Navigating Student Loan Repayment Programs

I had the fortunate / unfortunate experience of attending a seminar on the various repayment programs available to young professionals and the parents of these young professionals with student loan debt. I can summarize it in three words: “What a mess!!” As a financial planner, we are seeing firsthand the impact of the mounting student loan debt

I had the fortunate / unfortunate experience of attending a seminar on the various repayment programs available to young professionals and the parents of these young professionals with student loan debt. I can summarize it in three words: “What a mess!!” As a financial planner, we are seeing firsthand the impact of the mounting student loan debt epidemic. Only a few years ago, we would have a handful of young professional reach out to us throughout the year looking for guidance on the best strategy for managing their student loan debt. Within the last year we are now having these conversations on a weekly basis with not only young professionals but the parents of those young professional that have taken on debt to help their kids through college. It would lead us to believe that we may be getting close to a tipping point with the mounting student loan debt in the U.S.

While you may not have student loans yourself, my guess is over next few years you will have a friend, child, nephew, niece, employee, or co-working that comes to you looking for guidance as to how to manage their student loan debt. Why you? Because there are so many repayment programs that have surfaced over the past 10 years and there is very little guidance out there as to how to qualify for those programs, how the programs work, and whether or not it’s a good financial move. So individuals struggling with student loan debt will be looking for guidance from people that have been down this road before. This article is not meant to make you an expert on these programs but is rather meant to provide you with an understanding of the various options that are available to individuals seeking help with managing the student loan debt.

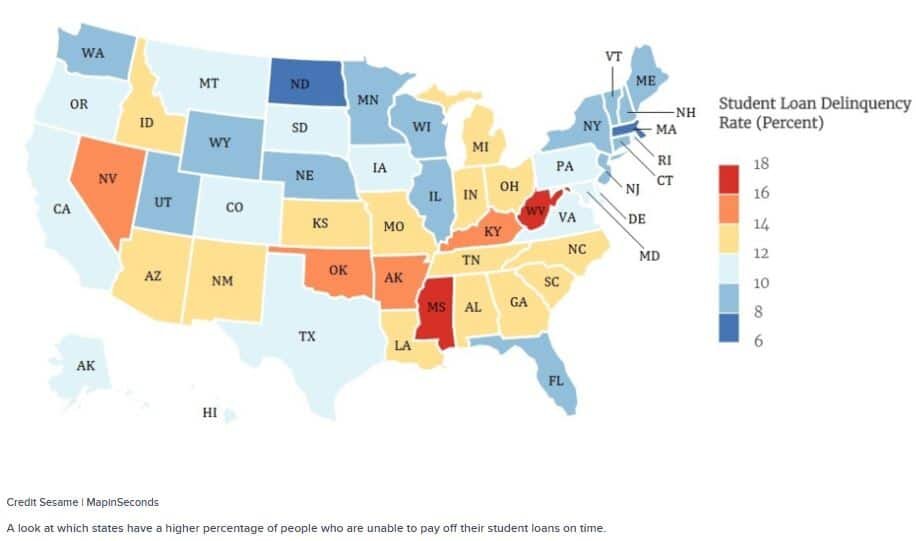

Student Loan Delinquency Rate: 25%

While the $1.5 Trillion dollars in outstanding student loan debt is a big enough issue by itself, the more alarming issue is the rapid rise in the number of loans that are either in delinquency or default. That statistic is 25%. So 1 in every 4 outstanding student loans is either behind in payments or is in default. Even more interesting is we are seeing a concentration of delinquencies in certain states. See the chart below:

Repayment Program Options

Congress in an effort to assist individuals with the repayment of their student loan debt has come out with a long list of repayment programs over the past 10 years. Upfront disclosure, navigating all of the different programs is a nightmare. There is a long list of questions that come up like:

Does a “balanced based” or “income based” repayment plan make the most sense?

What type of loan do you have now?

It is a federal or private loan?

When did you take the loan?

Who do you currently work for?

What is current interest rate on your loan?

What is your income?

Are you married?

Because it’s such an ugly process navigating through these programs and more and more borrowers are having trouble managing their student loan debt, specialists are starting to emerge that know these programs and can help individuals to identify which programs is right for them. Student loan debt management has become its own animal within the financial planning industry.

