How Transfer on Death (TOD) Accounts Help You Avoid Probate

Confused about transfer-on-death (TOD) accounts? This article answers the most common questions about Transfer on Death designations, how they work, and how they can help you avoid probate.

As an investment firm, we typically encourage clients to add TOD beneficiaries to their individual brokerage accounts to avoid the probate process, should the owner of the account unexpectedly pass away. TOD stands for “Transfer on Death”. When someone passes away, their assets pass to their beneficiaries in one of three ways:

Probate

Contract

Trust

Passing Asset by Contract

When you set up an IRA, 401(K), annuity, or life insurance policy, at some point during the account opening process, the custodian or life insurance company will ask you to list beneficiaries on your account. This is a standard procedure for these types of accounts because when the account owner passes away, they look at the beneficiary form completed by the account owner, and the assets pass “by contract” to the beneficiaries listed on the account. Since these accounts pass by contract, they automatically avoid the headaches of the probate process.

Probate

Non-retirement accounts like brokerage accounts, savings accounts, and checking accounts are often set up in an individual's name without beneficiaries listed on the account. If someone that passes away has one of these accounts, the decedent’s last will and testament determines who will receive the balance in those accounts - but those accounts are required to go through a legal process called “probate”. The probate process is required to transfer the decedent’s assets into their “estate”, and then ultimately distribute the assets of the estate to the estate beneficiaries.

Since the probate process involves the public court system, it can often take months before the assets of the estate are distributed to the beneficiaries of the estate. Depending on the size and complexity of the estate, there could also be expenses associated with the probate process, including but not limited to court filing fees, attorney fees, accountant fees, executor fees, appraiser fees, or valuation experts.

For this reason, many estate plans aim to avoid probate whenever possible.

Transfer On Death Designation

A very easy solution to avoid the probate process for brokerage accounts, checking accounts, and savings accounts, is to add a TOD designation to the account. The process of turning an individual account into a Transfer on Death account is also very easy because it usually only involves completing a Transfer-on-Death form, which lists the name and percentages of the beneficiaries assigned to the account. Once an individual account has been changed into a TOD account, if the account owner were to pass away, that account no longer goes through the probate process; it now passes to the beneficiaries by contract, similar to an IRA.

Frequently Asked Questions About TOD Accounts

After we explain the TOD strategy to clients, there are often several commonly asked questions that follow, so I’ll list them in a question-and-answer format:

Q: Can you change the beneficiaries listed on a TOD account at any time?

A: Yes, the beneficiaries assigned to a TOD account can be changed at any time by completing an updated TOD designation form

Q: If I list TOD beneficiaries on all of my non-retirement accounts, do I still need a will?

A: We strongly recommend that everyone execute a will for assets that are difficult to list TOD beneficiaries, such as a car, jewelry, household items, and for any other assets that don’t pass by contract or by trust.

Q: Can I list TOD beneficiaries on my house?

A: It depends on what state you live in. Currently, 31 states allow TOD deeds for real estate. New York became the newest state added to the list in 2024.

Q: Can my TOD beneficiaries be the same as my will?

A: Yes, you can make the TOD beneficiaries the same as your will. However, since TOD accounts pass by contract and not by your will, you can make beneficiary designations other than what is listed in your will.

Q: Can I list different beneficiaries on each TOD account (brokerage, checking, savings)?

A: Yes

Q: Can I list a trust as the beneficiary of my TOD account?

A: Yes

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How to Avoid the New York State Estate Tax Cliff

When someone passes away in New York, in 2025, there is a $7.16 million estate tax exclusion amount, which is significantly lower than the $13.9M exemption amount available at the federal level. However, in addition to the lower estate tax exemption amount, there are also two estate tax traps specific to New York that residents need to be aware of when completing their estate plan. Those two tax traps are:

1) The $7.5 million Cliff Rule

2) No Portability between spouses

With proper estate planning, these tax traps can potentially be avoided, allowing residents of New York to side-step a significant state tax liability when passing assets onto their heirs.

When someone passes away in New York in 2025, there is a $7.16 million estate tax exclusion amount, which is significantly lower than the $13.9M exemption amount available at the federal level. However, in addition to the lower estate tax exemption amount, there are also two estate tax traps specific to New York that residents need to be aware of when completing their estate plan. Those two tax traps are:

The $7.5 million Cliff Rule

No Portability between spouses

With proper estate planning, these tax traps can potentially be avoided, allowing residents of New York to side-step a significant state tax liability when passing assets onto their heirs.

New York Estate Tax Cliff Rule

When it comes to estate planning, it’s important to understand that estate tax rules at the federal and state levels can vary. Some states adhere to the federal rules, but New York is not one of those states. New York has a very punitive “cliff rule” where once an estate reaches a specific dollar amount, the New York estate tax exemption is eliminated, and the ENTIRE value of the estate is subject to New York state tax.

As mentioned above, the New York estate tax exemption for 2025 is $7,160,000. So, for anyone who lives in New York and passes away with an estate that is valued below that amount, they do not have to pay estate tax at the state or federal level.

For individuals that pass away with an estate valued between $7,160,000 and $7,518,000, they pay estate tax to New York only on the amount that exceeds the $7,160,000 threshold.

But the “cliff” happens at $7,518,000. Once an estate in New York exceeds $7,518,000, the ENTIRE estate is subject to New York Estate Tax, which ranges from 3.06% to 16% depending on the size of the estate.

Non-Portability Between Spouses in New York

Married couples that live in New York must be aware of how the portability rules vary between the federal and state levels. “Portability” is something that happens at the passing of the first spouse, and it refers to how much of the unused estate tax exemption can be transferred or “ported” over to the surviving spouse. The $13.9M federal estate tax exemption is “per person” and “full portable”. Why is this important? It’s common for married couples to own most assets “jointly with rights of survivorship”, so when the first spouse passes away, the surviving spouse assumes full ownership of the asset. However, since the spouse who passed away did not have any assets solely in their name, there is nothing to include in their estate, so the $13.9M federal estate tax exemption at the passing of the first spouse goes unused.

At the federal level that’s not an issue because the federal estate tax exemption for a married couple is portable, which means if the first spouse that passes away does not use their full estate tax exemption, any unused exemption amount is transferred to the surviving spouse. Assuming that the spouse who passes away first does not use any of their estate tax exemption, when the second spouse passes, they would have a $27.8 million federal estate tax exemption ($13.9M x 2).

However, New York does not allow portability, so any unused estate tax exemption at the passing of the first spouse is completely lost. The fact that New York does not allow portability requires more proactive estate tax planning prior to the passing of the first spouse.

Here is a quick example showing how this works: Larry & Kathy are married and have an estate valued at $10M in which most of their assets are titled jointly with rights of survivorship. Since everything is titled jointly, if Larry were to pass away in 2025, the $10M in assets would transfer over to Kathy with no estate taxes due at either the Federal or State level. The problem arises when Kathy passes away 2 years later. Assuming Kathy passes away with the same $10M in her name, there is still no federal estate taxes due because she more than covered by the $27.8M exemption at the federal level, however, because New York’s estate tax exemption is not portable, and her assets are well over the $7.5M cliff, the full $10M would be taxed by the New York level, resulting in close to a $1M tax liability. A tax liability that could have been completely avoided with proper estate planning.

If instead of Larry and Kathy holding all of their assets jointly, they had segregated their assets to $5M owned by Larry and $5M owned by Kathy, when Larry passed away, he would have been able to use his $7.1M New York State estate tax exemption to protect the full $5M. Then, when Kathy passed with her $5M two years later, she would have been able to use her full $7.1M New York State tax exemption, resulting in $0 in taxes paid to New York State — avoiding nearly $1M in unnecessary tax liability.

Setting Up Separate Trusts

A common solution that our clients will use to address both the $7.5M cliff and the non-portability issue in New York is that each spouse will set up their own revocable trust, and then split the non-retirement account assets in a way to maximize the $7.1M New York State exemption amount at the passing of the first spouse.

