1,200 per month, but if he waits until his FRA of 67, he would receive $1,700 per month. Even though Jim would receive a lower social security benefit at age 62, if he turns on his benefit at age 62, Jim and his child Josh would receive the following monthly payments from social security:

Jim: $1,200 ($14,400 per year)

Josh: $850 ($10,200 per year)

Even though Jim receives a reduced SS benefit by turning on his benefit at age 62, the 50% dependent child benefit is still calculated based on Jim’s Full Retirement Age benefit of $1,700. Josh will be eligible to continue to receive monthly payments from social security until the month of his 18th birthday. That’s a lot of money that could go towards college savings, buying a car, or a down payment on their first house.

The Family Maximum Benefit Limit

If you have 10 children, I have bad news; social security imposes a “family maximum benefit limit” for all dependents eligible to collect on your earnings history. The family benefits are limited to 150% to 188% of the parent’s full retirement age benefit.

I’ll explain this via an example. Let’s assume everything is the same as in the previous example with Jim, but now Jim has four children, all under 18. Let’s also assume that Jim’s Family maximum benefit is 150% of his FRA benefit, which would equal a maximum family benefit of $2,550 per month ($1,700 x 150%). We now have the following:

Jim: $1,200

Child 1: $850

Child 2: $850

Child 3: $850

Child 4: $850

If you total up the monthly social security benefits paid to Jim and his children, it equals $4,600, which is $2,050 over the $2,550 family maximum benefit limit.

Always Use Your FRA Benefit In The Family Max Calculation

Here is another important rule to note when calculating the family maximum benefit, regardless of when your file for your social security benefits, age 62, 64, 67, or 70, you always use your Full Retirement Age benefit when calculating the Family Maximum Benefit amount. In the example above, Jim filed for social security benefits early at age 62. Instead of using Jim’s age $1,200 social security benefit to calculate the remaining amount available for his children, Jim has to use his FRA benefit of $1,700 in the formula before determining how much his children are eligible to receive.

Social security would reduce the children’s benefits by an equal amount until their total benefit is reduced to the family maximum limit.

These are the steps:

Jim Max Family Benefit = $1,700 (FRA) x 150% = $2,550

$2,550 (Family Max) - $1,700 (Jim FRA) = $850

Divide $850 by Jim’s 4 eligible children = $212.50 for each child

This results in the following social security benefits paid to Jim and his 4 children:

Jim: $1,200

Child 1: $212.50

Child 2: $212.50

Child 3: $212.50

Child 4: $212.50

A note about ex-spouses, if someone was married for more than 10 years, then got divorced, the ex-spouse may still be entitled to the 50% spousal benefit, but that does not factor into the family maximum calculation, nor is it reduced for any family maximum benefit overages.

Social Security Taxation

Social security payments received by your children are considered taxable income, but that does not necessarily mean that they will owe any tax on the amounts received. Let me explain, your child’s income has to be above a specific threshold before they owe any federal taxes on the social security benefits they receive.

You have to add up all of their regular taxable income and tax-exempt income and then add 50% of the social security benefits that they received. If your child has no other income besides the social security benefits, it’s just 50% of the social security benefits that were paid to them. If that total is below $25,000, they do not have to pay any federal tax on their social security benefit. If it’s above that amount, then a portion of the social security benefits received will be taxable at the federal level.

States have different rules when it comes to taking social security benefits. Most states do not tax social security benefits, but there are about 13 states that assess state taxes on social security benefits in one form or another, but our state New York, is thankfully not one of them.

You Can Still Claim Your Child As A Dependent On Your Tax Return

More good news, even though your child is showing income via the social security payment, you can still claim them as a dependent on your tax return as long as they continue to meet the dependent criteria.

How To Apply For Social Security Dependent Benefits

You cannot apply for your child’s dependent benefits online; you have to apply by calling the Social Security Administration at 800-772-1213 or scheduling an appointment at your local Social Security office.

Be Care of This Pitfall

There is one pitfall to the social security payment received by your child or children, it’s not a pitfall about the money received, but the issue revolves around the titling of the account that the social security benefits are deposited into when they are received on behalf of the child.

The premise behind social security providing these benefits to the minor children of retirees is that if someone retires at age 62 and still has minor children as dependents, they may need additional income to support the household expenses. Whether that is true or not does not prevent you from taking advantage of these dependent payments to your children, but it does raise the issue of the “conserved benefits” letter that many people receive once the child turns age 18.

You may receive a letter from social security once your child is 18 instructing you to return any of the social security dependent payments received on your child’s behalf and saved. So wait, if you save this money for our child to pay for college, you have to hand it back to social security, but if you spend it, you get to keep it? On the surface, the answer is “yes,” but it all depends on who is listed as the account owner that the social security payments are deposited into on behalf of your child.

If the parent is listed as an owner or joint owner of the account, you are expected to return the saved or “conserved” payment to the Social Security Administration. However, if the account that the social security payments are deposited into is owned 100% by your child, you do not have to return the saved money to social security.

Then I will get the question, “Well, what type of account can you set up for a 12-year-old that they own 100%?” Some banks will allow you to set up savings accounts in the name of a child at age 14, UTMA accounts can be set up at any age, and they are considered accounts owned 100% by the child even though a parent is listed as a custodian.

Watch out for the 529 account pitfall. For parents that want to use these Social Security payments to help subsidize college savings, they will sometimes set up a 529 account and deposit the payments into that account to take advantage of the tax benefits. Even though these 529 accounts are set up with the child listed as the beneficiary, they are often considered assets of the parents because the parent has control over the distributions from the account. However, you can set up 529 accounts as UTMA 529, which avoids this issue since the child is now technically the owner and has complete control over the assets at the age of majority.

FAFSA Considerations

Be aware that if your child is college bound and you expect to qualify for need-based financial aid, assets owned by the child count against the FAFSA calculation. The way the calculation works is that about 20% of any assets owned by the child count against the need-based financial aid that is awarded. There is no way around this issue, but it’s not the end of the world because that means 80% of the balance does not count against the FAFSA calculation and it was free money from Social Security that can be used to pay for college.

Social Security Filing Strategy

If you are age 62 or older and have minor children, it may very well make sense to file for Social Security early, even though it may permanently reduce your Social Security benefit once you factor in the Social Security payments that will be made to your children as dependents. But, you have to make sure you understand how Social Security is taxed, the Security earned income penalty, the impact of Social Security survivor benefits for your spouse, and many other factors before making this decision.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Self-Employment Income In Retirement? Use a Solo(k) Plan To Build Wealth

It’s becoming more common for retirees to take on small self-employment gigs in retirement to generate some additional income and to stay mentally active and engaged. But, it should not be overlooked that this is a tremendous wealth-building opportunity if you know the right strategies. There are many, but in this article, we will focus on the “Solo(k) strategy

Self-Employment Income In Retirement? Use a Solo(k) Plan To Build Wealth

It’s becoming more common for retirees to take on small self-employment gigs in retirement to generate some additional income and to stay mentally active and engaged. But, it should not be overlooked that this is a tremendous wealth-building opportunity if you know the right strategies. There are many, but in this article, we will focus on the “Solo(k) strategy.”

What Is A Solo(K)

A Solo(k) plan is an employer-sponsored retirement plan that is only allowed to be sponsored by owner-only entities. It works just like a 401(k) plan through a company but without the high costs or administrative hassles. The owner of the business is allowed to make both employee deferrals and employer contributions to the plan.