Understanding The Grace Period

Before we jump into the programs, I want to address a situation that we see a lot of young professional getting caught in. Most students are aware of the 6 month grace period associated with student loan payment plans. The grace period is the 6 month period following graduation from college that no student loan payments are due. It gives graduates an opportunity to find a job before their student loan payments begin. What many borrowers do not realize is the “grace period’ is a one-time benefit. Meaning if you graduate with a 4 year degree, use your grace period, but then decide to go back for a master degree, you can often times put your federal student loans in a “deferred status” while you are obtaining your master degree but as soon as you graduate, there is no 6 month grace period. Those student loan payments begin the day after you graduate because you already used your 6 month grace period after your undergraduate degree. This can put students behind the eight ball right out of the gates.

What Type Of Loan Do You Have?

The first step is you have to determine what type of student loan you have. There are two categories: Federal and Private. The federal loans are student loans either issued or guaranteed by the federal government and they come in three flavors: Direct, FFEL, and Perkins. Private loans are student loans issued by private institutions such as a bank or a credit union.

If you are not sure what type of student loan you have you should visit www.nslds.ed.gov. If you have any type of federal loan it will be listed on that website. You will need to establish a login and it requires a FSA ID which is different than your Federal PIN. If your student loan is not listed on that website, then it’s a private loan and it should be listed on your credit report.

In general, if you have a private loan, you have very few repayment options. If you have federal loans, there are a number of options available to you for repayment.

Parties To The Loan

There are four main parties involved with student loans:

The Lender

The Guarantor

The Servicer

The Collection Agency

The lender is the entity that originates the loan. If you have a “direct loan”, the lender is the Department of Education. If you have FFEL loan, the lender is a commercial bank but the federal government serves as the “Guarantor”, essentially guaranteeing that financial institutions that the loan will be repaid.

Most individuals with student loan debt or Plus loans will probably be more familiar with the name of the loan “Servicer”. The loan servicer is a contractor to the bank or federal government, and their job is to handle the day-to-day operations of the loan. The names of these servicer’s include: Navient, Nelnet, Great Lakes, AES, MOHELA, HESC, OSLA, and a few others.

A collection agency is a third party vendor that is hired to track down payments for loans that are in default.

Balance-Based Repayment Plans

These programs are your traditional loan repayment programs. If you have a federal student loan, after graduate, your loan will need to be repaid over one of the following time periods: 10 years, 25 years, or 30 years with limitations. The payment can either be structure as a fixed dollar amount that does not change for the life of the loan or a “graduated payment plan” in which the payments are lower at the beginning and gradually get larger.

While it may be tempting to select the “graduated payment plan” because it gives you more breathing room early on in your career, we often caution students against this. A lot can happened during your working career. What happens when 10 years from now you get unexpectedly laid off and are out of work for a period of time? Those graduated loan payments may be very high at that point making your financial hardship even more difficult.

Private loan may not offer a graduated payment option. Since private student loans are not regulated by any government agency they get to set all of the terms and conditions of the loans that they offer.

From all of the information that we have absorbed, if you can afford to enroll in a balanced based repayment plan, that is usually the most advantageous option from the standpoint of paying the least interest during the duration of the loan.

Income-Driven Repayment Program

All of the other loan repayment programs fall underneath the “income based payment” category, where your income level determines the amount of your monthly student loan payment within a given year. To qualify for the income based plans, your student loans have to be federal loans. Private loans do not have access to these programs. Many of these programs have a “loan forgiveness” element baked into the program. Meaning, if you make a specified number of payments or payments for a specified number of years, any remaining balance on the student loan is wiped out. For individuals that are struggling with their student loan payments, these programs can offer more affordable options even for larger student loan balances. Also, the income based payment plans are typically a better long-term solution than “deferments” or “forbearance”.

Here is the list of Income-Driven Repayment Programs:

Income-Contingent Repayment (ICR)

Income-Based Repayment (IBR)

Pay-As-You-Earn (PAYE)

Revised Pay-As-You-Earn (REPAYE)

Each of these programs has a different income formula and a different set of prerequisites for the type of loans that qualify for each program but I will do a quick highlight of each program. If you think there is a program that may fit your circumstances I encourage you to visit https://studentaid.ed.gov/sa/

We have found that borrowers have to do a lot of their own homework when it comes to determining the right program for their personal financial situation. The loan servicers, which you would hope have the information to steer you in the right direction, up until now, have not been the best resource for individuals with student loan debt or parent plus loans. Hence, the rise in the number of specialists in the private sector now serving as fee based consultants.

