Can I Open A Roth IRA For My Child?

Parents always want their children to succeed financially so they do everything they can to set them up for a good future. One of the options for parents is to set up a Roth IRA and we have a lot of parents that ask us if they are allowed to establish one on behalf of their son or daughter. You can, as long as they have earned income. This can be a

Parents will often ask us: “What type of account can I setup for my kids that will help them to get a head start financially in life"?”. One of the most powerful wealth building tools that you can setup for your children is a Roth IRA because all of accumulation between now and when they withdrawal it in retirement will be all tax free. If your child has $10,000 in their Roth IRA today, assuming they never make another deposit to the account, and it earns 8% per year, 40 years from now the account balance would be $217,000.

Contribution Limits

The maximum contribution that an individual under that age of 50 can make to a Roth IRA in 2022 is the LESSER of:

$6,000

100% of earned income

For most children between the age of 15 and 21, their Roth IRA contributions tend to be capped by the amount of their earned income. The most common sources of earned income for young adults within this age range are:

Part-time employment

Summer jobs

Paid internships

Wages from parent owned company

If they add up all of their W-2's at the end of the year and they total $3,000, the maximum contribution that you can make to their Roth IRA for that tax year is $3,000.

Roth IRA's for Minors

If you child is under the age of 18, you can still establish a Roth IRA for them. However, it will be considered a "custodial IRA". Since minors cannot enter into contracts, you as the parent serve as the custodian to their account. You will need to sign all of the forms to setup the account and select the investment allocation for the IRA. It's important to understand that even though you are listed as a custodian on the account, all contributions made to the account belong 100% to the child. Once the child turns age 18, they have full control over the account.

Age 18+

If the child is age 18 or older, they will be required to sign the forms to setup the Roth IRA and it's usually a good opportunity to introduce them to the investing world. We encourage our clients to bring their children to the meeting to establish the account so they can learn about investing, stocks, bonds, the benefits of compounded interest, and the stock market in general. It's a great learning experience.

Contribution Deadline & Tax Filing

The deadline to make a Roth IRA contribution is April 15th following the end of the calendar year. We often get the question: "Does my child need to file a tax return to make a Roth IRA contribution?" The answer is "no". If their taxable income is below the threshold that would otherwise require them to file a tax return, they are not required to file a tax return just because a Roth IRA was funded in their name.

Distribution Options

While many of parents establish Roth IRA’s for their children to give them a head start on saving for retirement, these accounts can be used to support other financial goals as well. Roth contributions are made with after tax dollars. The main benefit of having a Roth IRA is if withdrawals are made after the account has been established for 5 years and the IRA owner has obtained age 59½, there is no tax paid on the investment earnings distributed from the account.

If you distribute the investment earnings from a Roth IRA before reaching age 59½, the account owner has to pay income tax and a 10% early withdrawal penalty on the amount distributed. However, income taxes and penalties only apply to the “earnings” portion of the account. The contributions, since they were made with after tax dollar, can be withdrawal from the Roth IRA at any time without having to pay income taxes or penalties.

Example: I deposit $5,000 to my daughters Roth IRA and four years from now the account balance is $9,000. My daughter wants to buy a house but is having trouble coming up with the money for the down payment. She can withdrawal $5,000 out of her Roth IRA without having to pay taxes or penalties since that amount represents the after tax contributions that were made to the account. The $4,000 that represents the earnings portion of the account can remain in the account and continue to accumulate tax-free. Not only did I provide my daughter with a head start on her retirement savings but I was also able to help her with the purchase of her first house.

We have seen clients use this flexible withdrawal strategy to help their children pay for their wedding, pay for college, pay off student loans, and to purchase their first house.

Not Limited To Just Your Children

This wealth accumulate strategy is not limited to just your children. We have had grandparents fund Roth IRA's for their grandchildren and aunts fund Roth IRA's for their nephews. They do not have to be listed as a dependent on your tax return to establish a custodial IRA. If you are funded a Roth IRA for a minor or a college student that is not your child, you may have to obtain the total amount of wages on their W-2 form from their parents or the student because the contribution could be capped based on what they made for the year.