Solo(k) Deferral Limits

For 2023, a business owner is allowed to contribute employee deferrals up to a maximum of the LESSER of:

100% of compensation; or

$30,000 (Assuming the business owner is age 50+)

Pre-tax vs. Roth Deferrals

Like a regular 401(K) plan, the business owner can contribute those employee deferrals as all pre-tax, all Roth, or some combination of the two. Herein lies the ample wealth-building opportunity. Roth assets can be an effective wealth accumulation tool. Like Roth IRA contributions, Roth Solo(k) Employee Deferrals accumulate tax deferred, and you pay NO TAX on the earnings when you withdraw them as long as the account owner is over 59½ and the Roth account has been in place for more than five years.

Also, unlike Roth IRA contributions, there are no income limitations for making Roth Solo(k) Employee Deferrals and the contribution limits are higher. If a business owner has at least $30,000 in compensation (net profit) from the business, they could contribute the entire $30,000 all Roth to the Solo(K) plan. A Roth IRA would have limited them to the max contribution of $7,500 and they would have been excluded from making that contribution if their income was above the 2023 threshold.

A quick note, you don’t necessarily need $30,000 in net income for this strategy to work; even if you have $18,000 in net income, you can make an $18,000 Roth contribution to your Solo(K) plan for that year. The gem to this strategy is that you are beginning to build this war chest of Roth dollars, which has the following tax advantages down the road……

Tax-Free Accumulation and Withdrawal: If you can contribute $100,000 to your Roth Solo(k) employee deferral source by the time you are 70, if you achieve a 6% rate of return at 80, you have $189,000 in that account, and the $89,000 in earnings are all tax-free upon withdrawal.

No RMDs: You can roll over your Roth Solo(K) deferrals into a Roth IRA, and the beautiful thing about Roth IRAs are no required minimum distributions (RMD) at age 72. Pre-tax retirement accounts like Traditional IRAs and 401(k) accounts require you to begin taking RMDs at age 72, which are forced taxable events; by having more money in a Roth IRA, those assets continue to build.

Tax-Free To Beneficiaries: When you pass assets on to your beneficiaries, the most beneficial assets to inherit are often a Roth IRA or Roth Solo(k) account. When they changed the rules for non-spouse beneficiaries, they must deplete IRAs and retirement accounts within ten years. With pre-tax retirement accounts, this becomes problematic because they have to realize taxable income on those potentially more significant distributions. With Roth assets, not only is there no tax on the distributions, but the beneficiary can allow that Roth account to grow for another ten years after you pass and withdraw all the earnings tax and penalty-free.

Why Not Make Pre-Tax Deferrals?

It's common for these self-employed retirees to have never made a Roth contribution to retirement accounts, mainly because, during their working years, they were in high tax brackets, which warranted pre-tax contributions to lower their liability. But now that they are retired and potentially showing less income, they may already be in a lower tax bracket, so making pre-tax contributions, only to pay tax on both the contributions and the earnings later, may be less advantageous. For the reasons I mentioned above, it may be worth foregoing the tax deduction associated with pre-tax contributions and selecting the long-term benefits associated with the Roth contributions within the Solo(k) Plan.

Now there are situations where one spouse retires and has a small amount of self-employment income while the other spouse is still employed. In those situations, if they file a joint tax return, their overall income limit may still be high, which could warrant making pre-tax contributions to the Solo(k) plan instead of Roth contributions. The beauty of these Solo(k) plans is that it’s entirely up to the business owner what source they want to contribute to from year to year. For example, this year, they could contribute 100% pre-tax, and then the following year, they could contribute 100% Roth.

Solo(k) versus SEP IRA

Because this question comes up frequently, let's do a quick walkthrough of the difference between a Solo(k) and a SEP IRA. A SEP IRA is also a popular type of retirement plan for self-employed individuals; however, SEP IRAs do not allow Roth contributions, and SEP IRAs limit contributions to 20% of the business owner’s net earned income. Solo(K) plans have a Roth contribution source, and the contributions are broken into two components, an employee deferral and an employer profit sharing.

As we looked at earlier, the employee deferral portion can be 100% of compensation up to the Solo(K) deferral limit of the year, but in addition to that amount, the business owner can also contribute 20% of their net earned income in the form of a profit sharing contribution.

When comparing the two, in most cases, the Solo(K) plan allows business owners to make larger contributions in a given year and opens up the Roth source.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Grandparent Owned 529 Accounts Just Got Better

A 529 account owned by a grandparent is often considered one of the most effective ways to save for college for a grandchild. But in 2023, the rules are changing………

Grandparent Owned 529 Accounts Just Got Better

A 529 account owned by a grandparent is often considered one of the most effective ways to save for college for a student. Mainly because 529 accounts owned by the grandparents are invisible to the college financial aid calculation (FAFSA) when determining the financial aid package that will be awarded to a student. But there is a little-known pitfall about distributions from grandparent owned 529 accounts and the rules are changing in 2023. In this article, we will review:

Advantages of grandparent owned 529 accounts

The FAFSA pitfall of distributions from grandparent owned 529 accounts

The FAFSA two-year lookback period

The change to the 529 rules starting in 2023

Tax deductions for contributions to 529 accounts

What if your grandchild does not go to college?

Paying K – 12 expenses with a 529 account

Pitfall of Grandparent Owned 529 Accounts

Historically, there has been a major issue when grandparents begin distributing money out of these 529 accounts to pay college expenses for their grandchildren which can hurt their financial aid eligibility. While these accounts are invisible to the FAFSA calculation as an asset, in the year that the distribution takes place from a grandparent owned 529 account, those distributions now count as “income of the student” in the year that the distribution takes place. Income of the student counts heavily against the need-based financial aid award. Currently, any income of the student above the $7,040 threshold counts 50% against the financial aid award.

For example, if a grandparent distributes $30,000 from the 529 account to pay college expenses for the grandchild, in that determination year, assuming the child has no other income, that distribution could reduce the financial aid award two years later by $11,480.

FAFSA Two-Year Lookback

FAFSA has a two-year lookback for purposes of determining income in the EFC calculation (expected family contribution), so the family doesn’t realize the misstep until two years later. For example, if the distribution takes place in the fall of the student’s freshman year, the financial aid package would not be reduced until the fall of their junior year.

Since we are aware of this income two-year lookback rule, the workaround has been to advise grandparents not to distribute money from the 529 accounts until the spring of their sophomore year. If the child graduates in four years by the time they are submitting the FAFSA application for their senior year, that determination year that 529 distribution took place is no longer in play.

Quick Note: All of this only matters if the student qualifies for need-based financial aid. If the student, through their parent’s FAFSA application, does not qualify for any need-based financial aid, then the impact of these distributions from the grandparent owned 529 accounts is irrelevant because they were not receiving any financial aid anyways.

New Rules Starting in 2023

But the rules are changing starting in 2023 to make these grandparent owned 529 accounts even more advantageous. Under the new rules, distribution from grandparent owned 529 account will no longer count as income of the student. These 529 accounts owned by the grandparents are now completely invisible to the FAFSA calculation for both assets and income, which makes them even more valuable.

Tax Deduction For 529 Contributions

There can also be tax benefits for grandparents contributing to 529 accounts for their grandkids. Certain states allow state income tax deductions for contributions up to a certain thresholds. In New York State, there is a $5,000 state tax deduction for single filers and a $10,000 deduction for joint filers each tax year. The amounts vary from state to state and some states have no deduction, so you have to do your homework.