Income-Contingent Repayment (ICR)

This program is for Direct Loans only. The formula is based on 20% of an individual’s “discretionary income” which is the difference between AGI and 100% of federal poverty level. For a single person household, the 2018 federal poverty level is $12,140 and it changes each year. The formula will result in a required monthly payment based on this data. Once approved you have to renew this program every 12 months. Part of the renewal process in providing your most up to date income data which could change the loan payment amount for the next year of the loan repayment. After a 25-years repayment term, the remaining balance is forgiven but depending on the tax law at the time of forgiveness, the forgiven amount may be taxable. The ICR program is typically the least favorable of the four options because the income formula usually results in the largest monthly payment.

However, this program is one of the few programs that allows Parent PLUS borrowers but they must first consolidate their federal loans via the federal loan consolidation program.

Income-Based Repayment (IBR)

This program is typically more favorable than the ICR program because a lower amount of income is counted toward the required payment. Both Direct and FFEL loans are allowed but Parent Plus Loans are not. The formula takes into account 15% of “discretionary income” which is the difference between AGI and 150% of the federal poverty level. If married it does look at your joint income unless you file separately. Like the ICR program, the loan is forgiven after 25 years and the forgiveness amount may be taxable income.

Pay-As-You-Earn (PAYE)

This plan is typically the most favorable plan for those that qualify. This program is for Direct Loans only. The formula only takes into account 10% of AGI. The forgiveness period is shortened to 20 years. The one drawback is this program is limited to “newer borrowers”. To qualify you cannot have had a federal outstanding loan as of October 1, 2007 and it’s only available for federal student loans issued after October 1, 2011. Joint income is takes into account for married borrowers unless you file taxes separately.

Revised Pay-As-You-Earn (REPAYE)

Same as PAYE but it eliminates the “new borrower” restriction. The formula takes into account 10% of AGI. The only difference is for married borrowers, it takes into account joint income regardless of how you file your taxes. So filing separately does not help. The 20 year forgiveness is the same at PAYE but there is a 25 year forgiveness if the borrow took out ay graduate loans.

Loan Forgiveness Programs

There are programs that are designed specifically for forgive the remaining balance of the loan after a specific number of payment or number of years based on a set criteria which qualifies an individual for these programs. Individuals have to be very careful with “loan forgiveness programs”. While it seems like a homerun having your student loan debt erase, when these individuals go to file their taxes they may find out that the loan forgiveness amount is considered taxable income in the tax year that the loan is forgiven. With this unexpected tax hit, the celebration can be short lived. But not all of the loan forgiveness programs trigger taxation. Here are the three loan forgiveness programs:

Public Service Loan Forgiveness

Teacher Loan Forgiveness

Perkins Loan Forgiveness

Following the same format as above, I will provide you with a quick summary on each of these loan forgiveness programs with links to more information on each one.

Public Service Loan Forgiveness

This program is only for Direct Loans. To qualify for this loan forgiveness program, you must be a full-time employee for a “public service employer”. This could be a government agency, municipality, hospital, school, or even a 501(C)(3) not-for-profit. You must be enrolled in one of the federal repayment plans either balanced-based or income driven. Once you have made 120 payments AFTER October 1, 2007, the remaining balance is forgiven. Also the 120 payments do not have to be consecutive. The good news with this program is the forgiven amount is not taxable income. To enroll in the plan you have to submit the Public Service Loan Forgiveness Employment Certification Form to US Department of Education. See this link for more info: https://studentaid.ed.gov/sa/repay-loans/forgiveness-cancellation/public-service

Teacher Loan Forgiveness

This program is for Federal Stafford loans issued after 1998. You have to teach full-time for five consecutive years in a “low-income” school or educational services agency to qualify for this program. The loan forgiveness amount is capped at either $5,000 or $17,000 based on the subject area that you teach. https://studentaid.ed.gov/sa/repay-loans/forgiveness-cancellation/teacher#how-much

As special note, even though teachers may also be considered “Public Service” employees, you cannot make progress toward the Teacher Loan Forgiveness Program and the Public Service Loan Forgiveness Program at the same time.

To apply for this program, you must submit the Teacher Loan Forgiveness Application to your loan servicer.

Perkins Loan Forgiveness

As the name suggests, this program is only available for Federal Perkins Loans. Also, it’s only available to certain specific full-time professions. You can find the list by clicking on this link: https://studentaid.ed.gov/sa/repay-loans/forgiveness-cancellation/perkins

The Perkins forgiveness program can provide up to 100% forgiveness in 5 years with NO PAYMENTS REQUIRED. To apply for this program you have complete an application through the school, if they are the lender, or your loan servicer.