I will sometimes hear married couples say “Well, we don’t have to worry about this because our total estate is only $6 million.” That would be true today, but if that married couple is only 70 years old, and they are both in good health, what if their assets double in size before the first spouse passes? Now they have a problem.

Special Legal Disclosure: This article is for educational purposes only, and it does not contain any legal advice. For legal advice, please contact an attorney.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Multi-Generational Roth Conversion Planning

With the new 10-Year Rule in effect, passing along a Traditional IRA could create a major tax burden for your beneficiaries. One strategy gaining traction among high-net-worth families and retirees is the “Next Gen Roth Conversion Strategy.” By paying tax now at lower rates, you may be able to pass on a fully tax-free Roth IRA—one that continues growing tax-free for years after the original account owner has passed away.

With the new 10-Year Rule in place for non-spouse beneficiaries of retirement accounts, one of the new tax strategies for passing tax-free wealth to the next generation is something called the “Next Gen Roth Conversion Strategy”. This tax strategy works extremely well when the beneficiaries of the retirement account are expected to be in the same or higher tax bracket than the current owner of the retirement account.

Here's how the strategy works. The current owner of the retirement account begins to initiate large Roth conversions over the course of a number of years to purposefully have those pre-tax retirement dollars taxed in a low to medium tax bracket. This way, when it comes time to pass assets to their beneficiaries, the beneficiaries inherit Roth IRA assets instead of pre-tax Traditional IRA and 401(k) assets that could be taxed at a much higher rate due to the requirement to fully liquidate and pay tax on those assets within a 10-year period.

In addition to lowering the total income tax paid on those pre-tax retirement assets, this strategy can also create multi-generational tax-free wealth, reduce the size of an estate to save on estate taxes, and reduce future RMDs for the current account owner.

10-Year Rule for Non-Spouse Beneficiaries

This tax strategy surfaced when the new 10-Year Rule went into place with the passing of the Secure Act. Non-spouse beneficiaries who inherit pre-tax retirement accounts are now required to fully deplete and pay tax on those account balances within a 10-year period following the passing of the original account owner. In many cases when children inherit pre-tax retirement accounts from their parents, they are still working, which means that they already have income on the table.

For example, if Josh, a non-spouse beneficiary, inherits a $600,000 Traditional IRA from his father when he is age 50, he would be required to pay tax on the full $600,000 within 10 years of his father passing. But what if Josh is married and he and his wife still work and are making $360,000 per year? If Josh and his wife do not plan to retire within the next 10 years, the $600,000 that is required to be distributed from that inherited IRA while they are still working could be subject to very high tax rates since the taxable distribution stacks on top of the $360,000 that they are already making. A large portion of those IRA distributions could be subject to the 32% federal tax bracket.

If Josh’s father had started making $100,000 Roth conversions each year while both he and Josh’s mother were still alive, they could have taken advantage of the 22% Federal Tax Bracket I in 2025 (which ranges from $96,951 to $206,000 in taxable income). If they had very little other income in retirement, they could have processed large Roth conversions, paid just 22% in federal taxes on the converted amount, and eventually passed a Roth IRA on to Josh. Utilizing this strategy, the full $600,000 pre-tax IRA would have been subject to the parent’s federal tax rate of 22% as opposed to Josh’s tax rate of 32%, saving approximately $60,000 in taxes paid to the IRS.

Tax Free Accumulations For 10 More Years

But it gets better. By Josh’s parents processing Roth conversions while they were still alive, not only is there multigenerational tax savings, but when John inherits a Roth IRA instead of a Traditional IRA from his parents, all of the accumulation within that Roth IRA since the parents completed the conversion, PLUS 10 years after Josh inherits the Roth IRA, are completely tax-free.

Multi-generational Tax-Free Wealth

If you are a non-spouse beneficiary, whether you inherited a pre-tax retirement account or a Roth IRA, you are subject to the 10-year distribution rule (unless you qualify for one of the exceptions). With a pre-tax IRA or 401(k), not only is the beneficiary required to deplete and pay tax on the account within 10 years, but they may also be required to process RMDs (required minimum distributions) from their inherited IRA each year, depending on the age of the decedent when they passed away.

With an Inherited Roth IRA, the account must be depleted in 10 years, but there is no annual RMD requirement, because RMDs do not apply to Roth IRAs subject to the 10-year rule. So, essentially, someone could inherit a $500,000 Roth IRA, take no money out for 9 years, and then at the end of the 10th year, distribute the full balance TAX-FREE. If the owner of the inherited Roth IRA invests the account wisely and obtains an 8% annualized rate of return, at the end of year 10 the account would be worth $1,079,462, which would be withdrawn completely tax-free.

Reduce The Size of an Estate

For individuals who are expected to have an estate large enough to trigger estate tax at the federal and/or state level, this “Next Gen Roth Conversion” strategy can also help to reduce the size of the estate subject to estate tax. When a Roth conversion is processed, it’s a taxable event, and any tax paid by the account owner essentially shrinks the size of the estate subject to taxation.

If someone has a $15 million estate, and included in that estate is a $5 million balance in a Traditional IRA and that person does nothing, it creates two problems. First, the balance in the Traditional IRA will continue to grow, increasing the estate tax liability that will be due when the individual passes assets to the next generation. Second, if there are only two beneficiaries of the estate, each beneficiary will have to move $2.5 million into their own inherited IRA and fully deplete and pay tax on that $2.5M PLUS earnings within a 10-year period. Not great.

If, instead, that individual begins processing Roth conversions of $500,000 per year, and over a course of 10 years can fully convert the Traditional IRA to a Roth IRA (ignoring earnings), two good things can happen. First, if that individual pays an effective tax rate of 30% on the conversions, it will decrease the size of the estate by $1.5 million ($5M x 30%), potentially lowering the estate tax liability when assets are passed to the beneficiaries of the estate. Second, even though the beneficiaries of the estate would inherit a $3.5M Roth IRA instead of a $5M Traditional IRA, no RMDs would be required each year, the beneficiaries could invest the Inherited Roth IRA which could potentially double the value of the Inherited Roth IRA during that 10-year period, and withdraw the full balance at the end of year 10, completely tax free, resulting in big multi-generational tax free wealth.

The Power of Tax-Free Compounding

Not only does the beneficiary of the Roth IRA benefit from tax-free growth for the 10 years following the account owner's death, but they also receive the benefit of tax-free growth and withdrawal within the Roth IRA, as long as the account owner is still alive. For example, if someone begins these Roth conversions at age 70 and they live until age 90, that’s 20 years of compounding, PLUS another 10 years after they pass away, so 30 years in total.

A quick example showing the power of this tax-free compounding effect: someone processes a $200,000 Roth conversion at age 70, lives until age 90, and achieves an 8% per year rate of return. When they pass away at age 90, the balance in their Roth IRA would be $932,191. The non-spouse beneficiary then inherits the Roth IRA and invests the account, also achieving an 8% annual rate of return. In year 10, the Inherited Roth IRA would have a balance of $2,012,531. So, the original owner of the Traditional IRA paid tax on $200,000 when the Roth conversion took place, but it created a potential $2M tax-free asset for the beneficiaries of that Roth IRA.

Reduce Future RMDs of Roth IRA Account Owner

Outside of creating the multi-generational tax-free wealth, by processing Roth conversions in retirement, it’s shifting money from pre-tax retirement accounts subject to annual RMDs into a Roth IRA that does not require RMDs. First, this lowers the amount of future taxable RMDs to the Roth IRA account owner because assets are being shifted from their Traditional IRA to Roth IRA, and second, since RMDs are not required from Roth IRAs, the assets in that IRA are allowed to continue to compound investment returns without disruption.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

IRS Gifting Rules: Tuition vs. Student Loan Payments

Helping a family member pay for education? Make sure you're on the right side of the IRS.

Whether you're covering K–12 tuition, writing checks for college, or assisting with student loans after graduation, the tax treatment of those payments isn’t always intuitive. The IRS draws a clear line between direct tuition payments and student loan contributions—and crossing that line could mean triggering gift tax rules you didn’t anticipate.