What If The Grandchild Does Not Go To College?

What happens if you fund this 529 account for your grandchild but then they decide not to go to college? There are a few options here. The grandparent can change the beneficiary of the account to another grandchild or family member. The second option, you can just take a distribution of the account balance. If the balance is distributed but it’s not used for college expenses, the contribution amounts are returned tax and penalty-free but the earnings portion of the account is subject to ordinary income taxes and a 10% penalty since it wasn’t used for qualified college expenses.

K - 12 Qualified Expenses

The federal government made changes to the tax rules in 2017 which also allow up to $10,000 per year to be distributed from 529 accounts for K - 12 expenses. If you have grandchildren that are attending a private k -12 school, this is another way for grandparents to potentially capture a tax deduction, and help pay those expenses.

However, and this is very important, while the federal government recognizes the K – 12 $10,000 per year as a qualified distribution, the states which sponsor these 529 plans may not adhere to those same rules. In fact, in New York State, not only does New York not recognize K – 12 expenses as “qualified expenses” for purposes of distributions from a 529 account, but these nonqualified withdrawals also require a recapture of any New York State tax benefits that have accrued on the contributions. Double ouch!! These rules vary state by state so you have to do your homework before paying K – 12 expenses out of a 529 account.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Potential investors of 529 plans may get more favorable tax benefits from 529 plans sponsored by their own state. Consult your tax professional for how 529 tax treatments and account fees would apply to your particular situation. To determine which college saving option is right for you, please consult your tax and accounting advisors. Neither APFS nor its affiliates or financial professionals provide tax, legal or accounting advice. Please carefully consider investment objectives, risks, charges, and expenses before investing. For this and other information about municipal fund securities, please obtain an offering statement and read it carefully before you invest. Investments in 529 college savings plans are neither FDIC insured nor guaranteed and may lose value.

The New PTET Tax Deduction for Business Owners

The PTET (pass-through entity tax) is a deduction that allows business owners to get around the $10,000 SALT cap that was put in place back in 2017. The PTET allows the business entity to pay the state tax liability on behalf of the business owner and then take a deduction for that expense.

Above is our video about the PTET (pass-through entity tax) deduction which allows business owners to get around the $10,000 SALT cap that was put in place back in 2017. The PTET allows the business entity to pay the state tax liability on behalf of the business owner and then take a deduction for that expense. This special tax deduction can save a business owner thousands of dollars in taxes. Currently, 31 states, including New York, have some form of PTET program. In this video, Dave Wojeski & Michael Ruger will cover:

How the PTET deduction works?

Which type of entities are eligible for the PTET deduction

Deadlines for electing into the PTET program

How the estimated tax payments are calculated and the deadlines for remitting them

Changes to the PTET S-corp rules in 2022

The new NYC PTET program available in 2023

The challenges faced by companies that have multiple owners that are residents of different states

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Additional Disclosure: Wojeski & Company, American Portfolios and Greenbush Financial Group LLC are unaffiliated entities. Neither APFS nor its Representatives provide tax, legal or accounting advice. Please consult your own tax, legal or accounting professional before making any decisions.

Self-employed Individuals Are Allowed To Take A Tax Deduction For Their Medicare Premiums

If you are age 65 or older and self-employed, I have great news, you may be able to take a tax deduction for your Medicare Part A, B, C, and D premiums as well as the premiums that you pay for your Medicare Advantage or Medicare Supplemental coverage.

Self-employed Individuals Are Allowed To Take A Tax Deduction For Their Medicare Premiums

If you are age 65 or older and self-employed, I have great news, you may be able to take a tax deduction for your Medicare Part A, B, C, and D premiums as well as the premiums that you pay for your Medicare Advantage or Medicare Supplemental coverage. This is a huge tax benefit for business owners age 65 and older because most individuals without businesses are not able to deduct their Medicare premiums, so they have to be paid with after-tax dollars.

Individuals Without Businesses

If you do not own a business, you are age 65 or older, and on Medicare, you are only allowed to deduct “medical expenses” that exceed 7.5% of your adjusted gross income (AGI) for that tax year. Medical expenses can include Medicare premiums, deductibles, copays, coinsurance, and other noncovered services that you have to pay out of pocket. For example, if your AGI is $80,000, your total medical expenses would have to be over $6,000 ($80,000 x 7.5%) for the year before you would be eligible to start taking a tax deduction for those expenses.

But it gets worse, medical expenses are an itemized deduction which means you must forgo the standard deduction to claim a tax deduction for those expenses. For 2022, the standard deduction is $12,950 for single filers and $25,900 for married filing joint. Let’s look at another example, you are a married filer, $70,000 in AGI, and your Medicare premiums plus other medical expenses total $12,000 for the year since the 7.5% threshold is $5,250 ($70,000 x 7.5%), you would be eligible to deduct the additional $6,750 ($12,000 - $5,250) in medical expenses if you itemize. However, you would need another $13,600 in tax deductions just to get you up to the standard deduction limit of $25,900 before it would even make sense to itemize.

Self-Employed Medicare Tax Deduction

Self-employed individuals do not have that 7.5% of AGI threshold, they are able to deduct the Medicare premiums against the income generated by the business. A special note in that sentence, “against the income generated by the business”, in other words, the business has to generate a profit in order to take a deduction for the Medicare premiums, so you can’t just create a business, that has no income, for the sole purpose of taking a tax deduction for your Medicare premiums. Also, the IRS does not allow you to use the Medicare expenses to generate a loss.

For business owners, it gets even better, not only can the business owner deduct the Medicare premiums for themselves but they can also deduct the Medicare premiums for their spouse. The standard Medicare Part B premium for 2022 is $170.10 per month for EACH spouse, now let’s assume that they both also have a Medigap policy that costs $200 per month EACH, here’s how the annual deduction would work:

Business Owner Medicare Part B: $2,040 ($170 x 12 months)

Business Owner Medigap Policy: $2,400

Spouse Medicare Part B: $2,040

Spouse Medigap Policy: $2,400

Total Premiums: $8,880

If the business produces $10,000 in net profit for the year, they would be able to deduct the $8,880 against the business income, which allows the business owner to pay the Medicare premiums with pre-tax dollars. No 7.5% AGI threshold to hurdle. The full amount is deductible from dollar one and the business owner could still elect the standard deduction on their personal tax return.

The Tax Deduction Is Limited Only To Medicare Premiums

When we compare the “medical expense” deduction for individual taxpayers that carries the 7.5% AGI threshold and the deduction that business owners can take for Medicare premiums, it’s important to understand that for business owners the deduction only applies to Medicare premiums NOT their total “medical expenses” for the year which include co-pays, coinsurance, and other out of pocket costs. If a business owner has large medical expenses outside of the Medicare premiums that they deducted against the business income, they would still be eligible to itemize on their personal tax return, but the 7.5% AGI threshold for those deductions comes back into play.

What Type of Self-Employed Entities Qualify?

To be eligible to deduct the Medicare premiums as an expense against your business income your business could be set up as a sole proprietor, independent contractor, partnership, LLC, or an S-corp shareholder with at least 2% of the common stock.

The Medicare Premium Deduction Lowers Your AGI

The tax deduction for Medicare Premiums for self-employed individuals is considered an “above the line” deduction, which lowers their AGI, an added benefit that could make that taxpayer eligible for other tax credits and deductions that are income based. If your company is an S-corp, the S-corp can either pay your Medicare Premiums on your behalf as a business expense or the S-corp can reimburse you for the premiums that you paid, report those amounts on your W2, and you can then deduct it on Schedule 1 of your 1040.

