Market Selloff: Time To Buy, Sell, or Hold?

Over the past month, the stock market has dropped by 20%. Largely due to the economic impact of the Coronavirus. As the feeling of panic continues to increase here in the U.S., our clients are asking:

Coronavirus Selloff

Over the past month, the stock market has dropped by 20%. Largely due to the economic impact of the Coronavirus. As the feeling of panic continues to increase here in the U.S., our clients are asking:

Should we be buying stocks at these lower levels?

Is it going to get worse before it gets better?

How quickly do you think the market will bounce back after the virus is contained?

Having managed money for clients through the Tech Bubble, The Great Recession of 2008/2009, and countless market selloffs, while the circumstances are always different from crisis to crisis, there are patterns that seem to be consistent within each market selloff. Being able to identify those patterns is key in determining what the next move should be within your investment portfolio and I’m going to share those with you today.

DISCLOSURE: Throughout this article I will be using examples of industries and companies. These are not recommendations to buy or sell a particular stock. Please consult your investment professional for advice.

Is The Market Oversold?

When there is a market selloff, one of the key questions we’re trying to answer is: “Has the stock market overreacted to the risks that are being presented?” In answering this question, I think the key thing that investors forget is that a company’s stock price represents more than just one year of its earnings. When investors buy a stock it’s typically because they expect that company to grow over the course of multiple years and yield a generous return. Unexpected events like the Coronavirus without question impact those projections but it’s not uncommon for the market to overreact because it’s focused on what’s going to happen to that company’s revenue in the short term.

A good example of this are the airlines in the United States. Due to the Coronavirus companies have canceled conferences, people have canceled vacations, and sporting events have been postponed or are now being played without spectators. That is a direct hit to the airlines in the U.S. because prior to the Coronavirus they had projected a specific amount of revenue to be generated during 2020 based on all that activity. But here comes the key question. Many of the airline stocks in the U.S. have dropped by more than 50% in the past 60 days. If investors believe that the Coronavirus will eventually be contained in the coming months, are those airlines really only worth half of what they were 60 days ago?

Buffett’s Words of Wisdom

I hesitate to use Warren Buffett’s famous quote because it’s used with such frequency but it’s proven to be a valuable investment practice during times of uncertainty: “Be fearful when others are greedy and greedy when others are fearful.” While it’s easy to say, it’s very difficult to execute effectively. Buying low and selling high goes against every human emotion. It often means stepping into the most unloved names, at what would seem to be the worst time, and owning that decision. Right now those investments seem to be the airlines, hotels, cruiselines, oil companies, and other industries directly tied to travel and tourism.

This same concept also applies to the decision to “hold” or not sell your equity holdings when the market is in a panic. Even though no one likes to see their investment accounts lose value, if you were positioned appropriately prior to the start the Coronavirus pandemic, in my professional opinion, you should not be making any adjustments to your portfolio given the recent market events. If however, you were allocated too aggressively based on your own personal risk tolerance or time horizon, you have a much more difficult decision to make.

Short Term vs Long Term Risks

Market selloffs are typically triggered by two types of risks: short term risks and long term risks. Being able to identify which risk the market is facing should greatly influence the decisions that you are making within your investment portfolio.

I’m going to use the airlines again as an example. In my personal option, the Coronavirus represents a short-term risk to the airline industry. In an effort to contain the virus, conferences have been cancelled, companies have told their employees not to travel, people have canceled vacations, etc. But you have to ask yourself this question: “what’s likely to happen once the virus is contained?” Conferences may be rescheduled, business travel resumes, and people map out a new plan for their vacation. There is arguably pent up demand being created right now that the airlines will benefit from once the virus is contained.

Back when 9/11 happened, I viewed that risk as a longer term risk for the airlines because people could choose to permanently change their behavior and choose not to fly for a very long time based on that event. In the 2008 financial crisis, the banks had a long road ahead of them as they executed plans to dig out of their leveraged positions. Problems of this nature usually require more time to fix which is why these longer term risks can justify a move from stocks into bonds.

Winners and Losers

Even with short term risk diversification is key. Just because a risk is a short term risk does not necessarily mean all companies are going to survive it. There is a risk to all companies that are impacted by market events that they run out of cash before the tide turns back to the upside. If you are an investor looking to buy into airlines at these lower levels, it's typically prudent to buy multiple companies in smaller increments, as opposed to establishing a large position in a single airline. Again, just an example, if you decide to buy stock in American Airlines, Delta, Southwest, and United Airlines, the risk of buying low is one of the four may run out of money before the virus is contained and they are forced with filing bankruptcy without a bailout from the government. If you put all of your money into one airline, you are taking on a lot more risk.