As the cost of college and private school continues to rise, it's increasingly common for extended family members—not just parents—to want to assist with the cost of tuition or student loan payments after graduation. However, many of those family members are surprised to learn that there are different gift tax and tax reporting rules that are dependent upon whether a direct tuition payment is made versus just helping with student loan payments post-graduation.

Tuition Payment Gift Exclusion

Because there are different gift tax rules that apply when making a tuition payment on behalf of someone else versus making a student loan payment for someone else, we will start with the tuition payment scenario first. Oddly enough in the eyes of the IRS, when someone makes a tuition payment for another person, the IRS does not view it as a “gift”. However, if that same person instead decides to help a family member pay off their student loans, the IRS views that action as a “gift”. So, when we have grandparents who want to help their grandchildren pay for college, we often advise them to provide their support as tuition payments directly to the college as opposed to allowing their grandchild to take the student loans and then assisting them in repaying the student loans after they have graduated.

As long as the tuition payment is made directly to the college from the family member, it does not constitute a gift, and gifting limits do not apply. However, if the money is not remitted directly to the college, then the gifting rules do apply. Sometimes, family members make the mistake of giving money directly to the student or the parents of the student to make the tuition payments; if that happens, they have now made a gift and must follow the gift tax and reporting rules.

What about tuition for a K-12 private school? The tuition gift exclusion also applies to tuition payments for preschool and K-12 private schools.

Another important note, the gift exception only applies to tuition. It is not extended to room and board. If a non-parent pays for the room and board on behalf of a student, it is considered a gift.

Student Loan Payment Gift Tax Rules

When someone makes a loan payment on behalf of someone else, the IRS considers that a gift. This is true whether the money is given to the individual and then they make the loan payment, or if payments are made directly to the loan servicer on behalf of the college student / graduate. As mentioned earlier, there are gift reporting rules and potential gift tax implications that the individual making the gift or loan payment needs to be aware of.

Annual Gift Exclusion

For 2025, the annual gift exclusion amount is $19,000, which, for purposes of this article, means any one person can make a student loan payment for someone else up to $19,000 per year without having to worry about filing a gift tax return or paying gift tax. The number of people to whom the annual gift exclusion amount is applied is infinite, meaning if a grandparent has 3 grandchildren, and they all have student loans, a single grandparent could make student loan payments up to $19,000 for EACH grandchild, and they are completely covered by the annual gift exclusion. No action needed.

If there are two grandparents, you can double the exclusion per grandchild to $38,000, since they each have a $19,000 annual gift exclusion.

For example, Jen graduated from college with $35,000 of student loan debt; her 2 grandparents would like to pay off the $35,000 on her behalf by sending a check directly to the servicer of the student loan. Since the amount is under the $38,000 joint filer gift exclusion amount, a gift tax return does not need to be filed, and no gift taxes are due.

If instead Jen had $50,000 in student loan debt, we might advise her grandparents to remit the max gift amount this year ($38,000) and then as soon as we flip into January of the next tax year, they can remit the remaining amount ($12,000) which is also under the annual exclusion limit since it resets each year.

Gifting Over the Annual Exclusion Amount

If a student loan payment is made on behalf of a family member that exceeds the annual gift exclusion amount, a gift tax return would need to be filed in the tax year the student loan payment was made. This, however, does not mean that gift tax is due.

The IRS provides a “lifetime gift tax exclusion” amount of $13.9 million per tax filer, meaning each person would have to gift over $13.9 million during their lifetime before any gift tax is due. For a married couple, double that to $27.8 million. Thus, only the ultra-wealthy typically have to worry about paying gift tax.

Be aware that state gifting limits can vary from the federal limits, so depending on what state you live in, you may or may not owe gift tax at the state level.

While gift tax may not be due on the student loan payment that is made, just remember that if the student loan payment exceeds the annual gift exclusion amount, a gift tax return still needs to be filed.

No Tax Impact For The Person Receiving The Gift

When a cash gift is made or a student loan payment is made on behalf of someone else, the person with the student loans in their name or the recipient of the gift does not incur a tax event. It’s a tax-free event for the recipient. If gift tax is triggered, it is paid by the person making the gift, not the person who benefited from the gift.

Estate Planning Strategy

There are a number of estate planning strategies that can be implemented, acknowledging these gift tax rules.

For individuals looking to shrink the size of their estate – either to avoid estate taxes or just to begin gifting to family members - tuition payments offer a unique advantage. Since direct tuition payments do not count as gifts, this opens up the ability to make tuition payments directly to a pre-school, K-12 private school, or college that are in excess of the $19,000 annual gift exclusion amount in an effort to shrink the size of the estate or avoid the headache of the gift tax filing process.

If you want to make a gift to your child, grandchild, or other family member, but you do not want to give them the cash directly, making a payment directly to the student loan service provider can ensure that the gift is used towards the outstanding student loan balance, but it is still subject to the gift tax and reporting requirements.

What if you have some family members who have student loans, but others do not, and you want to gift equally? Option 1: Give each family member a check for the annual gift exclusion amount and tell them they can do whatever they want with the cash, apply it toward a student loan, fund a Roth IRA, down payment on a house, etc. Option 2: You can send payments directly to the loan service provider for the family members who have student loans and make direct gifts to the family members without loans. All personal preference.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Company Stock In Your 401(k)? Don’t Forget To Elect NUA

If you’re retiring or leaving your job and have company stock in your 401(k), understanding NUA (Net Unrealized Appreciation) could save you thousands in taxes. Many miss this valuable opportunity by rolling everything into an IRA without considering the tax implications. Our latest article breaks down how NUA works, common tax mistakes, and when choosing NUA makes sense. Learn how factors like your age, retirement timeline, and stock performance play a role. Don’t overlook this strategy if your company stock has grown significantly in value—it could make a big difference in your retirement savings.

For employees with company stock as an investment holding within their 401(k) accounts, there is a special distribution rule available that provides significant tax benefits called “NUA”, which stands for Net Unrealized Appreciation. The NUA option becomes available to employees who have either retired or terminated their employment with a company and are in the process of rolling over their 401(k) balances to an IRA. The purpose of this article is to help employees understand:

How does the NUA 401(k) distribution option work?

What are the tax benefits of electing NUA?

The immediate tax event that is triggered with an NUA election

What situations should NUA be elected?

What situations should NUA be AVOIDED?

Special estate tax rules for NUA shares

The Common Rollover Mistake

For employees who have company stock in their 401(k) and do not receive proper guidance, they can easily miss the window to make the NUA election, which can cost them thousands of dollars in additional taxes in their retirement years. When employees leave a company, it’s common for the employee to open a Rollover IRA and process a direct rollover of their entire balance in their 401(k) to their IRA to avoid triggering an immediate tax event as they move their retirement savings away from their former employer.

Example: Tim retires from Company ABC and has a $500,000 balance in that 401(k) plan; $200,000 of the $500,000 is invested in ABC company stock. He sets up a traditional IRA, calls the 401(k) provider, and requests that they process a direct rollover of the full $500,000 balance from his 401K to his IRA. The 401(k) platform processes the rollover, and Tim deposits the $500,000 to his IRA with no taxes being triggered. Then, Tim begins taking distributions from his IRA to supplement his income in retirement. On the surface, everything seems perfectly fine with this scenario. However, Tim may have completely missed a huge tax-saving opportunity by failing to request NUA treatment of his company stock within his 401(k) account.

How Does NUA Work?

When an employee has company stock in their 401(k) account and they go to take a distribution/rollover from their 401(k) after they leave employment with the company, they may be able to elect NUA treatment of the portion of their 401(k) that is invested in company stock. But what does NUA treatment mean? When an employee processes a rollover from their pre-tax 401(k) balance to their Rollover IRA, and then takes distributions from their IRA in the future, they have to pay ordinary income tax on all distributions taken from the IRA account. However, prior to requesting a full rollover of their 401(k) balance to their IRA, an employee with company stock in their 401(k) account can make an NUA election, which allows the appreciation in the stock within the 401(k) account to be taxed at long-term capital gains rates in the future as opposed to ordinary income tax rates which may be higher.