Employer-Subsidized Health Plan Limitation

One limitation to be aware of, is if either the business owner or their spouse is eligible to enroll in an employer-subsidized health plan through their employer, you are no longer allowed to deduct the Medicare Premiums against your business income. For example, if you and your spouse are both age 66, and you are self-employed, but your spouse has a W2 job that offers health benefits to cover both them and their spouse, you would not be eligible to deduct the Medicare Premiums against your business income. This is true even if you voluntarily decline the coverage. If you or your spouse is eligible to participate, you cannot take a deduction for their Medicare premiums.

I receive the question, “What if they are only employed for part of the year with health coverage available?” For the month that they were eligible for employer-subsidized health plan, a deduction would not be able to be taken during those months for the Medicare premiums.

On the flip side, if the health plan through their employer is considered “credible coverage” by Medicare, you may not have to worry about Medicare premiums anyways.

Multiple Businesses

If you have multiple businesses, you will have to select a single business to be the “sponsor” of your health plan for the purpose of deducting your Medicare premiums. It’s usually wise to select the business that produces a consistent net profit because net profits are required to deduct all or a portion of the Medicare premium expense.

Forms for Tax Reporting

You will have to keep accurate records to claim this deduction. If you collect Social Security, the Medicare premiums are deducted directly from the social security benefit, but they issue you a SSA-1099 Form at the end of the year which summarized the Medicare Premiums that you paid for Part A and Part B.

If you have a Medigap Policy (Supplemental) with a Part D plan or a Medicare Advantage Plan, you normally make premium payments directly to the insurance company that you have selected to sponsor your plan. You will have to keep records of those premium payments.

No Deduction For Self-Employment Taxes

As a self-employed individual, the Medicare premiums are eligible for a federal, state, and local tax deduction but they do not impact your self-employment taxes which are the taxes that you pay to fund Medicare and Social Security.

Amending Your Tax Returns

If you have been self-employed for a few years, paying Medicare premiums, and are just finding out now about this tax deduction, the IRS allows you to amend your tax returns up to three years from the filing date. But again, the business had to produce a profit during those tax years to be eligible to take the deduction for those Medicare premiums.

DISCLOSURE: This information is for educational purposes only. For tax advice, please consult a tax professional.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

401(K) Cash Distributions: Understanding The Taxes & Penalties

When an employee unexpectedly loses their job and needs access to cash to continue to pay their bills, it’s not uncommon for them to elect a cash distribution from their 401(K) account. Still, they may regret that decision when the tax bill shows up the following year and then they owe thousands of dollars to the IRS in taxes and penalties that they don’t have.

When an employee unexpectedly loses their job and needs access to cash to continue to pay their bills, it’s not uncommon for them to elect a cash distribution from their 401(K) account. Still, they may regret that decision when the tax bill shows up the following year and then they owe thousands of dollars to the IRS in taxes and penalties that they don’t have. But I get it; if it’s a choice between working a few more years or losing your house because you don’t have the money to make the mortgage payments, taking a cash distribution from your 401(k) seems like a necessary evil. If you go this route, I want you to be aware of a few strategies that may help you lessen the tax burden and avoid tax surprises after the 401(k) distribution is processed. In this article, I will cover:

How much tax do you pay on a 401(K) withdrawal?

The 10% early withdrawal penalty

The 401(k) 20% mandatory fed tax withholding

When do you remit the taxes and penalties to the IRS?

The 401(k) loan default issue

Strategies to help reduce the tax liability

Pre-tax vs. Roth sources

Taxes on 401(k) Withdrawals

When your employment terminates with a company, that triggers a “distributable event,” which gives you access to your 401(k) account with the company. You typically have the option to:

Leave your balance in the current 401(k) plan (if the balance is over $5,000)

Take a cash distribution

Rollover the balance to an IRA or another 401(k) plan

Some combination of options 1, 2, and 3

We are going to assume you need the cash and plan to take a total cash distribution from your 401(k) account. When you take cash distributions from a 401(k), the amount distributed is subject to:

Federal income tax

State income tax

10% early withdrawal penalty

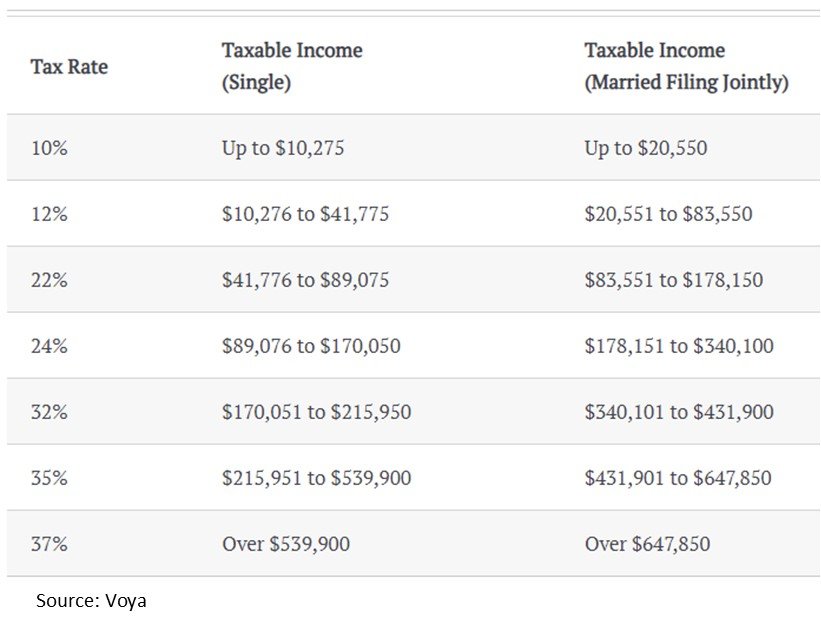

I’m going to assume your 401(k) account consists of 100% of pre-tax sources; if you have Roth contributions, I will cover that later on. When you take distributions from a 401(k) account, the amount distributed is subject to ordinary income tax rates, the same tax rates you pay on your regular wages. The most common question I get is, “how much tax am I going to owe on the 401(K) withdrawal?”. The answer is that it varies from person to person because it depends on your personal income level for the year. Here are the federal income tax brackets for 2022:

Using the chart above, if you are married and file a joint tax return, and your regular AGI (adjusted gross income) before factoring in the 401(K) distribution is $150,000, if you take a $20,000 distribution from your 401(k) account, it would be subject to a Fed tax rate of 24%, resulting in a Fed tax liability of $4,800.

If instead, you are a single filer that makes $170,000 in AGI and you take a $20,000 distribution from your 401(k) account, it would be subject to a 32% fed tax rate resulting in a federal tax liability of $6,400.

20% Mandatory Fed Tax Withholding Requirement

When you take a cash distribution directly from a 401(k) account, they are required by law to withhold 20% of the cash distribution amount for federal income tax. This is not a penalty; it’s federal tax withholding that will be applied toward your total federal tax liability in the year that the 401(k) distribution was processed. For example, if you take a $100,000 cash distribution from your 401(K) when they process the distribution, they will automatically withhold $20,000 (20%) for fed taxes and then send you a check or ACH for the remaining $80,000. Again, this 20% federal tax withholding is not optional; it’s mandatory.