Business Owners

Sometime we see business owners put their kids on payroll for the sole purpose of providing them with enough income to make the $6,000 contribution to their Roth IRA. Also, the child is usually in a lower tax bracket than their parents, so the wages earned by the child are typically taxed at a lower tax rate. A special note with this strategy, you have to be able to justify the wages being paid to your kids if the IRS or DOL comes knocking at your door.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Social Security Loophole: Age 62+ With Kids In High School

There is a little known loophole in the social security system for parents that are age 62 or older with children still in high school or younger. Since couples are having children later in life this situation is becoming more common and it could equal big dollars for families that are aware of this social security filing strategy.

There is a little known loophole in the social security system for parents that are age 62 or older with children still in high school or younger. Since couples are having children later in life this situation is becoming more common and it could equal big dollars for families that are aware of this social security filing strategy.

Here is how it works. If you are age 62 or older and you have children under that age of 18, they can collect a social security benefit based on your earnings history equal to half of the parents social security benefit at normal retirement age. This amount could equal as much as $16,122 per year for one child for higher income earners. If you have multiple children the total annual amount paid to your family members could equal between 150% to $180% of your normal retirement benefit which could be in excess of $40,000 per year depending on your earnings history.

There are some key considerations. First, your children cannot collect on this “family benefit” until you have begun to collect your social security benefit. You can turn on your social security benefit as early as age 62 but they reduce the monthly amount that you receive if you turn on the benefit prior to your normal retirement age. However, it may make sense to do so depending on the amount of the family benefit paid and the duration of the benefit. If you wait until normal retirement age, you will receive a slightly higher social security benefit for yourself, but all of the social security dollars that could have been paid to your children is lost.

Second, if you are still working and your earned income exceeds certain thresholds this filing strategy may not be advantageous due to the earned income penalty. They reduce your social security benefit by $1 for every $2 earned over a given threshold ($16,920 in 2017). Not only is your social security benefit reduce but also the benefit to your dependents.

Due to these restrictions, this filing strategy yields that greatest benefit to parents that are either fully or partially retired, age 62 or older, with a child or children below the age of 18.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Should I Gift A Stock To My Kids Or Just Let Them Inherit It?

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is largely influenced by the amount of appreciation or depreciation in the stock.

Gifting Stock

When you make a non-cash gift such as a stock, house, or even a business, the person receiving the gift assumes your cost basis in the assets. They do not receive a “step-up” in basis at the time the gift is made. Example, I buy XYZ Corp stock in 1995 for $10,000. In 2017, those shares of XYZ are now worth $100,000. If I gift them to my kids, no one owes tax on the gift at the time that the gift is made but my kids carry over my cost basis in the stock. If my kids hold the stock for 10 more years and sell it for $150,000, their basis in the stock is $10,000, and they owe capital gains tax on the $140,000 gain. Thus, creating an adverse tax consequence for my kids.

Inheriting Stock

Instead, let’s say I continue to hold XYZ stock and when I pass away my kids inherited the stock. If I pass away in 10 years and the stock is worth $150,000 then my kids receive a “step-up” in basis which means that their cost basis in the stock is the value of the stock as of the date of my death. They inherit the stock at $150,000 value, sell it the next day, and they owe $0 in taxes due to the step-up in basis upon my death.

In general, if you have assets that have low cost basis it is usually better for your heirs to inherit the assets as opposed to gifting it to them.

The concept is often times reversed for assets that have depreciated in value…..with an important twist. If I purchase XYZ Corp stock in 1995 for $10,000 but in 2017 it’s only worth $5,000, if I sold the stock myself I would capture the realized investment loss and could use it to offset investment gains or reduce my income by $3,000 for the IRS realized loss allowance.

Here is a very important rule......

In most cases, do not gift a depreciated asset to someone else. Why? When you gift an asset that has depreciated in value the carry over basis rules change. For an asset that has depreciated in value, the carry over basis for the person receiving the gift is the higher of the fair market value of the asset or the cost basis of the person making the gift. In other words, the loss evaporates when I gift the asset to someone else and no one gets the tax advantage of using the realized loss for tax purposes. It would be better if I sold the stock, captured the investment loss, and then gifted the cash.