But employees must be aware that by electing NUA, it triggers an immediate tax event for the employee.

Here is how NUA works as an example. Sue has a 401(k) account with Company XYZ. The total balance of Sue’s 401(k) is $800,000, but $400,000 of the $800,000 balance is invested in XYZ company stock that Sue has accumulated over the past 20 years with the company. The cost basis of Sue’s $400,000 in company stock within the 401(k) is $50,000, so over that 20-year period, the company stock has gained $350,000 in value.

When Sue retires, instead of rolling over the full $800,000 balance to her Rollover IRA, she makes an NUA election. The NUA election will send the $400,000 in company stock within her 401(k) account to an after-tax brokerage account in Sue’s name as opposed to a Rollover IRA account. When that happens, Sue has to pay ordinary income tax, not on the full $400,000 value of the stock, but on the $50,000 cost basis amount of the company stock. The $350,000 in “unrealized gain” in the company stock is now sitting in Sue’s brokerage account, and when she sells the stock, she receives long-term capital gain treatment of the $350,000 gain, as opposed to paying ordinary income tax on the $350,000 gain if it was rolled over to her IRA.

But what happens to the rest of Sue’s 401(k) balance that was not invested in company stock? The non-company stock portion of Sue’s 401(k) account can be rolled over to a Rollover IRA and it’s a 100% tax-free event. She just pays ordinary income tax on future distributions from the IRA account.

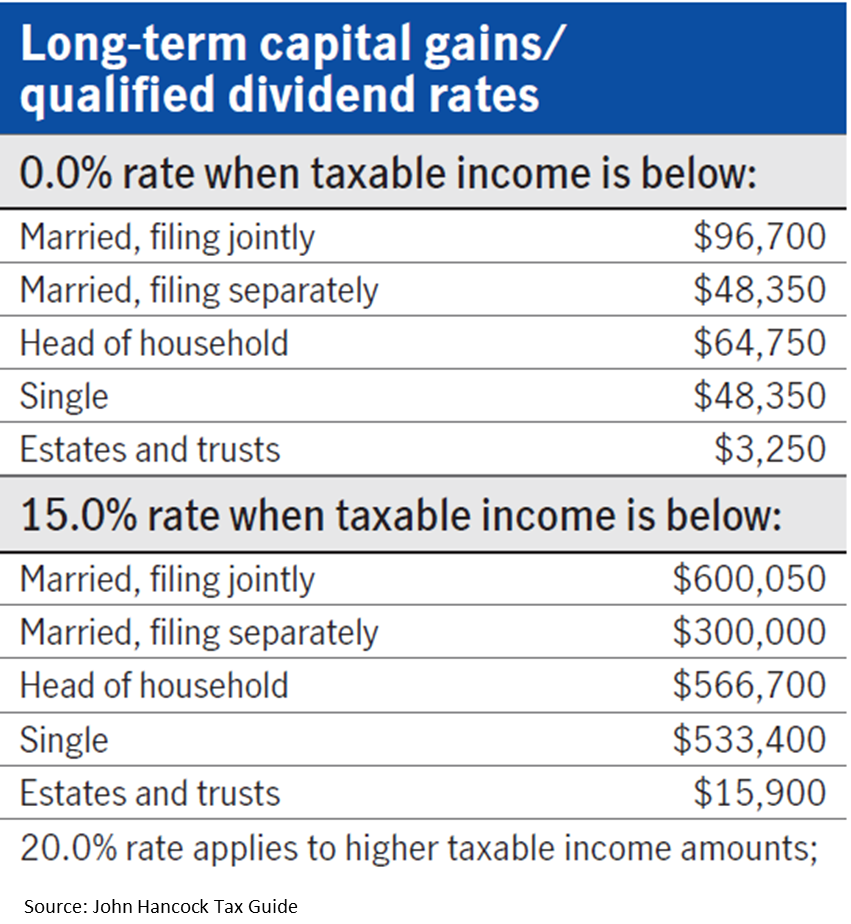

NUA – Long-Term Capital Gains Rates

Depending on Sue’s income level in retirement, her federal long-term capital gains rate may be 0%, 15%, or 20%, which may be lower than if she had realized the IRA distribution at ordinary income tax rates. Here is a quick chart that illustrates the 2025 long-term capital gains rates by filing status and income level:

NUA Triggers A Tax Event

Now let’s go back and review the tax event that was triggered when Sue requested the $400,000 transfer of her company stock from the 401(k) to her brokerage account. Again, when the NUA is processed, she only has to pay ordinary income tax on the cost basis amount of the stock, so in Sue’s case, in the year the NUA distribution takes place, she would have to report an additional $50,000 in taxable income. The tax liability generated could either be paid with her personal cash reserve or she could liquidate some of the company stock in her after-tax brokerage account to pay the taxes.

Timing of the NUA Distribution

There is a tax strategy associated with the timing of requesting the NUA distribution. If someone works for a company until September and then retires, they already have 9 months' worth of income in that tax year. In this case, it may be beneficial to process the rollover from the 401(k) with the NUA to the brokerage account the following tax year, when the individual’s W-2 income is completely off the table, so the taxable cost basis associated with the NUA election is potentially taxed at a lower rate since there is no W2 income the following year.

The Employee’s Age Matters for NUA

Because the cost basis of the company stock is treated like a cash distribution, if an employee takes an NUA distribution before age 55 and has already left the company, the cost basis would be subject to ordinary income tax and the 10% early withdrawal penalty.

NUA – Age 55 Exception To The 10% Early Withdrawal Penalty

Why age 55 and not 59½? Qualified retirement plans (401(k), 403(b), 457(b) plans) have a special exception to the under age 59½ 10% early withdrawal penalty. If you terminate employment with the company AFTER reaching age 55 and you take a cash distribution or NUA directly from the 401(k) plan, the employee is no longer subject to the 10% early withdrawal penalty. But an employee who terminates employment at age 54 and requests the NUA distribution at age 55 would still get hit with the 10% penalty because they did not separate from service AFTER reaching age 55.

The cost basis associated with the NUA distribution is treated the same as a regular cash distribution from a 401(k) plan.

When Electing NUA Makes Sense

There are certain situations where making the NUA election makes sense, and there are situations where it should be avoided. We will start off by reviewing the common situations where electing NUA makes sense in lieu of rolling over the entire balance to an IRA.

Large Unrealized Gain In The Company Stock

In order for the NUA election to make sense, there typically has to be a large unrealized gain built up in the company stock within the 401(k) plan. Said another way, the company stock has to have performed well within the 401(k) account. If the value of the company stock in an employee's 401(k) account is $200,000 and the cost basis is $170,000, if that employee elects an NUA and then transfers the $200,000 in stock to their brokerage account, it’s going to trigger a $170,000 immediate tax event and only $30,000 would receive long-term capital gains treatment. In this case, it’s probably not worth the tax hit.

In the example with Sue, she only had to pay ordinary income tax on $50,000 of the $400,000 in company stock, so the NUA would make more sense in her situation because she is shifting $350,000 to long-term capital gains treatment.

Ordinary Income Tax vs Long Term Capital Gains Rates

For NUA to make sense, it’s a race between what tax rate someone would pay if the money were distributed from a Rollover IRA and distributed at ordinary income tax rates versus the long-term capital gains tax rate if NUA is elected. Under current tax law, the federal tax rate jumps from 12% to 22% at $96,950 for a joint tax filer. On the surface it would seem that someone with under $96,950 in income might be better off rolling over the balance to an IRA and paying ordinary income tax rates at 12% instead of the long-term capital gains rate of 15%. However, if you look at the long-term capital gains tax rates in the table earlier in the article, if in 2025 a joint filer has income below $96,700, the long-term capital gains rate is 0%, and a 0% tax rate always wins.