Here's where people get into trouble. People make the mistake of thinking that since taxes were already withheld from the 401(k) distribution, they will not owe more. That is often an incorrect assumption. In our earlier example, the single filer was in a 32% tax bracket. Yes, they withheld 20% in federal income tax when the distribution was processed, but that tax filer would still owe another 12% in federal taxes when they file their taxes since their federal tax bracket is higher than 20%. If that single(k) tax filer took a $100,000 401(k) distribution, they could own an additional $12,000+ when they file their taxes.

State Income Taxes

If you live in a state with a state income tax, you should also plan to pay state tax on the amount distributed from your 401(k) account. Some states have mandatory state tax withholding similar to the required 20% federal tax withholding, but most do not. If you live in New York, you take a $100,000 401(k) distribution, and you are in the 6% NYS tax bracket, you would need to have a plan to pay the $6,000 NYS tax liability when you file your taxes.

10% Early Withdrawal Penalty

If you request a cash distribution from a 401(k) account before reaching a certain age, in addition to paying tax on the distribution, the IRS also hits you with a 10% early withdrawal penalty on the gross distribution amount.

Under the age of 55: If you are under the age of 55, in the year that you terminate employment, the 10% early withdrawal penalty will apply.

Between Ages 55 and 59½: If you are between the ages of 55 and 59½ when you terminate employment and take a cash distribution from your current employer’s 401(k) plan, the 10% early withdrawal penalty is waived. This is an exception to the 59½ rule that only applies to qualified retirement accounts like 401(k)s, 403(b)s, etc. But the distribution must come from the employer’s plan that you just terminated employment with; it cannot be from a previous employer's 401(k) plan.

Note: If you rollover your balance to a Traditional IRA and then try to take a distribution from the IRA, you lose this exception, and the under age 59½ 10% early withdrawal penalty would apply. The distribution has to come directly from the 401(k) account.

Age 59½ and older: Once you reach 59½, you can take cash distributions from your 401(k) account, and the 10% penalty no longer applies.

When Do You Pay The 10% Early Withdrawal Penalty?

If you are subject to the 10% early withdrawal penalty, it is assessed when you file your taxes; they do not withhold it from the distribution amount, so you must be prepared to pay it come tax time. The taxes and penalties add up quickly; let’s say you take a $50,000 distribution from your 401(k), age 45, in a 24% Fed tax bracket and a 6% state tax bracket. Here is the total tax and penalty hit:

Gross 401K Distribution: $50,000

Fed Tax Withholding (24%) ($12,000)

State Tax Withholding (6%) ($3,000)

10% Penalty ($5,000)

Net Amount: $30,000

In the example above, you lost 40% to taxes and penalties. Also, remember that when the 401(k) platform processed the distribution, they probably only withheld the mandatory 20% for Fed taxes ($10,000), meaning another $10,000 would be due when you filed your taxes.

Strategies To Reduce The Tax Liability

There are a few strategies that you may be able to utilize to reduce the taxes and penalties assessed on your 401(k) cash distribution.

The first strategy involves splitting the distribution between two tax years. If it’s toward the end of the year and you have the option of taking a partial cash distribution in December and then the rest in January, that would split the income tax liability into two separate tax years, which could reduce the overall tax liability compared to realizing the total distribution amount in a single tax year.

Note: Some 401(k) plans only allow “lump sum distributions,” which means you can’t request partial withdrawals; it’s an all or none decision. In these cases, you may have to either request a partial withdrawal and partial rollover to an IRA, or you may have to rollover 100% of the account balance to an IRA and then request the distributions from there.

The second strategy is called “only take what you need.” If your 401(k) balance is $50,000, and you only need a $20,000 cash distribution, it may make sense to rollover the entire balance to an IRA, which is a non-taxable event, and then withdraw the $20,000 from your IRA account. The same taxes and penalties apply to the IRA distribution that applies to the 401(k) distribution (except the age 55 rule), but it allows the $30,000 that stays in the IRA to avoid taxes and penalties.

Strategy three strategy involved avoiding the mandatory 20% federal tax withholding in the same tax year as the distribution. Remember, the 401(K) distribution is subject to the 20% mandatory federal tax withholding. Even though they're sending that money directly to the federal government on your behalf, it actually counts as taxable income. For example, if you request a $100,000 distribution from your 401(k), they withhold $20,000 (20%) for fed taxes and send you a check for $80,000, even though you only received $80,000, the total $100,000 counts as taxable income.

IRA distributions do not have the 20% mandatory federal tax withholding, so you could rollover 100% of your 401(k) balance to your IRA, take the $80,000 out of your IRA this year, which will be subject to taxes and penalties, and then in January next year, process a second $20,000 distribution from your IRA which is the equivalent of the 20% fed tax withholding. However, by doing it this way, you pushed $20,000 of the income into the following tax year, which may be taxed at a lower rate, and you have more time to pay the taxes on the $20,000 because the tax would not be due until the tax filing deadline for the following year.

Building on this example, if your federal tax liability is going to be below 20%, by taking the distribution from the 401K you are subject to the 20% mandatory fed tax withholding, so you are essentially over withholding what you need to satisfy the tax liability which creates more taxable income for you. By rolling over the money to an IRA, you can determine the exact amount of your tax liability in the spring, and distribute just that amount for your IRA to pay the tax bill.

Loan Default

If you took a 401K loan and still have an outstanding loan balance in the plan, requesting any type of distribution or rollover typically triggers a loan default which means the outstanding loan balance becomes fully taxable to you even though no additional money is sent to you. For example, if You have an $80,000 balance in the 401K plan, but you took a loan two years ago and still have a $20,000 outstanding loan balance within the plan, if you terminate employment and request a cash distribution, the total amount subject to taxes and penalties is $100,000, not $80,000 because you have to take the outstanding loan balance into account. This is also true when they assess the 20% mandatory fed tax withholding. The mandatory withholding is based on the balance plus the outstanding loan balance. I mention this because some people are surprised when their check is for less than expected due to the mandatory 20% federal tax withholding on the outstanding loan balance.

Roth 401(k) Early Withdrawal Penalty

401(k) plans commonly allow Roth deferrals which are after-tax contributions to the plan. If you request a cash distribution from a Roth 401(k) source, the portion of the account balance that you actually contributed to the plan is returned to you tax and penalty-free; however, the earnings that have accumulated on that Roth source you have to pay tax and potentially the 10% early withdrawal penalty on. This is different from pre-tax sources which the total amount is subject to taxes and penalties.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

$7,500 EV Tax Credit: Use It or Lose It

Claiming the $7,500 tax credit for buying an EV (electric vehicle) or hybrid vehicle may not be as easy as you think. First, it’s a “use it or lose it credit” meaning if you do not have a federal tax liability of at least $7,500 in the year that you buy your electric vehicle, you cannot claim the full $7,500 credit and it does not carryforward to future tax years.

Claiming the $7,500 tax credit for buying an EV (electric vehicle) or hybrid vehicle may not be as easy as you think. First, it’s a “use it or lose it credit” meaning if you do not have a federal tax liability of at least $7,500 in the year that you buy your electric vehicle, you cannot claim the full $7,500 credit and it does not carryforward to future tax years. Normally, most individuals and business owners adopt tax strategies to reduce their tax liability but this use it or lose it EV tax credit could cause some taxpayers to do the opposite, to intentionally create a larger federal tax liability, if they think their federal tax liability will be below the $7,500 credit threshold.