Buyer’s Remorse

One of the lessons I’ve learned from buying during a market selloff is you need to keep your long-term perspective. Meaning when you purchase a stock that has dropped significantly, there are forces acting on that company that could cause it to drop by more. You have to be comfortable with that reality and you have to possess the time horizon to weather the storm in the likely case that it could get worse before it gets better.

It’s all too common that investors purchase a stock thinking that since it’s already dropped 30%+ that it can’t possibly go any lower, only to watch it drop by another 30% and then feel pressured to sell it thinking they made a mistake. I call this “buyer’s remorse”. When you play the role of an opportunistic investor, it may take months or years for the benefit to be realized. Investing for a “quick pop” is a fool’s game, especially with the Coronavirus situation. No one knows how long it’s going to take to contain the virus, how badly Q1 and Q2 revenue will be hurt for companies, or will it end up causing a recession. Making the decision to buy stock at lower levels is usually based on the investment thesis that the stock market is overreacting to a relatively short term event and those companies getting hit the hardest will recover over time.

How Much Time Will It Take For the Market To Recover?

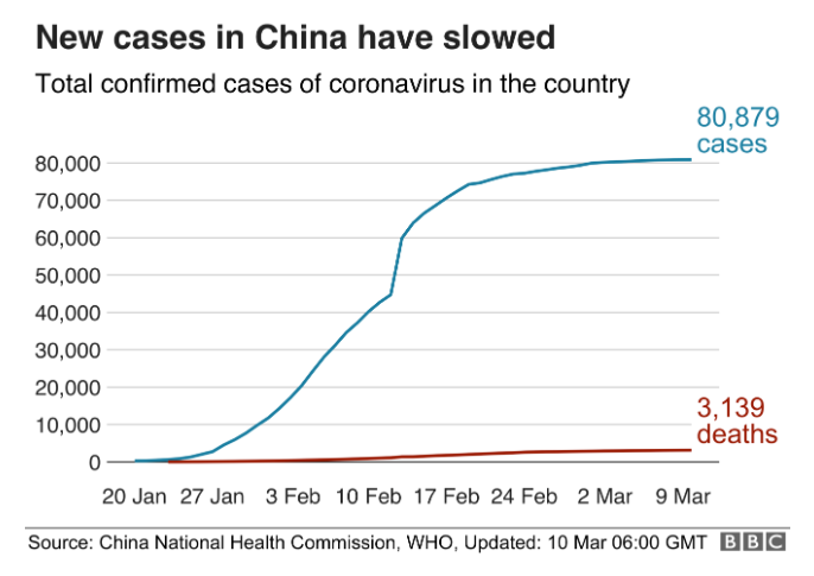

No one knows the answer to this question because we have never really been in this situation before. We have been through other epidemics in the past such as SARS, MERS, Swine Flu, and Ebola, but nothing that spread as quickly or as broadly around the globe as the Coronavirus. Since China was ground zero for the virus, the good news is we are already seeing significant progress being made at containing the virus.

As you can see via the blue line in the chart, at the beginning of February China was reporting thousands of new cases every day, but since the beginning of March the line flattens out, meaning the number new people getting infected is tapering off. If the United States follows a similar trajectory, we may see the rate of infection rise significantly in the upcoming days only to see the numbers taper off a month or two from now.

I would argue that we have an added advantage over China and Europe in that we had more time to prepare, we know more about the spread of the virus, and how to contain it. I think the lesson that we learned from Europe was you have to be aggressive in your containment efforts which is why you are seeing the extreme measures that the U.S. is taking to contain the spread of the virus. Those extreme containment efforts hurt the market more in the short term but will hopefully result in less damage to the economy over the longer term.

It’s really a race against time. The longer it takes to contain the virus, the longer it takes for people to get back to work, the longer it takes for people to feel safe traveling again, which results in more companies being put at risk of running out of capital waiting for the recovery to arrive. This is the reason why the Fed is aggressively dropping interest rates right now. Dropping interest rates does absolutely nothing to contain the virus or make people feel safe about traveling but it provides companies that are struggling due to the loss of revenue with access to low interest rate debt to bridge the gap.