Time Horizon Matters

An employee's time horizon to retirement also factors into the NUA decision. If an employee leaves a company at age 40, not only would they have to pay taxes and the 10% penalty on the cost basis of the NUA distribution, but by moving the company stock to a taxable brokerage account, they are losing the tax deferred accumulation benefit associated with the Rollover IRA for the next 19+ years. Since the brokerage account is a taxable account, the owner of the account has to pay taxes every year on dividends, interest, and realized gains produced by the brokerage account. If the company stock is liquidated and the full 401(k) balance is rolled over to an IRA, all of the investment income avoids immediate taxation and continues to accumulate within the IRA account. For taxpayers in higher tax brackets, this may have its advantages.

There are a lot of factors in the NUA decision, but in general, the shorter the timeline to when distributions will begin from retirement savings, the more it favors NUA; the longer the time horizon to retirement, the less it favors NUA over the benefits of continued tax deferred accumulation in a Rollover IRA account.

Reduce Future RMDs

For individuals who have a majority of their assets in pre-tax retirement accounts, like 401(k) and IRA accounts, and are fortunate enough to not need to take large distributions from those accounts in retirement because they have other sources of income, eventually when those individuals reach RMD age (73 or 75), the IRS is going to force them to start taking large taxable distributions out of their pre-tax retirement accounts.

For an individual in this situation, electing NUA can be an attractive option. Instead of their full 401(k) balance ending up in a Rollover IRA with a future RMD requirement, the company stock is sent to a brokerage account that does not require RMDs.

Estate Planning – No Step-Up In Cost Basis for NUA

Here is a little-known estate planning fact about NUA elections. Normally, when you have unrealized gains in a brokerage account and the owner of the account passes away, the beneficiaries of the estate receive a step-up in cost basis, which eliminates the taxable gain if the beneficiaries were to sell the stock. For individuals that elect NUA from a 401(k) account, there is a special rule that states if shares are deposited into a brokerage account as a result of an NUA election, the remaining portion of the NUA will be considered “income with respect of the decedent”, meaning the beneficiaries of the estate will have to pay long-term capital gains when they eventually sell those shares.

I’m not sure how this is tracked because when you move shares into a brokerage account that has NUA, if the shares continue to appreciate in value, and shares are bought and sold throughout the decedent’s lifetime, how do you determine which portion of the remaining unrealized gain was from the NUA election and which portion represents unrealized gains post NUA? A wonderful question for your tax professional if you end up in this situation.

When To Avoid NUA

As part of the analysis above, I highlighted a number of situations where an NUA election might not make sense, but a quick hit list is:

Company stock has not performed well in 401(k) account – high cost basis

High tax rate assessed on the cost basis amount during the year of NUA election

Employee under age 55 or 59½, potentially triggering early withdrawal penalty

Long time horizon to retirement (loss of tax deferred accumulation)

Ordinary tax rate lower or similar to long-term capital gains rate

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The Hidden Tax Traps in Retirement Most People Miss

Many retirees are caught off guard by unexpected tax hits from required minimum distributions (RMDs), Social Security, and even Medicare premiums. In this article, we break down the most common retirement tax traps — and how smart planning can help you avoid them.

Most people think retirement is the end of tax planning. But nothing could be further from the truth. There are several tax traps that retirees encounter, which range from:

How RMDs create tax surprises

How Social Security is taxed

How Medicare Premiums (IRMAA) are affected by income

A lack of tax-specific distribution planning

We will be covering each of these tax traps in this article to assist retirees in avoiding these costly mistakes in the retirement years.

RMD Tax Surprises

Once you reach a specific age, the IRS requires individuals to begin taking mandatory distributions from their pre-tax retirement accounts, called RMDs (required minimum distributions). Distributions from pre-tax retirement accounts represent taxable income to the retiree, which requires advanced planning to ensure that that income is not realized at an unnecessarily high tax rate.

All too often, Retirees will make the mistake of putting off distributions from their pre-tax retirement accounts until RMDs are required to begin, which allows the pretax accounts to accumulate and become larger during retirement, which in turn requires larger distributions once the RMD start age is reached.

Here is a common example: Tim and Sue retire from New York State at age 55 and both have pensions that are more than enough to meet their current expenses. Both of them also have retirement accounts through NYS, totaling $500,000. Assuming Tim and Sue start taking their required minimum distributions (RMDs) at age 75, and since Tim and Sue do not need to take withdrawals from their retirement account to supplement their income, those retirement accounts could grow to over $1,000,000. This sounds like a good thing, but it creates a potential tax problem. By age 75, they’ll both be receiving their pensions and have turned on Social Security, which under current tax law is 85% taxable at the federal level. On top of that, they’ll need to take a required minimum distribution of $37,735 which stacks up on top of all their other income sources.

This additional income from age 75 and beyond could:

Be subject to higher tax rates

Trigger higher Medicare Premiums

Cause them to phase out of certain tax deductions or credits

In hindsight, it may have been more prudent for Tim & Sue to begin taking distributions from their retirement accounts each year beginning the year after they retired, to avoid many of these unforeseen tax consequences 20 years after they retired.

How Is Social Security Taxed?

I start this section by saying, based on current law, because the Trump administration has on its agenda to make social security tax-free at the Federal level. At the time of this article, social security is potentially subject to taxation at the federal level for individuals based on their income. A handful of states also tax social security benefits.

Here is a quick summary of the proportion of social security benefits subject to taxation at the Federal level in 2025:

0% Taxable: Combined income for single filers below $25,000 and joint filers below $32,000.

50% Taxable: Combined income for single filers between $25,000 - $34,000 and joint filers between $32,000 - $44,000

85% Taxable: Combined income for single filers above $34,000 and joint filers above $44,000.

One-time events that occur in retirement could dramatically impact the amount of a retiree's social security benefit, subject to taxation. For example, a retiree might sell a stock at a gain in a brokerage account, surrender an insurance policy, earn part-time income, or take a distribution from a pre-tax retirement account. Any one of these events could inadvertently trigger a larger tax liability associated with the amount of an individual’s social security that is subject to taxation at the Federal level.

Medicare Premiums Are Income-Based

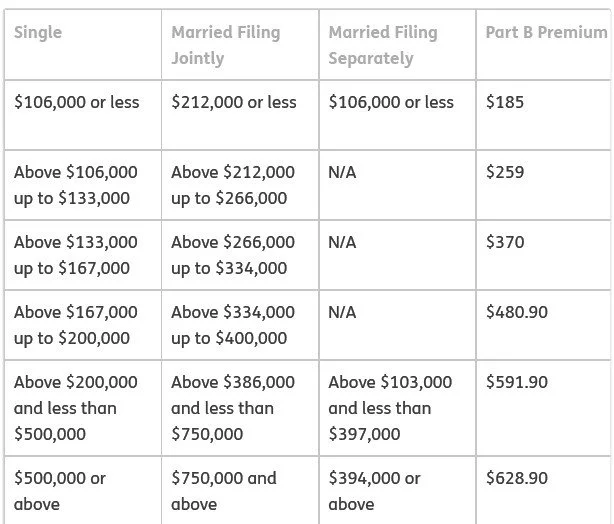

When you turn age 65, many retirees discover for the first time that there is a cost associated with enrolling in Medicare, primarily in the form of the Medicare Part B premiums that are deducted directly from a retiree's monthly social security benefit. The tax trap is that if a retiree shows too much income in a given year, it can cause their Medicare premium to increase for 2 years in the future.

Medicare looks back at your income from two years prior to determine the amount of your Medicare Part B premium in the current year. Here is the Medicare Part B premium table for 2025:

As you can see from the table, as income rises, so does the monthly premium charged by Medicare. There are no additional benefits, the retiree just has to pay more for their Medicare coverage.

This is where those higher RMDs can come back to haunt retirees once they reach the RMD start age. They might be ok between ages 65 – 75, but once they hit age 75 and must start taking RMDs from their pre-tax retirement accounts, those pre-tax RMD’s can sometimes push retirees over the Medicare based premium income threshold, and then they end up paying higher premiums to Medicare for the rest of their lives that could have been avoided.