Be Careful Consolidating Student Loans

Young professionals have to be very careful when consolidating student loan debt. One of the biggest mistakes that we see borrows without the proper due diligence consolidate their federal student loans with a private institution to take advantage of a lower interest rate. Is some cases it may be the right move but as soon as this happen you are shut out of any options that would have been available to you if you still had federal student loans. Before you go from a federal loan to a private loan, make sure you properly weigh all of your options.

If you already have private loans and you want to consolidate the loans with a different lender to lower interest rate or obtain more favorable repayment term, there is typically less hazard in doing so.

You are allowed to consolidate federal loans within the federal system but it does not save you any interest. They simply take the weighted average of all the current interest rate on your federal loans to reach the interest rate on your new consolidated federal student loan.

Defaulting On A Student Loan

Defaulting on any type of loan is less than ideal but student loans are a little worse than most loans. Even if you claim bankruptcy, there are very few cases where student loan debt gets discharged in a bankruptcy filing. For private loans, not only does it damage your credit rating but the lender can sue you in state court. Federal loans are not any better. Defaulting on a federal loan will damage your credit score but the federal government can go one step further than private lenders to collect the unpaid debt. They have the power to garnish your wages if you default on a federal loan.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The Top 2 Strategies For Paying Off Student Loan Debt

With total student loan debt in the United States approaching $1.4 Trillion dollars, I seem to be having this conversation more and more with clients. There has been a lot of speculation between president obama and student loans, but student loan debt is still piling up. The amount of student loan debt is piling up and it's putting the next generation of

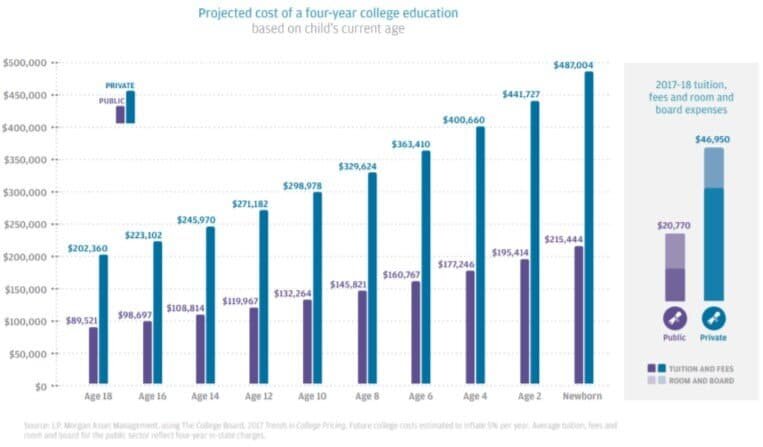

With total student loan debt in the United States approaching $1.4 Trillion dollars, I seem to be having this conversation more and more with clients. There has been a lot of speculation between president obama and student loans, but student loan debt is still piling up. The amount of student loan debt is piling up and it's putting the next generation of our work force at a big disadvantage. While you yourself may not have student loan debt, at some point you may have to counsel a child, grandchild, friend, neighbor, or a co-worker that just can't seem to get ahead because of the financial restrains of their student loan payments. After all, for a child born today, it's projected that the cost for a 4 year degree including room and board will be $215,000 for a State College and $487,000 for a private college. Half a million dollars for a 4 year degree!!

The most common reaction to this is: "There is no way that this can happen. Something will have to change." The reality is, as financial planners, we were saying that exact same thing 10 years ago but we don't say that anymore. Despite the general disbelief that this will happen, the cost of college has continued to rise at a rate of 6% per year over the past 10 years. It's good old supply and demand. If there is a limited supply of colleges and the demand for a college degree keeps going up, the price will continue to go up. As many of us know, a college degree is not necessarily an advantage anymore, it's the baseline. You need it just to get the job interview and that will be even more true for types of jobs that will be available in future years.

No Professional Help

Making matters worse, most individuals that have large student loan debt don't have access to high quality financial planners because they do not have any investible assets since everything is going toward paying down their student loan debt. I wrote this article to give our readers a look into how we as Certified Financial Planners® help our clients to dig out of student loan debt. Unfortunately a lot of the advice that you will find by searching online is either incomplete or wrong. The solution for digging out of student loan debt is not a one size fits all solution and there are trap doors along the way.