A Recession Is Very Possible

A recession is defined as two consecutive quarters of negative GDP growth. With the global slowdown that has taken place in 2020, the U.S. economy may post a negative GDP number for the first quarter. Since it takes a while to bring global supply chains back online and for consumers to return to their normal spending behaviors, it's possible that the U.S. economy could also post a negative GDP number for the second quarter as well. By definition, that puts the U.S. economy in a recession. But it may end up being a very brief recession as the Coronavirus reaches containment, global supply chains come back online, pent up demand for goods and services is fulfilled, and U.S. households and businesses have the dual benefit of having access to lower oil prices and lower interest rates.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

M&A Activity: Make Sure You Address The Seller’s 401(k) Plan

Buying a company is an exciting experience. However, many companies during a merger or acquisition fail to address the issues surrounding the seller’s retirement plan which can come back to haunt the buyer in a big way. I completely understand why this happens. Purchase price, valuations, tax issues, terms, holdbacks, and new employment

Buying a company is an exciting experience. However, many companies during a merger or acquisition fail to address the issues surrounding the seller’s retirement plan which can come back to haunt the buyer in a big way. I completely understand why this happens. Purchase price, valuations, tax issues, terms, holdbacks, and new employment agreements tend to dominate the conversations throughout the business transaction. But lurking in the dark, below these main areas of focus, lives the seller’s 401(k) plan. Welcome to the land of unintended consequences where unexpected liabilities, big dollar outlays, and transition issues live.

Asset Sale or Stock Sale

Whether the transaction is a stock sale or asset sale will greatly influence the series of decisions that the buyer will need to make regarding the seller’s 401(k) plan. In an asset sale, it is common that employees of the seller’s company are terminated from employment and subsequently “rehired” by the buyer’s company. With asset sales, as part of the purchase agreement, the seller will often times be required to terminate their retirement plan prior to the closing date.

Terminating the seller’s plan prior to the closing date has a few advantages from both the buyer’s standpoint and from the standpoint of the seller’s employees. Here are the advantages for the buyer:

Advantage 1: The Seller Is Responsible For Terminating Their Plan

From the buyer’s standpoint, it’s much easier and cost effective to have the seller terminate their own plan. The seller is the point of contact at the third party administration firm, they are listed as the trustee, they are the signer for the final 5500, and they typically have a good personal relationship with their service providers. Once the transaction is complete, it can be a headache for the buyer to track down the authorized signers on the seller’s plan to get all of the contact information changed over and allows the buyer’s firm to file the final 5500.

The seller’s “good relationship” with their service providers is key. The seller has to call these companies and let them know that they are losing the plan since the plan is terminating. There are a lot of steps that need to be completed by those 401(k) service providers after the closing date of the transaction. If they are dealing with the seller, their “client”, they may be more helpful and accommodating in working through the termination process even though they losing the business. If they get a random call for the “new contact” for the plan, you risk getting put at the bottom of the pile

Part of the termination process involves getting all of the participant balances out of the plan. This includes terminated employees of the seller’s company that may be difficult for the buyer to get in contact with. It’s typically easier for the seller to coordinate the distribution efforts for the terminated plan.

Advantage 2: The Buyer Does Not Inherit Liability Issues From The Seller’s Plan

This is typically the main reason why the buyer will require the seller to terminate their plan prior to the closing date. Employer sponsored retirement plans have a lot of moving parts. If you take over a seller’s 401(k) plan to make the transition “easier”, you run the risk of inheriting all of the compliance issues associated with their plan. Maybe they forgot to file a 5500 a few years ago, maybe their TPA made a mistake on their year-end testing last year, or maybe they neglected to issues a required notice to their employees knowing that they were going to be selling the company that year. By having the seller terminate their plan prior to the closing date, the buyer can better protect themselves from unexpected liabilities that could arise down the road from the seller’s 401(k) plan.

Now, let’s transition the conversation over to the advantages for the seller’s employees.

Advantage 1: Distribution Options

A common goal of the successor company is to make the transition for the seller’s employees as positive as possible right out of the gate. Remember this rule: “People like options”. Having the seller terminate their retirement plan prior to the closing date of the transactions gives their employees some options. A plan termination is a “distributable event” meaning the employees have control over what they would like to do with their balance in the seller’s 401(k) plan. This is also true for the employees that are “rehired” by the buyer. The employees have the option to:

Rollover their 401(k) balance in the buyer’s plan (if eligible)

Rollover their 401(k) balance into a rollover IRA

Take a cash distribution

Some combination of options 1, 2, and 3

The employees retain the power of choice.