Lack of Retirement Distribution Planning

All these tax traps surface due to a lack of proper distribution planning as an individual enters retirement. It’s incredibly important for retirees to look at their entire asset picture leading up to retirement, determine the income level that is needed to cover expenses in their retirement year, and then construct a long-term distribution plan that allows them to minimize their tax liability over the remainder of their life expectancy. This may include:

Processing sizable distributions from pre-tax accounts early in the retirement years

Processing Roth conversions

Delaying to file for social security

Developing a tax plan for surrendering permanent life insurance policies

Evaluating pension and annuity elections

A tax plan for realizing gains in taxable investment accounts

Forecasting RMDs at age 73 or 75

Developing a robust distribution plan leading up to retirement can potentially save retirees thousands of dollars in taxes over the long run and avoid many of the pitfalls and tax traps that we reviewed in the article today.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Trump Has The Stock Market and Fed Cornered

The stock market selloff continues amid the escalation of the trade wars between the US and 180 other countries. It’s left investors asking the questions:

Where is the bottom?

Are we headed for a recession?

Unfortunately, the answers are largely rooted in the decisions that President Trump makes in the coming days and weeks. There have been talks about the Fed decreasing rate, tax reform getting passed sooner, negotiations beginning with 50 of the 180 countries that we placed tariff on, but in this article we are going to explain why all of these solutions may be too little too late when it comes to the overall negative impact that tariff are currently having on the US economy.

The stock market selloff continues amid the escalation of the trade wars between the U.S. and 180 other countries, and it’s left investors asking the questions:

Where is the bottom?

Are we headed for a recession?

Unfortunately, the answers are largely rooted in the decisions that President Trump makes in the coming days and weeks. There have been talks about the Fed decreasing rates, tax reform getting passed sooner, and negotiations beginning with 50 of the 180 countries that we placed tariffs on. In this article, we are going to explain why all of these solutions may be too little too late when it comes to the overall negative impact that tariffs are currently having on the U.S economy.

Trump Holds All of the Cards

In our opinion, the only way out of this market selloff is a policy pivot by the Trump administration on the latest round of tariffs - which could be announced ant any moment. Markets would likely respond very positively to any sign of relief. This could come in the form of a “pause” in the assessments of the tariffs for a specific number of days to provide time for negotiations to take place, or the Trump administration could reverse course, either walking back or reducing the tariff amounts that are currently being assessed.

Notice that I didn’t add to the list that “tariffs are either eliminated or reduced by successfully negotiating with 180 countries on which tariffs have been placed.” While this would typically be an option, we do not believe that the Trump administration has the manpower to successfully negotiate with 180 countries simultaneously in a way that would reduce or eliminate the tariffs before they negatively impact the global economy.

The magnitude of the tariff is a real problem, and we believe this to be one of the big missteps by the Trump administration in trade negotiations. The reciprocal tariffs are not based on the tariffs that are being levied against U.S. goods being imported by other countries, but rather a formula by the Trump administration that’s based on the trade deficit between the U.S. and these various countries, which is not prudently resolved through the assessment of tariffs.

For example, let's say that Japan assesses a 5% tariff against U.S. imports. Since the U.S. imports more from Japan than Japan imports from the U.S., this results in a trade deficit between the two countries. The Trump administration has decided not to levy a reciprocal tariff based on the 5% actual tariff levied against U.S. goods but rather is assessing a much larger tariff based on the amount of the trading deficit between the U.S. and Japan. However, this might not be the root cause of the trade imbalance. Another example: let's say the U.S. consumer prefers buying Japanese electronics, but there aren’t naturally many things that Japan buys or needs from the U.S. This would cause exports from Japan to exceed imports from the U.S., which is being driven largely by consumer demand, not tariffs. However, the Trump administration is now assessing sizable tariffs against Japan to try to reduce the trade deficit. In effect, this approach either forces Japan to buy more goods from the U.S. or for the U.S. consumer to buy less goods imported from Japan - even those products are preferred for their quality over alternatives from other countries.

In a way, the Trump administration is trying to use a hammer to fix a problem that requires a screwdriver. In addition, it was recently pointed out on an analyst call that since the United States spends more than it makes, we are naturally going to run deficits with other countries because we're purchasing more than we produce as a country. If we are concerned with the U.S. trade deficits, and although tariffs may be a contributing factor, the lion’s share of the problem may be the U.S. just outspending what we produce each year.

Tariffs are Paralyzing the Global Economy

While we have seen the tariffs being implemented this week, just the threat of tariffs has a paralyzing impact on both the U.S. and global economy. Since there is so much at stake in the negotiation of these tariffs, it causes companies to put off purchasing decisions, hiring decisions, new construction, and encourages companies to sit on their cash, not knowing which direction the economy will go from here.

Not only do we need a pause, delay, or elimination of the tariff to stave off a recession, but it needs to happen within a reasonable period of time, because the reduction in spending by consumers and businesses during this wait-and-see approach is already reducing the GDP in Q2, which could push the QDP negative in Q2 and potentially Q3. Two consecutive quarters of negative GDP is a recession.

Delay In Building New Factories

While the Trump administration's main goal with the trade negotiations is to bring more manufacturing back to the United States, these are multibillion-dollar decisions for these publicly traded companies. For example, it’s estimated that if Apple were to move forward with building a new multi-billion facility in the U.S., it might take them 10 years to build it. The catalyst for building it in the first place would be to avoid having to pay the tariffs on iPhones that are being imported from China. But if you're Apple, do you commit to spending billions to build a new factory in the US when in 4 years there could be a change in the administration in Washington and then the tariffs could be removed, making it no longer prudent to produce hardware in the United States? These are the decisions that these big multinational companies face before pulling the trigger on bringing manufacturing back to the United States.

Labor Shortage

Another reasonable question to ask is if all these manufacturing jobs come back to the United States, do we have enough workers to hire in the U.S. to run those factories? The unemployment rate in the U.S. is 4.2%, which is well below the 6% historical trend. With the Trump administration greatly limiting immigration into the U.S., it’s difficult to pinpoint where all these additional workers would come from within the U.S.

The Fed is Stuck

The Fed is stuck between a rock and a hard place. Normally, when there is weakness in the U.S. economy, the Fed will step in and begin lowering interest rates. However, tariffs are inflationary, so if the Fed begins reducing rates to help the economy while prices are moving higher because of the tariffs, it could result in another round of hyperinflation like we saw coming out of COVID. This may cause the Fed to stay on pause, meaning the markets may not receive any immediate help from the Fed in the near future.

Tax Reform

There is also the argument to be made that weakening the U.S. economy may allow larger tax cuts to be passed with the anticipation of the Trump tax cuts that are currently working their way through Congress. While this may very well be true, again, it’s a timing issue. Tax reform is a slow-moving animal, and even in the best-case scenario, we may not see the tax reform passed until August 2025 or later, but by then the U.S. economy could already be in a recession if the tariff issues are not resolved.

Waiting For the Recovery

The economy is truly balancing on the edge of a knife right now. An announcement at any moment from the Trump administration indicating a pause or reduction of the tariff could make the last few weeks just a bad dream. But it’s not just that relief happens, but that the U.S. economy likely needs to receive that relief soon to avoid too much damage from happening due to the economic paralysis in the interim. There are very few moments in history where so much is riding on policy coming out of Washington that it becomes difficult to predict which path the U.S. economy will follow in coming weeks and months. This is truly a situation where investors will have to assess the data each day and what the developing trends in the economic data are to determine whether or not changes should be made to their asset allocation.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Trump’s Reciprocal Tariff: Renegotiating with the World

Yesterday, April 2, 2025, President Trump announced new tariffs, referred to as “reciprocal tariffs,” against more than 180 countries simultaneously. Both the magnitude of the tariffs and the number of countries against which they will be levied far exceeded market expectations. This raises new concerns for investors regarding how these new tariff policies will impact the US economy, both in the short term and long term.