Loan Inventory

The first step in the process is to the collect and organize all of the information pertaining to your student loan debt. Create a spreadsheet that lists the following information:

Name of Lender

Type of Loan (Federal or Private)

Name of Loan Servicer

Total Outstanding Loan Balance

Interest Rate

Fixed or Variable Interest Rate

Minimum Monthly Payment

Current Monthly Payment

Estimated Payoff Date

Now, below this information I want you to list January 1 of the current year and the next 10 years. It will look like this:

Total Balance

January 1, 2018

January 1, 2019

January 1, 2020

Each year you will record your total student loan debt below your itemized student loan information. Why? In most cases you are not going to be able to payoff your student loans overnight. It’s going to be a multi-year process. But having this running total will allow you to track your progress. You can even add another column to the right of the “Total Balance” column labelled “Goal”. If your goal is to payoff your student loan debt in five years, set some preliminary balance goals for yourself. When you receive a raise or a bonus at work, a tax refund, or a cash gift from a family member, this will encourage you to apply some or all of those cash windfalls toward your student loan balance to stay on track.

Order of Payoff

The most common advice you will find when researching this topic is “make minimum payments on all of the student loans with the exception of your student loan with the highest interest rate and apply the largest payment you can against that loan”. Mathematically this is the right strategy but we do not necessary recommend this strategy for all of our clients. Here’s why……..

There are two situations that we typically run into with clients:

Situation 1: “I’m drowning in student loan debt and need a lifeline”

Situation 2: “I’m starting to make more money at my job. Should I use some of that extra income to pay down my student loan debt or should I be applying it toward my retirement plan or saving for a house?”

Situation 1: I'm Drowning

As financial planners we are unfortunately running into Situation 1 more frequently. You have young professionals that are graduating from college with a 4 year degree, making $50,000 per year in their first job, but they have $150,000 of student loan debt. So they basically have a mortgage that starts 6 months after they graduate but that mortgage payment comes without a house. For the first few years of their career they are feeling good about their new job, they receive some raises and bonuses here and there, but they still feel like they are struggling every month to meet their expenses. The realization starts to set in the “I’m never going to get ahead because these student loan payments are killing me. I have to do something.”

If you or someone you know is in this category remember these words: “Cash is king”. You will hear this in the business world and it’s true for personal finances as well. As mentioned earlier, from a pure math standpoint, they fastest way to get out of debt is to target the debt with the highest interest rate and go from there. While mathematically that may work, we have found that it is not the best strategy for individuals in this category. If you are in the middle of the ocean, treading water, with the closest island a mile away, why are we having a debate about how fast you can swim to that island? You will never make it. Instead you just need someone to throw you a life preserver.

Life Preserver Strategy

If you are just barely meeting your monthly expense or find yourself falling short each month, you have to stop the bleeding. In these situations, you should be 100% focus on improving your current cash flow not whether you are going to be able to payoff your student loans in 8 years instead of 10 years. In the spreadsheet that you created, organize all of your student loan debt from the largest outstanding loan balance to the smallest. Ignore the interest rate column for the time being. Next, begin making the minimum payments on all of your student loans except for the one with the SMALLEST BALANCE. We need to improve your cash flow which means reducing the number of monthly payments that you have each month. Once the month to month cash flow is no longer an issue then you can graduate to Situation 2 and revisit the debt payoff strategy.

This strategy also builds confidence. If you have a $50,000 loan with a 7% interest rate and two other student loans for $5,000 with an interest rate of 4% while applying more money toward the largest loan balance will save you the most interest long term, it’s going to feel like your climbing Mt. Everest. “Why put an extra $200 toward that $50,000 loan? I’m going to be paying it until I’m 50.” There is no sense of accomplishment. We find that individuals that choose this path will frequently abandon the journey. Instead, if you focus your efforts on the loans with the smaller balances and you are able to pay them off in a year, it feels good. Getting that taste of real progress is powerful. This strategy comes from the book written by Dave Ramsey called the Total Money Makeover. If you have not read the book, read it. If you have a child or grandchild graduating from college, if you were going to give them a check for graduation, buy the book for them and put the check in the book. Tell them that “this check will help you to get a start in your new career but this book is worth the amount of the check multiplied by a thousand”.

Situation 2: Paying Off Your Student Loans Faster

If you are in Situation 2, you are no longer treading water in the middle of the ocean and you made it to the island. The name of this island is “Risk Free Rate Of Return”. Let me explain.