There are several other factors that you also have to consider to qualify for this EV tax credit which include:

New income limitations for claiming the credit

Limits on the purchase price of the car

The type of EV / hybrid vehicles that qualify for the credit

Inflation Reduction Act (August 2022) changes to the EV tax credit rules

Buying an EV in 2022 vs 2023+

Tax documents that you need to file with your tax return

State EV tax credits that may be available

Inflation Reduction Act Changes To EV Tax Credits

On August 16, 2022, the Inflation Reduction Act was signed into law, which changed the $7,500 EV Tax Credits that were previously available. The new law expanded and limited the EV tax credits depending on your income level, what type of EV car you want, and when you plan to buy the car. Most of the changes do not take place until 2023 and 2024, so depending on your financial situation it may be better to purchase an EV in 2022 or it may be beneficial to wait until 2023+.

$7,500 EV Tax Credit

If you purchase an electronic vehicle or hybrid that qualifies for the EV tax credit, you may be eligible to claim a tax credit of up to $7,500 in the tax year that you purchased the car. This is the government’s way of incentivizing consumers to buy electric vehicles. The Inflation Reduction Act also opened up a new $4,000 tax credit for used EVs.

New Income Limits for EV Tax Credits

Starting in 2023, your income (modified AGI) will need to be below the following thresholds to qualify for the federal EV tax credits on a new EV or hybrid:

Single Filers: $150,000

Married Filing Joint: $300,000

Single Head of Household: $225,000

There are lower income thresholds to be eligible for the used EV tax credit which is as follows:

Single Filers: $75,000

Married Filing Joint: $150,000

Single Head of Household: $112,500

Before the passage of the Income Reduction Act, there were no income limitations to claim the $7,500 Tax Credit. Taxpayers with incomes level above the new thresholds may have an incentive to purchase their new EV before December 31, 2022, before the income limitations take effect in 2023.

Restriction on EV Cars That Qualify

Not all EV or hybrid vehicles will qualify for the EV tax credit. The passage of the Inflation Reduction Act made several changes in this category.

Removal of the Manufacturers Cap

On the positive side, Tesla and GM cars will once again be eligible for the EV tax credit. Under the old EV tax credit rules, once a car manufacturer sold over 200,000 EVs, vehicles made by that manufacturer were no longer eligible for the $7,500 tax credit. The new legislation that just passed eliminated those caps making Tesla, GM, and Toyota vehicles once again eligible for the credit. The removal of the cap does not take place until January 1, 2023.

Purchase Price Limit

Adding restrictions, the Inflation Reduction Act introduced a cap on the purchase price of new EVs and hybrids that qualify for the $7,500 EV tax credit. The limit on the manufacturer’s suggested retail price is as follows:

Sedans: $55,000

SUV / Trucks / Vans: $80,000

If the MSRP is above those prices, the vehicle no longer qualified for the EV tax credit.

Assembly & Battery Requirements

Another change was made to the EV tax credit under the new legislation that will most likely limit the number of vehicles that are eligible for the credit. The new law introduced a final assembly and battery component requirement. First, to be eligible for the credit, the final assembly of the vehicle needs to take place in North America. Second, the battery used to power the vehicle must be made up of key materials and consist of components that are either manufactured or assembled in North America.

Leases Do Not Qualify

If you lease a car, that does not qualify toward the EV tax credit because you technically do not own the vehicle, the manufacturer does. You have to buy the vehicle to be eligible for the $7,500 EV tax credit.

Are You Eligible For The EV Tax Credit?

Bringing everything together, starting in 2023, to determine whether or not you will be eligible for the $7,500 EV Tax Credit, you will have to make sure that:

Your income is below the EV tax credit limits

The purchase price of the vehicle is below the EV tax credit limit

The vehicles assembly and battery components meet the new requirement

Once there is more clarification around the assembly and components piece of the new legislation there will undoubtedly be a website that lists all of the vehicles that are eligible for the $7,500 tax credit that you will be able to use to determine which vehicles qualify.

Timing of The Tax Credit

Under the current EV tax credit rule, you purchase the vehicle now, but you do not receive the tax credit until you file your taxes for that calendar year. Starting in 2024, the tax credit will be allowed to occur at the point of sale which is more favorable for consumers. Logistically, it would seem that an individual would assign the credit to the car dealer, and then the car dealer would receive an advance payment from the US Department of Treasury to apply the discount or potentially allow the car buyer to use the credit toward the down payment on the vehicle.

However, car buyers will have to be careful here. Since your eligibility for the tax credit is income based, if you apply for the credit in advance, but then your income for the year is over the MAGI threshold, you may owe that money back to the IRS when you file your taxes. It will be interesting to see how this is handled since the credits are being awarded in advance.

A Use It or Lose It Tax Credit

There are going to be some challenges with the new EV tax credit rule beyond limiting the number of people that qualify and the number of cars that qualify. The primary one is that the $7,500 EV federal tax credit is not a “refundable tax credit.” A refundable tax credit means if your total federal tax liability is less than the credit, the government gives you a refund of the remaining amount, so you receive the full amount as long as you qualify. The EV tax credit is still a “non-refundable tax credit” meaning if you do not have a federal tax liability of at least $7,500 in the year that you purchase the new EV vehicle, you may lose all or a portion of the $7,500 that you thought you were going to receive.

For example, let’s say you are a single tax filer, and you make $50,000 per year. If you just take the standard deduction, with no other tax deductions, your federal tax liability may be around $4,200 in 2023. You buy a new EV in 2023, you meet the income qualifications, and the vehicle meets all of the manufacturing qualifications, so you expect to receive $7,500 when you file your taxes for 2023. However, since your federal tax liability was only $4,200 and the EV tax credit is not refundable, you would only receive a tax credit of $4,200, not the full $7,500.

No EV Tax Credit Carryforward

With some tax deductions, there is something called tax carryforward, meaning if you do not use the tax deduction in the current tax year, you can “carry it forward” to be used in future tax years to offset future income. The EV tax credit does not allow carryforward, if you can’t use all of it in the year of the EV purchase, you lose it.

Intentionally Creating Federal Tax Liability

If you are in this scenario where you purchase an EV but you expect your federal tax liability to be below the full $7,500 credit threshold, you may have to do what I call “opposite tax planning”. Normally you are trying to find ways to reduce your tax bill, but in these cases, you are trying to find ways to increase your tax liability to get the maximum refund from the government. But how do you intentionally increase your tax liability? Here are a few ideas:

Stop or reduce the contributions being made to your pre-tax retirement accounts. When you make pretax contributions to retirement accounts it reduces your tax liability. But you have to be careful here, if your company offers an employer match, you could be leaving free money on the table, so you have to conduct some analysis here. In many cases, 401(k) / 403(b) allows either pre-tax or Roth contributions. If you are making pre-tax contributions, you may be able to just switch to Roth contributions, which are after-tax contributions, and still take advantage of the employer match.

Push more income into the current tax year. If you are a small business owner, you may want to push more income into the current tax year. If you are a W2 employee, you are expecting to receive a bonus payment, and you have a good working relationship with your employer, you may be able to request that they pay the bonus to you this year as opposed to the spring of next year.

Delay tax-deductible expenses into the following tax year. Again, if you are a small business owner and have control over when you realize expenses, you could push those into the following year. For W2 employees, if you have enough tax deductions to itemize, you may want to push some of the itemized deductions into the following tax year.

Delay getting married until the following tax year. Kidding but not kidding. Nothing says I love you like a full $7,500 tax credit. Use it toward the wedding. You may not qualify under the single file income limit but maybe you would qualify under the joint filer limit.