If they inherit the stock that has lost value there is no value to the step-up in basis because the stock has not appreciated in value.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How To Teach Your Kids About Investing

As kids enter their teenage years, as a parent, you begin to teach them more advanced life lessons that they will hopefully carry with them into adulthood. One of the life lessons that many parents teach their children early on is the value of saving money. By their teenage years many children have built up a small savings account from birthday gifts,

As kids enter their teenage years, as a parent, you begin to teach them more advanced life lessons that they will hopefully carry with them into adulthood. One of the life lessons that many parents teach their children early on is the value of saving money. By their teenage years many children have built up a small savings account from birthday gifts, holidays, and their part-time jobs. As parents you have most likely realized the benefit of compounding interest through working with a financial advisor, contributing to a 401(k) plan, or depositing money to a college savings account. As financial planners, we often get the question: “What is the best way to teach your children about the value of investing and compounding interest? "

The #1 rule.......

We have been down this road many times with our clients and their children. Here is the number one rule: Make it an engaging experience for your kids. Investments can be a very dull topic to talk about and it can be painfully dull from a child’s point of view. All they know is the $1,000 that was in their savings account is now with their parent’s investment guy.

Ignoring the life lessons for a moment, the primary investment vehicle for brokerage accounts with balances under $50,000 is typically a mutual fund. But let’s pause for a moment. We have a dual objective here. We of course want our children to make as much money as possible in their investment account but we also want to simultaneously teach them life long lessons about investing.

The issue with young investors

Explaining how a mutual fund operates can be a complex concept for a first time investor because you have all of these companies in one investment, expense ratios, different types of funds, and different fund families. It’s not exciting, it’s intimidating.

Consider this approach. Ask the child what their hobbies are? Do they have a cell phone? Have them take their cell phone out during the meeting and ask them how often they use it during the day and how many of their friends have cell phones. Then ask them, if you received $20 every time someone in this area bought a cell phone would you have a lot of money? Then explain that this scenario is very similar to owning stock in a cell phone company. The more they sell the more money the company makes. As a “shareholder” you own a piece of that company and you receive a piece of the profits if the company grows. If your child plays sports, do they wear a lot of Nike or Under Armour? Explain investing to them in a way that they can relate it to their everyday life. Now you have their attention because you attached the investment idea to something they love.

A word of caution....

If they are investing in stocks it is also important for them to understand the concept of risk. Not every investment goes up and you could start with $1,000 and end the year with $500, so they need to understand risk and time horizon.

While it’s not prudent in most scenarios to invest 100% of a portfolio in one stock, there may be some middle ground. Instead of investing their entire $1,000 in a mutual fund, consider investing $500 – $700 in a mutual fund but let them pick one to three stocks to hold in the account. It may make sense to have them review those stock picks with your investment advisor for two reasons. One, you want them to have a good experience out of the gates and that investment advisor can provide them with their option of their stock picks. Second, the investment advisor can tell them more about the companies that they have selected to further engage them.

Don't forget the last step......

Download an app on their smartphone so they can track the investments that they selected. You may be surprise how often they check the performance of their stock holdings and how they begin to pay attention to news and articles applicable to the companies that they own.At that point you have engaged them and as they hopefully see their investment holdings appreciate in value they will become even more excited about saving money in their investment account and making their next stock pick. In addition, they also learn valuable investment lessons early on like when one of their stocks loses value. How do they decide whether to sell it or continue to hold it? It’s a great system that teaches them about investing, decision making, risk, and the value of compounding investment returns.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Financial Planning To Do's For A Family

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with the

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with them.

There is a lot of information to take into consideration when putting together a financial plan and the larger your family the more pieces to the puzzle. It is important to set goals and celebrate them when they are met. Everything cannot be done in a day, a week, or a month, so creating a task list to knock off one by one is usually an effective approach. Using relatives, friends, and professionals as resources is important to know what should be on that list for topics you aren’t familiar with.

Create a Budget

It may seem tedious but this is one of the most important pieces of a family’s financial plan. You don’t have to track every dollar coming in and out but having a detailed breakdown on where your money is being spent is necessary in putting together a plan. This simple Expense Planner can serve as a guideline in starting your budget. If you don’t have an accurate idea of where your money is being spent then you can’t know where you can cut back or afford to spend more if needed. Also, the budget is a great topic during a romantic dinner.

You will always want to have 4-6 months expenses saved up and accessible in case a job is lost or someone becomes disabled and cannot work. Having an accurate budget will help you determine how much money you should have liquid.

Insurance

You want to be sure you are sufficiently covered if anything ever happened. One terrible event could leave your family in a situation that may have been avoidable. Insurance is also something you want to take care of as soon as possible so you know the coverage is there if needed.