While policy can be debated regarding whether or not the new tariffs will bring positive long-term change to the US economy, we believe that additional risk may lie in the method by which the new policy is being implemented. As we have seen in business many times, the right strategy, executed the wrong way, can lead to unexpected negative outcomes.

Yesterday, April 2, 2025, President Trump announced new tariffs, referred to as “reciprocal tariffs,” against more than 180 countries simultaneously. Both the magnitude of the tariffs and the number of countries against which they will be levied far exceeded market expectations. This raises new concerns for investors regarding how these new tariff policies will impact the U.S. economy, both in the short-term and long-term.

While policy can be debated on whether or not the new tariffs will bring positive long-term change to the U.S. economy, we believe that additional risk may lie in the method by which the new policy is being implemented. As we have seen in business many times, the right strategy, executed the wrong way, can lead to unexpected negative outcomes.

Separating Policy from Politics

As an investment advisor, it’s often challenging to present emerging trends in the markets and economy without the message sounding political, especially when policy coming from Washington is driving the trends. When making investment decisions for portfolios, we have found it to be increasingly important to separate politics and policy, requiring us to leave any political biases at the door.

Many investors struggle with this concept because half the country supports Trump, while the other half can’t stand him, and it’s often difficult for investors to set aside their personal and political biases when making prudent investment decisions. Admittedly, we are living in a time when it has never been more difficult to accomplish this, yet being able to separate the two has never been more important. A true challenge for both investors and investment advisors alike.

Trump’s Reciprocal Tariff Plan

Trump presented in his announcement yesterday that these are not just baseless tariffs, but rather reciprocal tariffs based on the current tariffs that exist in these 180+ countries on U.S. goods imported. More specifically, the Trump administration conducted a “current tariff” calculation, with U.S. reciprocal tariffs equal to 50% of the tariff amounts being imposed on U.S. goods by those countries.

The overall aim of this policy is to create a more level playing field when it comes to trade with our various trading partners with the simple solution of, “you drop your tariffs on us, and we will drop our tariffs on you”.

On the surface, from a pure policy standpoint, it makes sense that if Japan is levying 40%+ tariffs on goods imported from the U.S., and the U.S., on average, is only imposing a 2.5% tariff on goods imported from Japan, why is that fair? (I’m just using these tariff percentages for example, the actual tariff amounts are different) By having these large tariff imbalances, it makes the goods produced in the U.S. more expensive when sold abroad, which ultimately hurts manufacturing in the U.S. and the U.S. labor that supports our manufacturing industry.

According to the Trump administration, this tariff imbalance has been in existence for 20+ years, and has been accepted as the norm, but they made a clear statement yesterday that the time has come to end this imbalance.

I can understand how a tariff imbalance between trading partners can add to the U.S. deficit since tariffs on our goods imposed by other countries make U.S. manufactured goods more expensive when sold abroad, but if we levy little to no reciprocating tariffs, goods produced by those countries that are imported into the U.S. do not face those same price hurdles from the U.S. consumer. With our government deficits spiraling out of control, taking steps to create a better balance between exports and imports, or at least encouraging the consumer to purchase more U.S.-made goods, probably makes sense in the long-term.

From a pure policy standpoint, we must acknowledge that new reciprocal tariffs, while they may create economic disruption in the short-term, they may also reset the global table on trade to set the U.S. economy on a more sustainable path to prosperity over the long term without having to continue to rely on rising government deficits to finance the trade imbalances.

Risk Exists in the Improper Execution of The Strategy

Only history will be able to tell us whether the new trade policy being implemented will be successful or not, but we have greater concern over the method by which the new policy is being implemented. If you have trade imbalances with over 180 countries that you are trying to resolve, is it prudent to attempt to renegotiate 20+ years of policy with more than 180 countries in one public announcement? What is the likelihood that by choosing this approach, agreements will be reached with all 180 countries within the next few weeks to avoid unnecessary harm to the U.S. economy? The chances are slim.

This is where we feel the risk lies as the negotiation process begins with all 180+ countries, because the timeline to resolution is a pivotal piece in determining the impact on the U.S. economy over the next six months. In the past, President Trump focused trade negotiations on just one or two countries at a time, which made it easier to resolve, delay, or negotiate down “trade wars” fairly quickly. Now, attempting to negotiate with 180 countries at once seems unrealistic. While the proposed solution—“You drop your tariffs on us, and we’ll drop ours on you”—sounds simple, it underestimates the complexity of these trade relationships as each country negotiates to protect its own economic interests.

Investment In the U.S. & Jobs

It was a little surreal yesterday seeing the head of the U.S. Auto Workers Union providing full support for a Republican president during the tariff announcement since historically the unions have aligned themselves with the Democratic party, but I think it highlights some of the pain that is being felt in places like Detroit for all of the off shoring of manufacturing and labor over the past 10 – 15 years. While there is real risk to these trade wars and real economic risk to the rapid rollout of these new policies, it may encourage a return of manufacturing to the U.S. with companies like Apple, Toyota, and Nvidia investing hundreds of billions of dollars to build facilities within the U.S. to avoid the assessment of the tariffs. Again, time will tell.

Allocation Shift

While the long-term outcome of these new trade policies is unknown, for investors with short- to medium-term time horizons, I think it’s important to acknowledge the near-term risks given the magnitude of the tariffs, the number of countries against which they are being levied, and the speed of the rollout, to determine how this new policy could impact the U.S. economy over the next 6 months.

With that said, this is not a “run for the hills” moment. We acknowledge at this point the additional challenges that these new reciprocal tariffs present, as well as the unknown timeline for resolving these tariffs with our 180+ trading partners. We will need to closely monitor the economic data over the next few weeks and months to assess its impact on labor markets, the U.S. consumer, the overall economy, and, if necessary, respond with allocation changes within client accounts.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The March Selloff – Trouble on the Surface

March was a tough month for the stock market, with the S&P 500 Index dropping by over 5% for the month. With the new “Liberation Day” tariffs going into effect on April 2nd, many investors are asking if the new tariffs and the recent stock market correction warrant a change in investment strategy. Will the selloff continue, or are we in store for a market rally in April?

In this article, we will share our market analysis, highlight key economic data points to watch as the new tariffs are rolled out, and answer the question: Do recent events warrant a change in investment strategy?

After conducting hundreds of client meetings over the past 90 days, I would best describe investors' overall sentiment as “emotionally charged.” There is a lot of fear, anxiety, and uncertainty, with no shortage of media headlines on a daily, and often hourly, basis. Historically, in the short term, the market is not a fan of this type of environment which may have been a significant contributor to the more than 5% selloff in the S&P 500 Index in March. However, if there is a lesson that I have learned over the past 20 years in the investment industry, it’s that emotions can easily lead to investors making irrational investment mistakes, with “fear” serving as the captain of that team.

That then begs the question, how do you know when fear is warranted versus when fear is a distraction? The answer: look at the data. Data is unemotional. Data often reveals what’s really happening in labor markets, the economy, consumer behavior, the historical impact of policies coming out of Washington, and more. Data also enables us to examine the historical trends of similar data in the past and use them to forecast potential outcomes in the future.

Today, I’ll be sharing with you the key data points that may help determine where the markets go from here.