State EV Tax Credit

The $7,500 EV tax credit is a federal tax credit but some states also have EV tax credits in addition to the federal tax credit and those credits could have different criteria to qualify. It’s worth looking into before purchasing your new or used EV.

EV Tax Credit Tax Forms

In 2022, you apply for the federal EV tax credit when you file your tax return. You will have to file Form 8936 with your tax return.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

401K Loans: Pros vs Cons

There are a number of pros and cons associated with taking a loan from your 401K plan. There are definitely situations where taking a 401(k) loan makes sense but there are also number of situations where it should be avoided.

There are a number of pros and cons associated with taking a loan from your 401K plan. There are definitely situations where taking a 401(k) loan makes sense but there are also number of situations where it should be avoided. Before taking a loan from your 401(k), you should understand:

How 401(k) loans work

How much you are allowed to borrow

Duration of the loans

What is the interest rate that is charged

How the loans are paid back to your 401(k) account

Penalties and taxes on the loan balance if you are laid off or resign

How it will impact your retirement

Sometimes Taking A 401(k) Loan Makes Sense

People are often surprised when I say “taking a 401(k) loan could be the right move”. Most people think a financial planner would advise NEVER touch your retirement accounts for any reasons. However, it really depends on what you are using the 401(k) loan for. There are a number of scenarios that I have encountered with 401(k) plan participants where taking a loan has made sense including the following:

Need capital to start a business (caution with this one)

Resolve a short-term cash crunch

Down payment on a house

Payoff high interest rate credit cards

Unexpected health expenses or financial emergency

I will go into more detail regarding each of these scenarios but let’s do a quick run through of how 401(k) loans work.

How Do 401(k) Loans Work?

First, not all 401(k) plans allow loans. Your employer has to voluntary allow plan participants to take loans against their 401(k) balance. Similar to other loans, 401(k) loans charge interest and have a structured payment schedule but there are some differences. Here is a quick breakout of how 401(k) loans work:

How Much Can You Borrow?

The maximum 401(k) loan amount that you can take is the LESSER of 50% of your vested balance or $50,000. Simple example, you have a $20,000 vested balance in the plan, you can take a 401(K) loan up to $10,000. The $50,000 limit is for plan participants that have balances over $100,000 in the plan. If you have a 401(k) balance of $500,000, you are still limited to a $50,000 loan.

Does A 401(k) Loan Charge Interest?

Yes, 401(k) loans charge interest BUT you pay the interest back to your own 401(k) account, so technically it’s an interest free loan even though there is interest built into the amortization schedule. The interest rate charged by most 401(k) platforms is the Prime Rate + 1%.

How Long Do You Have To Repay The 401(k) Loan?

For most 401(k) loans, you get to choose the loan duration between 1 and 5 years. If you are using the loan to purchase your primary residence, the loan policy may allow you to stretch the loan duration to match the duration of your mortgage but be careful with this option. If you leave the employer before you payoff the loan, it could trigger unexpected taxes and penalties which we will cover later on.

How Do You Repay The 401(k) Loan?

Loan payments are deducted from your paycheck in accordance with the loan amortization schedule and they will continue until the loan is paid in full. If you are self employed without payroll, you will have to upload payments to the 401(k) platform to avoid a loan default.

Also, most 401(K) platforms provide you with the option of paying off the loan early via a personal check or ACH.

Not A Taxable Event

Taking a 401(k) loan does not trigger a taxable event like a 401(k) distribution does. This also gives 401(k)’s a tax advantage over an IRA because IRA’s do not allow loans.

Scenarios Where Taking A 401(k) Loans Makes Sense

I’ll start off on the positive side of the coin by providing you with some real life scenarios where taking a 401(k) loan makes sense, but understand that all of the these scenarios assume that you do not have idle cash set aside that could be used to meet these expenses. Taking a 401(k) loan will rarely win over using idle cash because you lose the benefits of compounded tax deferred interest as soon as you remove the money from your account in the form of a 401(k) loan.

Payoff High Interest Rate Credit Cards

If you have credit cards that are charging you 12%+ in interest and you are only able to make the minimum payment, this may be a situation where it makes sense to take a loan from your 401(k) and payoff the credit cards. But………but…….this is only a wise decision if you are not going to run up those credit card balances again. If you are in a really bad financial situation and you may be headed for bankruptcy, it’s actually better NOT to take money out of your 401(k) because your 401(k) account is protected from your creditors.

Bridge A Short-Term Cash Crunch

If you run into a short-term cash crunch where you have a large expense but the money needed to cover the expense is delayed, a 401(k) loan may be a way to bridge the gap. A hypothetical example would be buying and selling a house simultaneously. If you need $30,000 for the down payment on your new house and you were expecting to get that money from the proceeds from the sale of the current house but the closing on your current house gets pushed back by a month, you might decide to take a $30,000 loan from your 401(k), close on the new house, and then use the proceeds from the sale of your current house to payoff the 401(k) loan.

Using a 401(k) Loan To Purchase A House

Frequently, the largest hurdle for first time homebuyers when planning to buy a house is finding the cash to satisfy the down payment. If you have been contributing to your 401(k) since you started working, it’s not uncommon that the balance in your 401(k) plan might be your largest asset. If the right opportunity comes along to buy a house, it may makes sense to take a 401(k) loan to come up with the down payment, instead of waiting the additional years that it would take to build up a down payment outside of your 401(k) account.

Caution with this option. Once you take a loan from your 401(k), your take home pay will be reduced by the amount of the 401(k) loan payments over the duration of the loan, and then you will a have new mortgage payment on top of that after you close on the new house. Doing a formal budget in advance of this decision is highly recommended.

Capital To Start A Business

We have had clients that decided to leave the corporate world and start their own business but there is usually a time gap between when they started the business and when the business actually starts making money. It is for this reason that one of the primary challenges for entrepreneurs is trying to find the capital to get the business off the ground and get cash positive as soon as possible. Instead of going to a bank for a loan or raising money from friends and family, if they had a 401(k) with their former employer, they may be able to setup a Solo(K) plan through their new company, rollover their balance into their new Solo(K) plan, take a 401(k) loan from their new Solo(k) plan, and use that capital to operate the business and pay their personal expenses.

Again, word of caution, starting a business is risky, and this strategy involves spending money that was set aside for the retirement years.

Reasons To Avoid Taking A 401(k) Loan

We have covered some Pro side examples, now let’s look at the Con side of the 401(k) loan equation.

Your Money Is Out of The Market

When you take a loan from your 401(k) account, that money is removed for your 401(k) account, and then slowly paid back over the duration of the loan. The money that was lent out is no longer earning investment return in your retirement account. Even though you are repaying that amount over time it can have a sizable impact on the balance that is in your account at retirement. How much? Let’s look at a Steve & Sarah example:

Steve & Sarah are both 30 years old

Both plan to retire age 65

Both experience an 8% annualize rate of return

Both have a 401(K) balance of $150,000

Steve takes a $50,000 loan for 5 years at age 30 but Sarah does not

Since Sarah did not take a $50,000 loan from her 401(k) account, how much more does Sarah have in her 401(k) account at age 65? Answer: approximately $102,000!!! Even though Steve was paying himself all of the loan interest, in hindsight, that was an expensive loan to take since taking out $50,000 cost him $100,000 in missed accumulation.