Health Insurance

Research the policies that are available to you and determine which option may be the most appropriate in your situation. It is important to know the medical needs of your family when making this decision.

Turning one spouse’s single coverage into family coverage is one of the more common ways people obtain coverage for a family. Insurance companies will usually only allow changes to policies through open enrollment or when a “qualifying event” occurs. Having a child is usually a qualifying event but this may only allow the child to be added to one’s coverage, not the spouse. If that is the case, the spouse will want to make sure they have their own coverage until they can be added to the family plan.

It is important to use the resources available to you and consult with your health insurance provider on the ins and outs. If neither spouse has coverage through work, the exchange can be a resource for information and an option to obtain coverage (https://www.healthcare.gov/).

Life Insurance

The majority of people will obtain Term Life Insurance as it is a cost effective way to cover the needs of your family. Life insurance policies have an extensive underwriting process so the sooner you start the sooner you will be covered if anything ever happened. How Much Life Insurance Do I Need?, is an article that may help answer the question regarding the amount of life insurance sufficient for you.

Disability Insurance

The probability of using disability insurance is likely more than that of life insurance. Like life insurance, there is usually a long underwriting process to obtain coverage. Disability insurance is important as it will provide income for your family if you were unable to work. Below are some terms that may be helpful when inquiring about these policies.

Own Occupation – means that insurance will turn on if you are unable to perform YOUR occupation. “Any Occupation” is usually cheaper but means that insurance will only turn on if you can prove you can’t do ANY job.

60% Monthly Income – this represents the amount of the benefit. In this example, you will receive 60% of your current income. It is likely not taxable so the net pay to you may be similar to your paycheck. You can obtain more or less but 60% monthly income is a common benefit amount.

90 Day Elimination Period – this means the benefit won’t start until 90 days of being disabled. This period can usually be longer or shorter.

Cost of Living or Inflation Rider – means the benefit amount will increase after a certain time period or as your salary increases.

Wills, POA’s, Health Proxies

These are important documents to have in place to avoid putting the weight of making difficult decisions on your loved ones. There are generic templates that will suffice for most people but it is starting the process that is usually the most difficult. “What Is The Process Of Setting Up A Will?, is an article that may help you start.

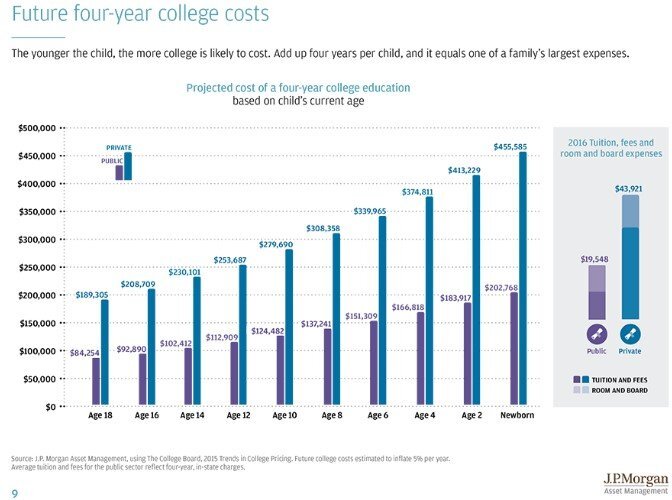

College Savings

The cost of higher education is increasing at a rapid rate and has become a financial burden on a lot of parents looking to pick up the tab for their kids. 529 accounts are a great way to start saving early. There are state tax benefits to parents in some states (including NYS) and if the money is spent on tuition, books, or room and board, the gain from the investments is tax free. Roth IRA’s are another investment vehicle that can be used for college but for someone to contribute to a Roth IRA they must have earned income. Therefore, a newborn wouldn’t be able to open a Roth IRA. Since the gain in 529’s is tax free if used for college, the earlier the dollars go into the account the longer they have to potentially earn income from the market.

529’s can also be opened by anyone, not just the parents. So if the child has a grandparent that likes buying savings bonds or a relative that keeps purchasing clothes the child will wear once, maybe have them contribute to a 529. The contribution would then be eligible for the tax deduction to the contributor if available in the state.

Below is a chart of the increasing college costs along with links to information on college planning.

About Rob……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.