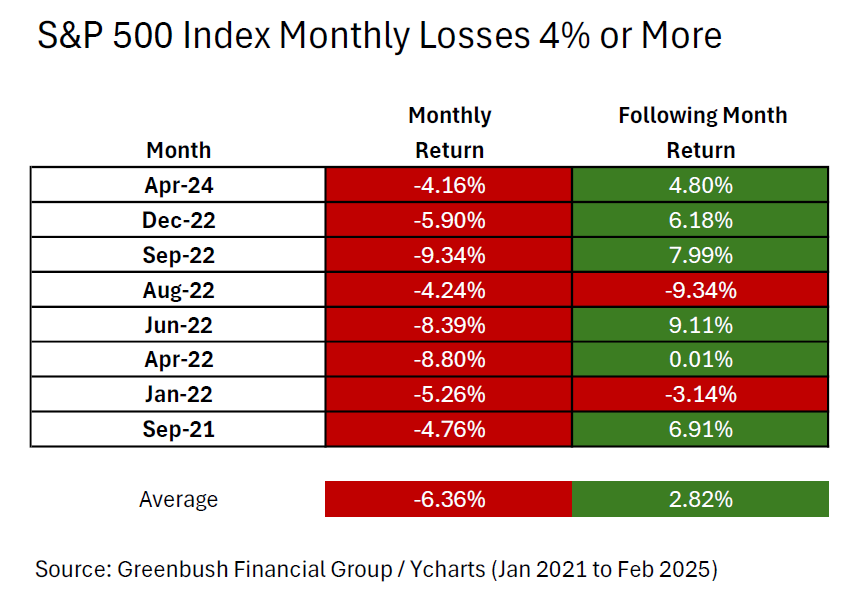

Data Point #1: 8

Prior to the recent 5%+ selloff in the S&P 500 Index in March, 8 is the number of times since January 2021 that the S&P 500 Index has dropped by more than 4% in a single month.

Data Point #2: -6.36%

For the 8 months that the S&P 500 Index dropped by over 4% in a single month between January 2021 and February 2025, -6.36% was the average monthly drop in the S&P 500 Index during that 8 month period. The S&P 500 was down 5.8% for the month of March.

Data Point #3: 6 of 8

Important next question: After the S&P 500 Index dropped by more than 4% in each of those months, did the losses historically continue, or did the market typically stage a recovery in the following month? In 6 of the 8 occurrences, the S&P 500 posted a positive return in the month following the 4%+ monthly drop.

Data Point #4: 2.82%

If we look at ALL eight 1-month periods following the month that the S&P 500 Index dropped by 4%+ in a single month, on average, the S&P 500 Index was up 2.82% in the following month.

Here is the chart with all the data for Data Points #1 through #4:

Trump 1.0 versus Trump 2.0

When President Trump announced the first round of tariffs in February 2025, we released an article comparing the market behavior we were seeing under Trump 2.0 versus the market trends and reactions to Trump’s policies during his first term (Trump 1.0).

Article: Trump Tariffs 2025 vs Trump Tariffs 2017

Again, more data. During Trump’s first term, he announced tariffs throughout the 4-year period, he signed waves of executive orders, there were multiple sizable sell-offs in the stock market, and market volatility remained high throughout his first four-year term. It was an “emotionally charged” environment similar to now. However, what we also pointed out in that article is that, ignoring the emotions, market volatility, and politics, the S&P 500 Index was up just over 16% annualized during the Trump 1.0 era.

Will history repeat itself? Since he just took office two months ago, we still need more time to collect the economic data to compare the trend. While we acknowledge that the tariffs being levied under Trump 2.0 are impacting more countries than those under Trump 1.0, the knee-jerk reaction from markets is similar today as to what we saw during Trump’s first term.

Tax Reform is Yet To Come

The news outlets right now are filled with headlines about new tariffs, federal employee layoffs, inflation risks, recession fears, and more. The one positive item that may be getting lost in the mix is that since the Republicans control Congress and the White House, there is a high probability that the Tax Cut and Jobs Act that were set to expire will get extended, and additional favorable tax provisions will most likely be passed either the second half of 2025 or in 2026.

Data Point #5: 5 of 7

Since 1945, Congress has passed 7 major tax reform bills. In 5 of the 7 years that major tax reform was passed, the S&P 500 Index posted a positive return for the year.

Data Point #6: 13.12%

If you total up the S&P 500 Index performance in each of the 7 years that tax reform was passed (both the positive and negative years), the S&P 500 Index averaged a 13.12% annual rate of return in the year that tax reform was passed by Congress. The explanation is easy: lower taxes means more money stays in the pockets of individuals and corporations, that money is then spent, and the U.S. is still largely a consumer-driven economy.

A special note here as well: if consumers and corporations have more money from lower taxes, that may help them weather some of the price increases resulting from the tariff activity.

Politics, Emotions, and Investing

March was a tough month for the markets. It’s never fun looking at a monthly statement following a 5.8% drop in the stock market. I shared with you today a few of the many data points that we are tracking across markets and the economy to assist our clients in making informed investment decisions that will enable them to meet their short-, medium-, and long-term financial objectives. In periods of heightened emotion, calm can often be found in looking beyond the politics and news headlines, and focusing on hard data and historical trends that can guide us in determining whether or not changes should be made to the asset allocation in client accounts.

Even after turning the page on a tough month for the market, we have yet to see a meaningful deterioration in the economic data within the economy. If the tariffs that are being implemented begin to have an significant impact on the economy, we would expect to see a meaningful rise in the unemployment rate as companies begin to lay off workers, a drop in manufacturing hours worked, a drop in new housing permits, and a steeper inversion of the yield curve, and we have yet to see a meaningful change in any of those data points.

It's also important to remember that one or two months of bad data is not a meaningful trend, and there is not a single indicator that, by itself, trips the alarm bells. Rather, it is a combination of multiple indicators over a multi-month period of time where meaningful trends develop and can be used in determining whether or not the current environment warrants a change in investment strategy.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Turning on Social Security Early? Keep Your Final Paystub to Avoid Penalties

Deciding to take Social Security benefits early can be a practical choice for many retirees, but it comes with potential challenges. One major consideration is the earned income penalty, which could reduce your benefits if you’re still earning income over a certain threshold. But there is a flaw in the Social Security system that sometimes incorrectly assesses the earned income penalty. When someone retires, oftentimes their income for the year is already above the $23,400 earned income threshold but very few retirees realize that if their social security benefit is not turned on until after they receive their final paycheck, the earned income penalty will not apply even though social security may attempt to assess the penalty anyways.

The good news? With proper planning and documentation, such as holding onto your final paystub, you can avoid unnecessary penalties and protect your benefits.

If you are planning to retire prior to your social security full retirement age, and you are also planning on turning on your social security benefits as soon as you retire, you have to be aware of a flaw in the social security system that may automatically prompt social security to attempt to assess an earned income penalty error against your social security benefit in the year that you retire.

Social Security Earned Income Penalty

If you elect to begin receiving Social Security benefits prior to your full retirement age, Social Security assesses a penalty against the Social Security benefits that you receive if your earned income exceeds a specific threshold. That limit in 2025 is $23,400. If you have earned income over $23,400, and you file for social security benefits prior to your FRA, social security will assess a penalty equal to $1 for every $2 over the $23,400 threshold.

For example, Scott retires at age 63; his full retirement age for Social Security is 67, but he elects to file for Social Security benefits as soon as he retires. Scott continues to work part-time and makes $35,000. Since Scott’s income is $11,600 over the $23,400 threshold, social security will assess a $5,800 penalty against Scott’s social security benefit in the following year.

Social security does not assess the penalty by requesting a check from Scott, instead, if Scott was receiving $2,000 per month in Social Security, then the following year they would withhold 3 months of social security payments from Scott, totaling $6,000 to cover the penalty, and then Scott’s monthly benefit would resume after the penalty months have been assessed.

Note: Social security does not withhold partial months for the penalty; if $100 is still owed in the penalty and the monthly SS benefit is $2,400, social security will withhold the full $2,400 monthly benefit to assess the final $100 penalty amount owed.

Flaw In Assessment of Social Security Income Penalty

There is a common flaw in the assessment of the Social Security earned income penalty in the year that an individual retires because it’s a common occurrence that prior to an individual actually retiring, they may have already earned more than the $23,400 income threshold with their employer prior to turning on their social security benefits. Will they be doomed and have to pay the SS penalty, or is there a way to appeal the earned income penalty in these cases?

Thankfully, it’s the latter of the two. In the year that you retire, if you stop working and then turn on your social security benefits AFTER you have stopped working, the income earned prior to the month that you turned on your social security benefits is ignored for purposes of the social security earned income penalty.