If instead of terminating the seller’s plan, what happens if the buyer decides to “merge” the seller’s plan in their 401(k) plan? With plan mergers, the employees lose all of the distribution options listed above. Since there was not a plan termination, the employees are forced to move their balances into the buyer’s plan.

Advantage 2: Credit For Service With The Seller’s Company

In many acquisitions, again to keep the new employees happy, the buyer will allow the incoming employee to use their years of service with the seller’s company toward the eligibility requirements in the buyer’s plan. This prevents the seller’s employees from coming in and having to satisfy the plan’s eligibility requirements as if they were a new employee without any prior service. If the plan is terminated prior to the closing date of the transaction, the buyer can allow this by making an amendment to their 401(k) plan.

If the plan terminates after the closing date of the transaction, the plan technically belonged to the buyer when the plan terminated. There is an ERISA rule, called the “successor plan rule”, that states when an employee is covered by a 401(k) plan and the plan terminates, that employee cannot be covered by another 401(k) plan sponsored by the same employer for a period of 12 months following the date of the plan termination. If it was the buyer’s intent to allow the seller’s employees to use their years of service with the selling company for purposes of satisfy the eligibility requirement in the buyer’s plan, you now have a big issue. Those employees are excluded from participating in the buyer’s plan for a year. This situation can be a speed bump for building rapport with the seller’s employees.

Loan Issue

If a company allows 401(k) loans and the plan terminates, it puts the employee in a very bad situation. If the employee is unable to come up with the cash to payoff their outstanding loan balance in full, they get taxed and possibly penalized on their outstanding loan balance in the plan.

Example: Jill takes a $30,000 loan from her 401(k) plan in May 2017. In August 2017, her company Tough Love Inc., announces that it has sold the company to a private equity firm and it will be immediately terminating the plan. Jill is 40 years old and has a $28,000 outstanding loan balance in the plan. When the plan terminates, the loan will be processed as an early distribution, not eligible for rollover, and she will have to pay income tax and the 10% early withdrawal penalty on the $28,000 outstanding loan balance. Ouch!!!

From the seller’s standpoint, to soften the tax hit, we have seen companies provide employees with a severance package or final bonus to offset some of the tax hit from the loan distribution.

From the buyer’s standpoint, you can amend the plan to allow employees of the seller’s company to rollover their outstanding 401(k) loan balance into your plan. While this seems like a great option, proceed with extreme caution. These “loan rollovers” get complicated very quickly. There is usually a window of time where the employee’s money is moving over from seller’s 401(k) plan over to the buyer’s 401(k) plan, and during that time period a loan payment may be missed. This now becomes a compliance issue for the buyer’s plan because you have to work with the employee to make up those missed loan payments. Otherwise the loan could go into default.

Example, Jill has her outstanding loan and the buyer amends the plan to allow the direct rollover of outstanding loan balances in the seller’s plan. Payroll stopped from the seller’s company in August, so no loan payments have been made, but the seller’s 401(k) provider did not process the direct rollover until December. When the loan balance rolls over, if the loan is not “current” as of the quarter end, the buyer’s plan will need to default her loan.

Our advice, handle this outstanding 401(k) loan issue with care. It can have a large negative impact on the employees. If an employee owes $10,000 to the IRS in taxes and penalties due to a forced loan distribution, they may bring that stress to work with them.

Stock Sale

In a stock sale, the employees do not terminate and then get rehired like in an asset sale. It’s a “transfer of ownership” as opposed to “a sale followed by a purchase”. In an asset sale, employees go to sleep one night employed by Company A and then wake up the next morning employed by Company B. In a stock sale, employees go to sleep employed by Company A, they wake up in the morning still employed by Company A, but ownership of Company A has been transferred to someone else.

With a stock sale, the seller’s plan typically merges into the buyer’s plan, assuming there is enough ownership to make them a “controlled group”. If there are multiple buyers, the buyers should consult with the TPA of their retirement plans or an ERISA attorney to determine if a controlled group will exist after the transaction is completed. If there is not enough common ownership to constitute a “controlled group”, the buyer can decide whether to continue to maintain the seller’s 401(k) plan as a standalone plan or create a multiple employer plan. The basic definition of a “controlled group” is an entity or group of individuals that own 80% or more of another company.