401(k) Loan Default Risk

If you have an outstanding balance on a 401(k) loan and the loan “defaults”, it becomes a taxable event subject to both taxes and if you are under the age of 59½, a 10% early withdrawal penalty. Here are the most common situations that lead to a 401(k) loan defaults:

Your Employment Ends: If you have an outstanding 401(K) loan and you are laid off, fired, or you voluntarily resign, it could cause your loan to default if payments are not made to keep the loan current. Remember, when you were employed, the loan payments were being made via payroll deduction, now there are no paychecks coming from that employer, so no loan payment are being remitted toward your loan. Some 401(k) platforms may allow you to keep making loan payments after your employment ends but others may not past a specified date. Also, if you request a distribution or rollover from the plan after your have terminated employment, that will frequently automatically trigger a loan default if there is an outstanding balance on the loan at that time.

Your Employer Terminates The 401(k) Plan: If your employer decides to terminate their 401(k) plan and you have an outstanding loan balance, the plan sponsor may require you to repay the full amount otherwise the loan will default when your balance is forced out of the plan in conjunction with the plan termination. There is one IRS relief option in the instance of a plan termination that buys the plan participants more time. If you rollover your 401(k) balance to an IRA, you have until the due date of your tax return in the year of the rollover to deposit the amount of the outstanding loan to your IRA account. If you do that, it will be considered a rollover, and you will avoid the taxes and penalties of the default but you will need to come up with the cash needed to make the rollover deposit to your IRA.

Loan Payments Are Not Started In Error: If loan payments are not made within the safe harbor time frame set forth by the DOL rules, the loan could default, and the outstanding balance would be subject to taxes and penalties. A special note to employees on this one, if you take a 401(k) loan, make sure you begin to see deductions in your paycheck for the 401(k) loan payments, and you can see the loan payments being made to your account online. Every now and then things fall through the cracks, the loan is issued, the loan deductions are never entered into payroll, the employee doesn’t say anything because they enjoy not having the loan payments deducted from their pay, but the employee could be on the hook for the taxes and penalties associated with the loan default if payments are not being applied. It’s a bad day when an employee finds out they have to pay taxes and penalties on their full outstanding loan balance.

Double Taxation Issue

You will hear 401(k) advisors warn employees about the “double taxation” issue associated with 401(k) loans. For employees that have pre-tax dollars within their 401(k) plans, when you take a loan, it is not a taxable event, but the 401(k) loan payments are made with AFTER TAX dollars, so as you make those loan payments you are essentially paying taxes on the full amount of the loan over time, then once the money is back in your 401(k) account, it goes back into that pre-tax source, which means when you retire and take distributions, you have to pay tax on that money again. Thus, the double taxation issue, taxed once when you repay the loan, and then taxed again when you distribute the money in retirement.

This double taxation issue should be a deterrent from taking a 401(k) loan if you have access to cash elsewhere, but if a 401(k) loan is your only access to cash, and the reason for taking the loan is justified financially, it may be worth the double taxation of those 401(k) dollars.

I’ll illustrate this in an example. Let’s say you have credit card debt of $15,000 with a 16% interest rate and you are making minimum payments. That means you are paying the credit card company $2,400 per year in interest and that will probably continue with only minimum payments for a number of years. After 5 or 6 years you may have paid the credit card company $10,000+ in interest on that $15,000 credit card balance.

Instead, you take a 401(k) loan for $15,000, payoff your credit cards, and then pay back the loan over the 5-year period, you will essentially have paid tax on the $15,000 as you make the loan payments back to the plan BUT if you are in a 25% tax bracket, the tax bill will only be $3,755 spread over 5 years versus paying $2,000 - $2,500 in interest to the credit card company EVERY YEAR. Yes, you are going to pay tax on that $15,000 again when you retire but that was true even if you never took the loan.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Avoid Taking Auto Loans For More Than 5 Years – The Negative Equity Wave

There is a negative equity problem building within the U.S. auto industry. Negative equity is when you go to trade in your car for a new one but the outstanding balance on your car loan is GREATER than the value of your car. You have the option to either write a check for the remaining balance on the loan or “roll” the negative equity into your new car loan. More and more consumers are getting caught in this negative equity trap.

There is a negative equity problem building within the U.S. auto industry. Negative equity is when you go to trade in your car for a new one but the outstanding balance on your car loan is GREATER than the value of your car. You have the option to either write a check for the remaining balance on the loan or “roll” the negative equity into your new car loan. More and more consumers are getting caught in this negative equity trap. Below is a chart of the negative equity trend over the past 10 years.

In 2010, 22% of new car buyers with trade-ins had negative equity when they went to go purchase a new car. In 2020, that number doubled to 44% (source Edmunds.com). The dollar amount of the negative equity also grew from an average of $3,746 in 2010 to $5,571 in 2020.

Your Car Is A Depreciating Asset

The first factor that is contributing to this trend is the simple fact that a car is a depreciating asset, meaning, it decreases in value over time. Since most people take a loan to buy a car, if the value of your car drops at a faster pace than the loan amount, when you go to trade in your car, you may find out that your car has a trade-in value of $5,000 but you still owe the bank $8,000 for the outstanding balance on your car loan. In these cases, you either have to come out of pocket for the $3,000 to payoff the car loan or some borrowers can roll the $3,000 into their new car loan which right out of gates put them in the same situation over the life of the next car.

Compare this to a mortgage on a house. A house, historically, appreciates in value over time, so you are paying down the loan, while at the same time, your house is increasing in value a little each year. The gap between the value of the asset and what you owe on the loan is called “wealth”. You are building wealth in that asset over time versus the downward spiral horse race between the value of your car and the amount due on the loan.

How Long Should You Take A Car Loan For?

When I’m consulting with younger professionals, I often advise them to stick to a 5-year car loan and not be tempted into a 6 or 7 year loan. The longer you stretch out the payments, the more “affordable” your car payment will be, but you also increase the risk of ending up in a negative equity situation when you go to turn in your car for a new one. In my opinion, one of the greatest contributors to this negative equity issue is the rise in popularity of 6 and 7 year car loan. Can’t afford the car payment on the car you want over a 5 year loan, no worries, just stretch out the term to 6 or 7 years so you can afford the monthly payment.

Let’s say the car you want to buy costs $40,000 and the interest rate on the auto loan is 3%. Here is the monthly loan payment on a 5 year loan versus a 7 year loan:

5 Year Loan Monthly Payment: $718.75

7 Year Loan Monthly Payment: $528.53

A good size difference in the payment but what happens if you decide to trade in your car anytime within the next 7 years, it increases your chances of ending up in a negative equity situation when you go to trade in your car. Also, when comparing the total interest that you would pay on the 5-year loan versus the 7 year loan, the 7 year car loan costs you another $1,271 in interest.

But Cars Last Longer Now……

The primary objection I get to this is “well cars last longer now than they did 10 years ago so it justifies taking out a 6 or 7 year car loan versus the traditional 5 year loan.” My response? I agree, cars do last longer than what they used to 10 years ago BUT you are forgetting the following life events which can put you in a negative equity scenario:

Not everyone keeps their car for 7+ years. It’s not uncommon for car owners to get bored with the car they have and want another one 3 – 5 years later. Within the first 3 years of buying your car that is when you have the greatest negative equity because your car depreciates by a lot within those first few years, and the loan balance does not decrease by a proportionate amount because a larger portion of your payments are going toward interest at the onset of the loan.

Something breaks on the car, you are out of the warrantee period, and you worry that new problems are going to continue to surface, so you decide to buy a new car earlier than expected.

Change in the size of your family (more kids)

You move to a different climate. You need a car for snow or would prefer a convertible for down south