Individuals in this scenario have a good handle on their monthly expenses and they are finding that they now have extra discretionary income. So what’s the best use of that extra income? When you are younger there are probably a number items on your wish list, some of which you may debate looking into title loans near me to obtain. Here are the top four that we see:

Retirement savings

Saving for a house

Paying off student loan debt

Buying a new car

Don't Leave Free Money On The Table

Before applying all of your extra income toward your student loan payments, we ask our clients “what is the employer contribution formula for your employer’s retirement plan?” If it’s a match formula, meaning you have to put money in the plan to get the employer contribution, we will typically recommend that our clients contribute the amount needed to receive the full employer match. Otherwise you are leaving free money on the table.

The amount of that employer contribution represents a risk free rate of return. Meaning, unlike the investing in the stock market, you do not have to take any risk to receive that return on your money. If your company guarantees a 100% match on the first 5% of pay contribution out of your paycheck into the plan, your money is guaranteed to double up to 5% of your pay. Where else are you going to get a 100% risk free rate of return on your money?

Start With The Highest Interest Rate

Now that you have extra income each month you can begin to pick and choose how you apply it. You should list all of you student loans from the highest interest rate to the lowest. If it’s close between two interest rates but one is a fixed interest rate and the other is a variable interest rate, it’s typically better to pay down the variable interest rate loan first if interest rates are expected to move higher. Apply the minimum payment amount to all of your student loan payments and apply as much as you can toward the loan with the HIGHEST INTEREST RATE. Once the loan with the highest interest rate is paid off, you will move on to the next one.

Again, by applying more money toward your student loans, those additional payments represent a risk free rate of return equal to the interest rate that is being charges on each loan. For example, if the highest interest rate on one of your student loans is 7%, every additional dollar that you are apply toward paying off that loan you are receiving a 7% rate of return on because you are not paying that amount to the lender.

Here is a rebuttal question that we sometimes get: “But wouldn’t it be better to put it in the stock market and earn a higher rate of return?” However, that’s not an apple to apples comparison. The 7% rate of return that you are receiving by paying down that student loan balance is guaranteed because it represents interest that would have been paid to the lender that you are now keeping. By contrast, even though the stock market may average an 8% annualized rate of return over a 10 year period, you have to take risk to obtain that 8% rate of return. A 7% risk free rate of return is the equivalent of being able to buy a CD at a bank with a 7% interest rate guaranteed by the FDIC which does not exist right now.

But Can't I Deduct The Interest On My Student Loans?

It depends on how much you make. In 2018, if you are single, the deduction for student loan interest begins to phaseout at $70,000 of AGI and you completely lose the deduction once your AGI is above $85,000. If you are married filing a joint tax return, the deduction begins to phaseout at $140,000 of AGI and it’s completely gone once your AGI hits $170,000.

Also the deduction is limited to $2,500.

However, even if you can deduct the interest on your student loan, the tax benefit is probably not as big as you think. Let me explain via an example. Take the following fact set:

Tax Filing Status: Single

Adjusted Gross Income (AGI): $50,000

Outstanding Student Loan Balance: $60,000

Interest Rate: 7% ($4,200 Per Year)

First, you are limited to deducting $2,500 of the $4,200 in student loan interest that you paid to the lender. At $50,000 of AGI your top federal tax bracket in 2018 is 22%. So that $2,500 equals $550 in actual tax savings ($2,500 x 22% = $550). If you want to get technical, taking the tax deduction into account, your after tax interest rate on your student loan debt is really 6.08% instead of 7%. Can you get a CD from a bank right now with a 6% interest rate? No. From both a debt reduction standpoint and a rate of return standpoint, it probably makes sense to pay down that loan more aggressively.

Striking A Balance

When you are younger, you typically have a lot of financial goals such as saving for retirement, paying off debt, saving for the down payment on your first house, starting a family, college savings for you kids, etc. While I'm sure you would like to take all of your extra income and really start aggressively reducing your student loans you have to determine what the right balance is between all of your financial goals. If you receive a $5,000 bonus from work, you may allocate $3,000 of that toward your student loan debt and deposit $2,000 in your savings account for the eventual down payment on your first house. We also recommend speaking a loan authority company to see what can be done to help you reach your goal. One example being to create that "goal" column in your student loan spreadsheet will help you to keep that balance and eventually lead to the payoff of all of your student loans.

Forgiveness Scheme

Although they are not very common and only a few people can qualify for one of these schemes, they will provide great help. A student loan forgiveness scheme can help a student pay off their loan over an extended period of time, a shorter period of time, reduce the amount they owe, or entirely pay off the loan for them. However, like I have already mentioned, this is based upon whether they qualify or not.I hope this has been of some assistance and i have provided you with some helpful advice on how to prepare for and manage your student loan.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.