Stock Sales: Do Your Due Diligence!!!

In a stock sale, since the buyer will either be merging the seller’s plan into their own or continuing to maintain the seller’s plan as a standalone, you are inheriting any and all compliance issues associated with that plan. The seller’s issues become the buyer’s issues the day of the closing. The buyer should have an ERISA attorney that performs a detailed information request and due diligence on the seller’s 401(k) plan prior the closing date.

Seller Uses A PEO

Last issue. If the selling company uses a Professional Employer Organization (PEO) for their 401(k) services and the transaction is going to be a stock sale, make sure you get all of the information that you need to complete a mid-year valuation or the merged 5500 for the year PRIOR to the closing date. We have found that it’s very difficult to get information from PEO firms after the acquisition has been completed.

The Transition Rule

There is some relief provided by ERISA for mergers and acquisitions. If a control group exists, you have until the end of the year following the year of the acquisition to test the plans together. This is called the “transition rule”. However, if the buyer makes “significant” changes to the seller’s plan during the transition period, that may void the ability to delay combined testing. Unfortunately, there is not clear guidance as to what is considered a “significant change” so the buyer should consult with their TPA firm or ERISA attorney before making any changes to their own plan or the seller’s plan that could impact the rights, benefits, or features available to the plan participants.

Horror Stories

There are so many real life horror stories out there involving companies that go through the acquisition process without conducting the proper due diligence and transition planning with regard to the seller’s retirement plan. It never ends well!! As the buyer, it’s worth the time and the money to make sure your team of advisors have adequately addressed any issues surrounding the seller’s retirement plan prior to the closing date.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The #1 Question To Ask Yourself Before Selling A Stock

When is the right time to sell an investment? It's a tough decision that individuals have a difficult time making but it's one of the most important decisions that you will have to make as an investor. Often time the decision to "buy" an investment is much easier. You gather information on a given investment, look at the trends in the market acting on

When is the right time to sell an investment? It's a tough decision that individuals have a difficult time making but it's one of the most important decisions that you will have to make as an investor. Often time the decision to "buy" an investment is much easier. You gather information on a given investment, look at the trends in the market acting on that investment, assess the risk versus reward trade off, and you put your strategy to work. Deciding to sell has a lot more emotions involved which frequently causes investors to make the wrong decision.

When do I sell a big winner?

First scenario is "the rocket ship". You purchased a stock and the stock price has gone through the roof. It's made you a ton of money on paper, you proudly boast to your friends and co-workers about the price that you bought it at, and in certain instances it has been a life changing financial event. The mistake investors make here is they get into what we call "the teddy bear syndrome".

Teddy bear syndrome.....

Have you ever tried to take a teddy bear away from a five year old......good luck. As adults, we often fall into the same behavioral pattern with very successful investments. Individuals typically have a strong emotional attachment to their most successful investments. But you will frequently hear many legendary investment managers make comments like: "Investment decisions are not emotional decisions. You have to remove your emotions from the decision-making process." Let's say you bought $10,000 of XYZ stock at $10 per share and five years later it's now selling at $890 per share turning your $10,000 into $890,000. Do you sell some of it, maybe all of it?

Here is the key question........

"If you had that $890,000 in cash in your hand today, would you invest all of it back into XYZ stock at $890 per share?"

Most people would say "No!! That's crazy. I would diversify that $890,000 across a number of holdings and the stock has already gone up so much". Continuing to hold a stock is the same decision as buying a stock. But doing nothing is easier because we feel like we are not making a decision, we are just "continuing to hold". Remember, it's easy to sell a stock that has lost money. It's much more difficult to sell a stock that produced a gain. Of course, this brings up the question of how do you find the right stocks to invest in?

"If I sell the stock, I'll have to pay tax on the gain."

Question: Would you rather pay taxes on a gain or lose money? Usually if you are paying taxes it means that you are making money. If I sold the stock holding in the example above, I would have an $880,000 long term capital gain at a minimum would pay around $132,000 in long term capital gains tax at 15%. This would leave me with $758,000 cash in hand from a $748,000 gain plus $10,000 original investment. What if instead of selling I continue to hold the stock and to no fault of company XYZ the economy goes into a recession? The stock goes from $890 a share to $500 a share. Now my total investment is worth $500,000 instead of $890,000. It's still a good investment because I bought it at $10,000 and it's still worth $500,000 but if I sold it at $500 per share I would still pay tax on the gain, now a smaller amount of gain, and be left with around $425,000. That poor decision cost me $333,000 after tax.

The fallen star

Most investors have been here at one point or another. You purchased a stock that rose in value dramatically but for whatever reason the stock lost all of its early investment gains and your investment is now underwater. Many investors will say “It’s a good long term holding so I’m just going to wait for it to come back.” While we are all familiar with the buy and hold strategy, there is a risk and opportunity cost with this strategy. The risk being that it may never come back to its original value. The opportunity cost is the money invested in that underperforming company could be growing somewhere else instead of just “waiting for it to come back”.

You must ask yourself the same key question that was listed above: “If I had that money in my hand today, would I invest all of it in that stock?” If the answer is “no”, you should probably sell some or all of it. Do not hold a stock solely based on a target share price. I will hear people say, “Well I bought it at $55 per share so I’m going to wait until it at least gets back to that price.” That is not an investment strategy. You must look at the fundamentals of the company, their competitors, global market conditions, company management, the company’s strategy, and their financials to really come up with a price target for the stock.

The inherited gem

It's a common occurrence that individuals will inherit stock from a family member and they know that family member had a strong emotional attachment to the stock because they either work for the company or they never sold a single share during their lifetime. It's easy to feel that selling the stock is in some way selling the memory of that family member. I will often hear comments like: "My dad worked for the company and held that stock for 40 years. He would be rolling in his grave right now if he knew I was thinking about selling his stock." This frequently happens because the generation before us had pension plans to support them in retirement and did not have to sell stock to supplement their income or they came from a generation that was very frugal about spending money. Your needs and circumstances are probably very different from the person that you inherited the stock from so you need to look at that investment holding from your financial standpoint.

I work for the company........

If you work for a publicly traded company then there is a good chance that you own shares of that company in an employee stock purchase plan, retirement plan, options plan, or brokerage account. Since you work for the company it usually means that you have "drank the kool-aide" and believe in the company's mission, vision, and you feel like you have more control over the fate of your investment. Remember, even though you work for that company it's still one company and attaching too much for your net worth to one investment is very risky. It's even more risky for employees because if something negatively impacts the company not only is your employment at risk but so is your total net worth if a large portion of your investment portfolio is tied to the company that you work for. Make sure you periodically calculate a total of all your investment holdings and compare that to the amount invested in your company's stocks to make sure you stay balanced in your overall investment approach.

Ask yourself the easy question.......

While making the decision to buy, sell, or hold an investment is not always an easy one. Finding the right answer may be as easy as asking yourself: "If the amount invested in that stock was in cash and in my hand today, would I invest 100% of it back into that stock holding?"

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Should I Buy Or Lease A Car?

This is one of the most common questions asked by our clients when they are looking for a new car. The answer depends on a number of factors:

How long do you typically keep your cars?

How many miles do you typically drive each year?

What do you want your down payment and monthly payment to be?

This is one of the most common questions asked by our clients when they are looking for a new car. The answer depends on a number of factors:

How long do you typically keep your cars?

How many miles do you typically drive each year?

What do you want your down payment and monthly payment to be?

We typically start off by asking how long clients usually keep their cars. If you are the type of person that trades in their car every 2 or 3 year for the new model, leasing a car is probably a better fit. If you typically keep your cars for 5 plus years, then buying a car outright is most likely the better option.

“How many miles do you drive each year?”

This is often times the trump card for deciding to buy instead of lease. Most leases allow you to drive about 12,000 miles per year but this varies from dealer to dealer. If you go over the mileage allowance there are typically sever penalties and it becomes very costly when you go to trade in the car at the end of the lease. We see younger individuals get caught in this trap because they tend to change jobs more frequently. They lease a car when they live 10 miles away from work but then they get a job offer from an employer that is 40 miles away from their house and the extra miles start piling on. When they go to trade in the car at the end of the lease they owe thousands of dollars due to the excess mileage.

We also ask clients how much they plan to put down on the car and what they want their monthly payments to be. If you think you can stay within the mileage allowance, a lease will more often require a lower down payment and have a lower monthly payment. Why? Because you are not “buying” the car. You are simply “borrowing” it from the dealership and your payments are based on the amount that the dealership expects the car to depreciate in value during the duration of the lease. When you buy a car……you own it……and at the end of the car loan you can sell it or continue to drive the car with no car payments.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.